"Solvency II Capital requirements" of collective investment funds: an Overview

This article is part of a series sharing aggregated analytics on collective investment funds used in different regulatory or business contexts. On this occasion, we will analyse the Solvency II capital requirements (SCR) for market risk in the context of look-through on collective investment funds.

The SCR, as defined in the Solvency II regulation (EU CDR 2015/35), as amended, represents the level of eligible own funds that should allow an insurance or reinsurance undertakings to absorb significant losses. The SCR is calibrated using the Value at Risk (VaR) of the basic own funds of an insurance or reinsurance undertaking, subject to a confidence level of 99.5% over one year. In other words, this would correspond to a one-year loss level expected not to be breached more than once over the next two hundred years.

The SCR is composed of different risk modules and sub-modules as laid out in the Solvency II regulation. For this article, we will only focus on the Market SCR (excluding Concentration Risk) which, on average, represents the main component of the total SCR for European insurance companies and particularly for collective investment funds.

Our internal analysis considers a sample of 310 sub-funds covering a wide range of asset classes, and the graph below depicts the typical Market SCR observed per investment strategy. While the market SCR range for some categories is quite well defined—such as fixed income covered, capital protected, and money market—for other investment strategies the observed market SCR can vary significantly.

Distribution of Market SCR (2023) across different investment strategies1

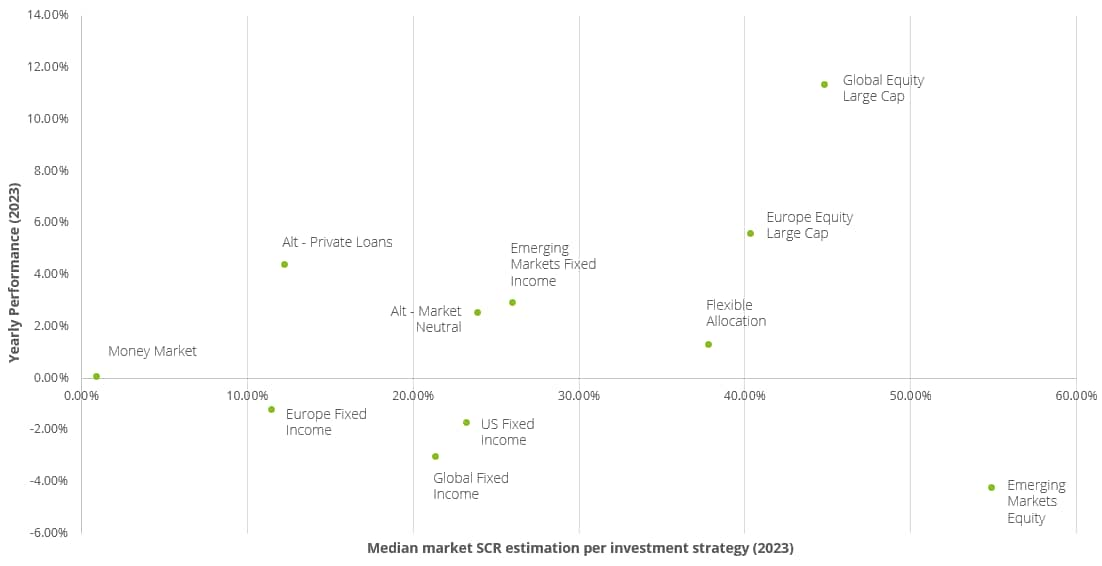

On another note, we found it interesting to compare the net average annual performance of the sub-funds in scope over the last 3 years and the average Market SCR for each investment funds category.

Comparative Yearly performance 2023 VS Median Market SCR per investment strategies2

We hope the above was of interest and stay tuned for other analytics.

1 SCR Benchmarking based on a sample of 1374 SCR computations performed across 2023, on a representative scope of 366 sub funds. Only the most represented strategies in the sample considered are included in above chart. The box and whisker chart are represented without outliers.

2 Yearly performances collected from Morningstar. SCR Benchmarking based on a sample of 1374 SCR computations performed across 2023, on a representative scope of 366 sub funds. Only the most represented strategies in the sample considered are included in above chart.