Retail Forecasts: Rocky Road

For retailers the immediate road ahead is looking rocky... but there is also some sunshine on the way.

The latest issue of Retail Forecasts outlines the rocky road facing retailers after a sombre summer.

For retailers, the year has begun with a fizzle rather than a bang. Real spending decreased by 0.4% over the March quarter of 2024, reversing much of the Black Friday gains.

Indeed, retail has been subdued for some time now. In per capita terms, real retail turnover has not grown in quarterly terms for seven straight quarters since June 2022. Retail sales volumes per capita fell 1.0% over the March quarter and are now 3.6% lower than a year ago – reflecting just how much an average consumer has had to pull back on spending. It has also fed into rising business insolvencies in retail and hospitality.

Keeping spending at bay has been persistently high levels of price growth seen in essential spending outside of retail (rents, insurance, utilities) causing consumers to cut back on spending on discretionary retail.

The latest monthly Retail Trade figures released last week continue the sombre story with nominal retail turnover only increasing by 0.1% over the month of April. Additionally, today’s National Accounts data on Q1 2024 points to the difficult economic environment faced by retailers. Real GDP growth slowed over the March quarter, increasing by just 0.1% over the quarter, and just 1.1% over the past year. And while household consumption was a little stronger, growing by 0.4% over the March quarter, most of the growth was attributable to spending on services.

The immediate road ahead is looking rocky, particularly as unemployment rises further. But there is also some sunshine - real wage growth, stage 3 tax cuts and interest rate cuts (eventually) are expected to spur consumer spending later in 2024 and into 2025. Throwing a spanner in the works is the slowdown in population growth working through – mostly as the post-COVID catch-up runs its course. With per capita spending stagnating or contracting for the last seven consecutive quarters, more moderate population growth risks dampening the retail recovery.

The Fair Work Commission’s decisions on the 3rd of June to increase the minimum and award wages by 3.75% are something of a double-edged sword for the retail sector. On the one hand this will provide a modest further boost to real wage growth for consumers, supporting the economy’s capacity to spend. On the other hand, the increase is higher than the retail sector was suggesting, and will place some businesses under further financial pressure, at a time when retail and hospitality insolvencies are already rising.

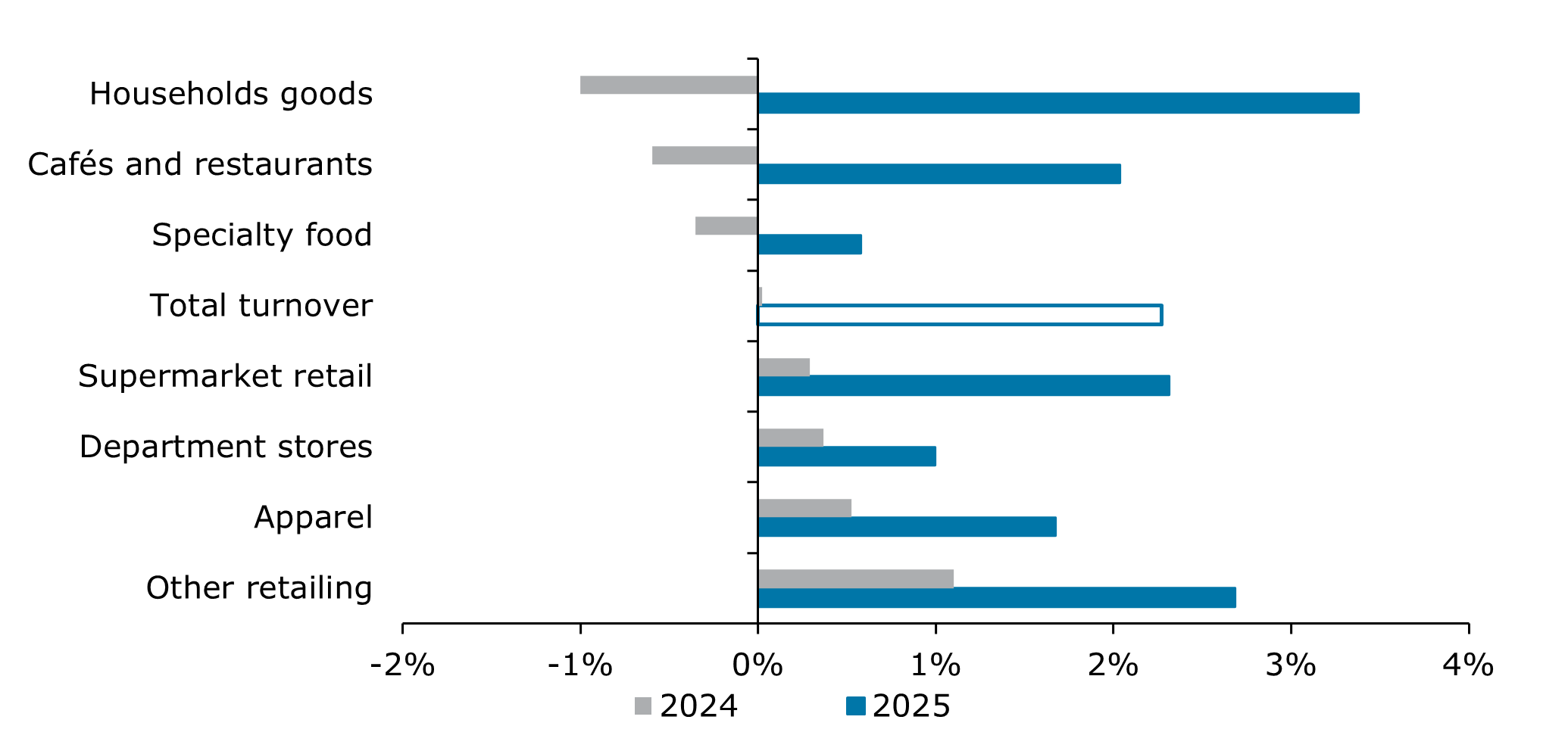

Despite the uncertainties ahead, real retail turnover is expected to increase from 0.0% in calendar 2024 to 2.3% in 2025. Household goods turnover should pick up more with better economic conditions and with an uplift in national building activity, supported by the Government’s ambitious housing targets. The additional dollars from tax cuts later this year may bump up spending at cafes, restaurants and takeaway in the September and December quarters.

Chart 1: Real turnover by category, 2024 and 2025

Source: Deloitte Access Economics, ABS Retail Trade.

This newsletter was distributed on 5th June 2024. For any questions/comments on this week's newsletter, please contact our authors:

This blog was co-authored by Shannon Cutter, Manager at Deloitte Access Economics

Click on the links below to read our previous Weekly Economic Briefings: