DORA is now a household name

From compliance challenges to future milestones

One year into DORA: Where do we stand and what lies ahead?

As we approach one year since the entry into force of the Digital Operational Resilience Act (DORA), a large majority of financial institutions are still not fully compliant. While significant progress has been made, several requirements continue to emerge as particularly challenging.

This raises a number of key questions for the market: Where do institutions currently stand? What tangible changes has DORA brought so far? What are the main obstacles in the compliance journey? And what major milestones should institutions prepare for next?

This article aims to provide insights into the current market landscape and offer a forward-looking perspective, drawing on our experience supporting multiple entities throughout their DORA compliance journey, as well as on the findings of our 2025 DORA European Survey, published this summer.

Current market status: Insights from the DORA European Survey

Our survey results show that progress towards full compliance remains uneven across the different DORA pillars. While 48% of surveyed entities consider themselves fully compliant with the ICT Incident Management pillar, only 25% report full compliance with the of ICT Risk Management pillar. The figures drop even further for Digital Operational Resilience Testing and ICT Third-Party Risk Management, where just 8% of respondents consider themselves fully compliant.

These results clearly indicate that the journey towards full DORA compliance is still long for most institutions. In fact, 50% of surveyed institutions expect to reach full compliance only by 2026 or even 2027, well beyond the initial regulatory timeline.

The impact of DORA so far: Three key positive developments

Despite the multiple challenges—some of which have only recently been uncovered and will be explored later in this article—we have observed three major positive effects driven by DORA so far.

First, DORA has compelled institutions to establish a clear and structured link between business functions, the underlying technological landscape, and supporting ICT service providers. As a result, asset management has become a critical, living capability, rather than a static inventory updated once a year.

Second, DORA has significantly increased the involvement of executive management and supervisory functions, the so-called “management body.” Their accountability under the regulation has elevated both their engagement and their understanding of ICT risk management across the organization.

And third, DORA has acted as a catalyst for breaking down silos. It has fostered stronger alignment between risk management, cybersecurity, and business continuity functions, which historically often operated independently, with limited coordination.

The challenges faced and how the financial sector is responding

To better understand how financial institutions are progressing on their DORA journey, it is useful to take a closer look at each pillar, the key challenges encountered, and the ways in which those challenges have been addressed.

What to expect as next major milestones

What to expect for financial institutions

The latest milestone reached was the designation of Critical Third-Party Providers (CTTPs) in the EU. 19 CTPPs were designated that will be directly overseen by the joint supervisory teams led by the European Supervisory Authorities (ESAs). These third party providers will have to align their internal governance and security with DORA requirements and the financial institutions of EU.

Regarding supervision by national competent authorities, regulators across the EU—including the CSSF—have indicated that the initial on-site inspections will primarily focus on the maturity of institutions’ DORA gap assessments, implementation roadmaps, and associated action plans. In Germany, BaFin initiated DORA- related on-site visits as early as May 2025. In Luxembourg, while no DORA-specific on-site inspections were undertaken by the CSSF in 2025, several thematic reviews targeting management companies and banks were announced. The CSSF is expected to accelerate its supervisory activities move in 2026, with IT on-site inspection programs adapted to reflect DORA requirements.

What to expect for support PSFs

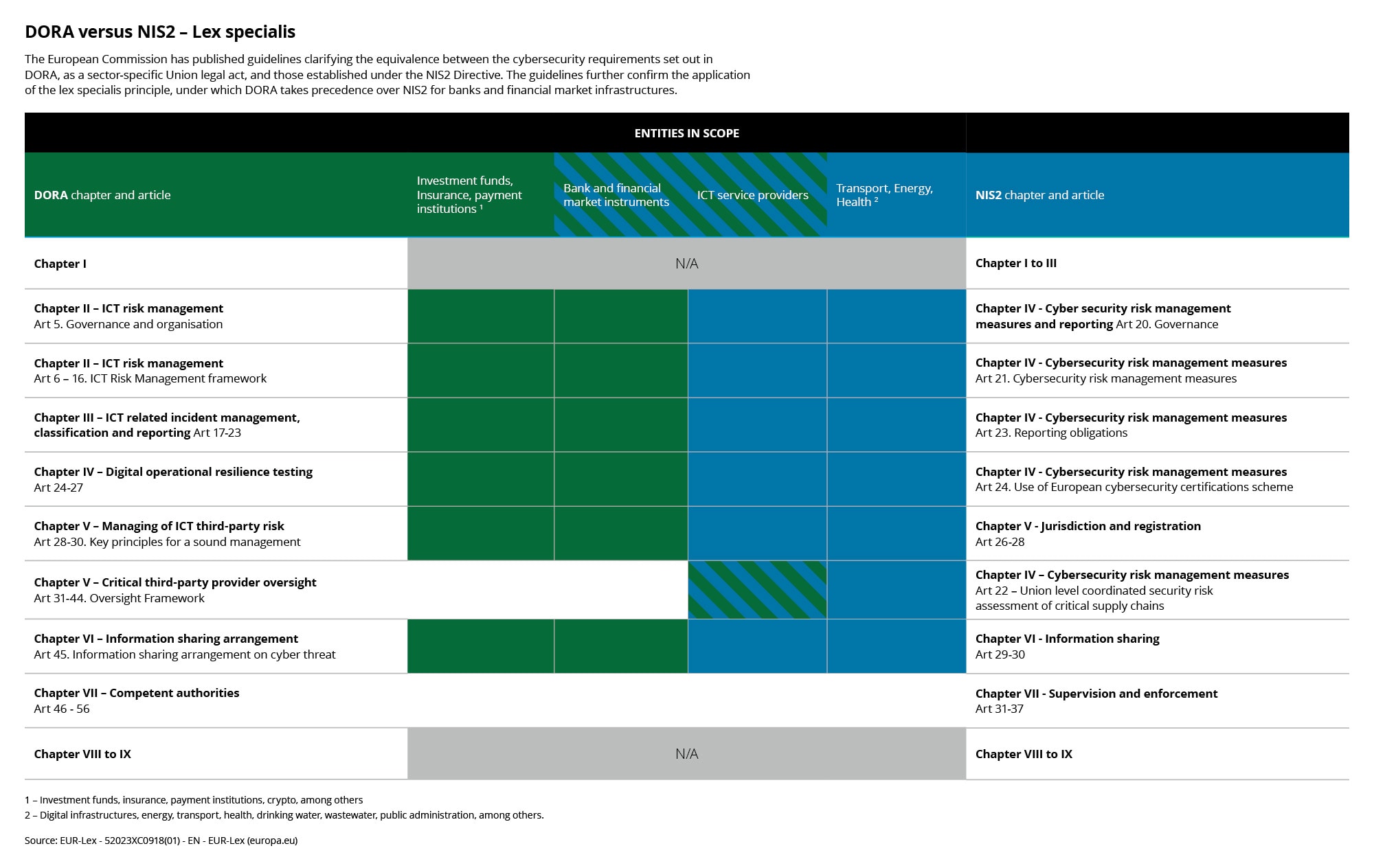

The transposition of the NIS2 Directive will complete the regulatory landscape for support PSFs providing ICT services.

While DORA is a sector-specific regulation that is directly applicable to financial entities, NIS2 is cross-sector directive that requires national transposition into local law. As a result, the scope of entities subject to NIS2 does not fully align with those subject to DORA. Nevertheless, two distinct areas of overlap exist.

The first overlap concerns banks and financial market infrastructures, which fall directly within the scope of both NIS2 and DORA. In this case, the lex specialis principle applies, meaning that DORA takes precedence over NIS2. This approach presents duplicate regulatory requirements and ensures that financial-sector-specific rules prevail.

The second overlap applies to support PSF providing ICT services. These entities are directly subject to NIS2 requirements, while DORA obligations apply to them indirectly through contractual arrangements. Financial entities subject to DORA must cascade relevant DORA requirements into their contracts with ICT service providers. In this scenario, the lex specialis principle does not apply. However, by achieving compliance with NIS2, a Support PSF can already meet a significant portion of its clients’ DORA-related expectations.

Key areas where DORA and NIS2 overlap include:

- ICT and cyber risk management processes, including the level of comprehensiveness and risk reporting requirements.

- Incident classification criteria, reporting timeline, and data requirements.

- Third-party and supply chain risk management, including subcontracting, where DORA introduces additional obligations compared to NIS2.

- Responsibilities of the management body.

The illustration below provides a high-level view of these overlapping areas and their respective regulatory coverage.

Click here to enlarge the table

In summary, DORA remains a demanding journey for the financial sector, yet institutions have already taken significant steps toward strengthening their digital operational resilience. While the first wave of challenges—focused on interpretation, scoping, and initial implementation—has largely been overcome, a second wave is now emerging. This next phase centers on embedding DORA requirements into business-as-usual operations, alongside addressing more structural and technical implementation challenges.

Ultimately, these combined efforts will better position financial entities and their service providers for upcoming supervisory scrutiny, with on-site inspections expected to be conducted against a significantly higher bar of maturity and preparedness.

Laureline Senequier