Although price growth is contained, cost of living pressures remain

A slowdown in price growth does not mean that the cost-of-living crisis is over. For many Australians, it remains very much a reality.

Today’s consumer price index (CPI) release shows Australia’s policy settings must shift from containing inflation to stimulating economic growth to lift Australians’ living standards.

Headline inflation rose by 0.7% in the June quarter, bringing the annual rate to 2.1%. The trimmed mean – the Reserve Bank of Australia’s (RBA's) preferred measure of underlying inflation – decelerated to 2.7% over the year to the June quarter, down from 2.9% in the year to March and consistent with the RBA’s latest forecast of 2.6%.

The June quarter saw a slowing in both goods and services inflation, with annual goods inflation at 1.1% and services inflation at 3.3%. Although services inflation remains significantly higher than goods inflation, it is experiencing its slowest growth rate in three years. A 10% decline in fuel prices over the past year contributed to the moderation in goods inflation, while the taming of services inflation was attributable to slower insurance price inflation and stabilising rents.

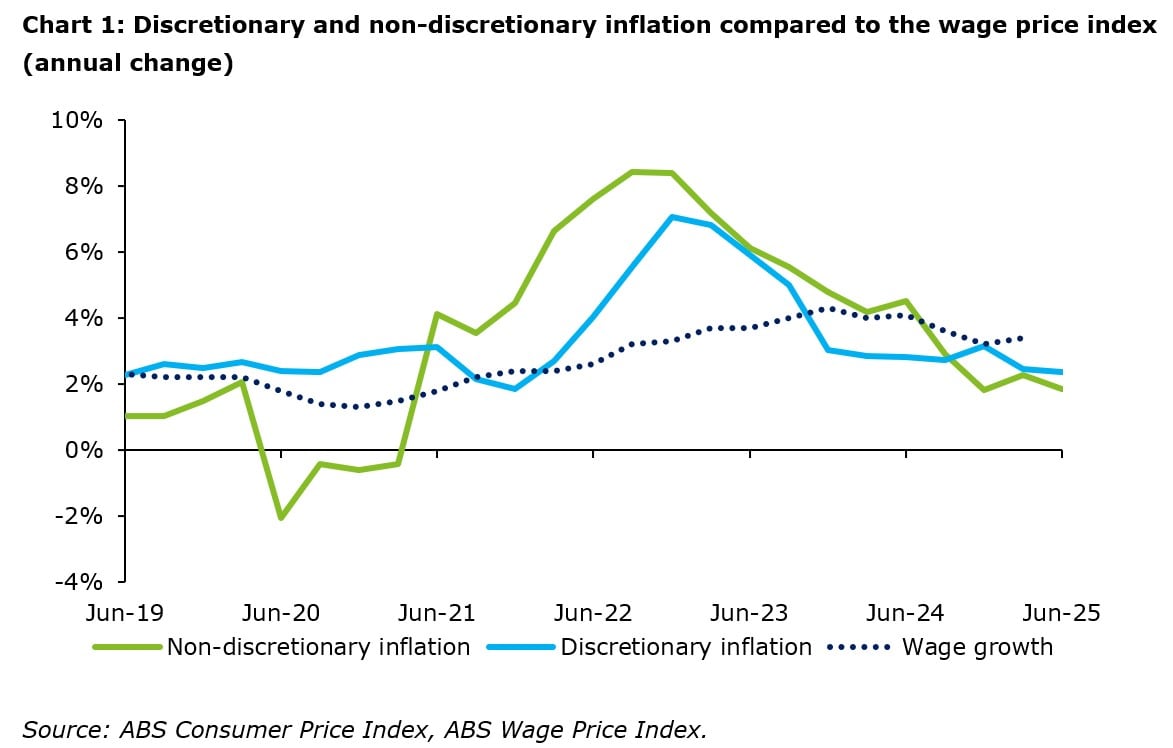

In good news for households, annual price growth for non-discretionary goods and services eased from 2.3% to 1.8% in the June quarter. In comparison, annual price growth for discretionary goods and services decelerated more modestly, from 2.5% to 2.4%. Throughout the period of elevated inflation, price growth for non-discretionary goods and services outpaced that of discretionary goods and services, making it more difficult for households to avoid the effects of higher price growth.

Even with inflation easing and sustainably back in the RBA's target band, the reality is that the cost-of-living crisis is not over. Prices are still increasing, just at a reduced pace. The significant rise in price levels from the post-pandemic period is still being felt, especially by low income earners.

Low income earners typically have smaller savings buffers, spend a higher proportion of their income and proritise non-discretionary purchases. Elevated prices have therefore left little room to re-arrange the household budget.

Indeed, this is evident in indicators of financial stress. Despite inflation cooling from 3.8% in the June quarter of 2024 to 2.1% in the June quarter of 2025 and two rate cuts in early 2025, low income households remain under financial strain. According to NAB’s Stress Index, stress levels for individuals earning up to $50,000 showed little change over the past year, while financial stress for the average Australian declined.

The reality is that falling real wages have eroded households’ purchasing power and lowered their standard of living over the past few years. While real wage gains have started to re-appear, it will take several years before workers recoup the living standards lost as a result of elevated inflation.

The June quarter inflation results largely track with the RBA’s forecast, and should support a cut to the cash rate in August. Not only is underlying inflation continuing to move to the midpoint of the RBA’s target band, the current cash rate of 3.85% is still well above the RBA’s estimate of the neutral cash rate.

In other words, the bank knows its monetary policy settings are restricting growth. This is becoming increasingly harder to justify given ongoing global economic volatility and the continued sluggishness of the Australian economy.

This newsletter was distributed on 30th July 2025. For any questions/comments on this week's newsletter, please contact our authors.

This blog was co-authored by Amy Kerrigan, Graduate Economist at Deloitte Access Economics.

Click on the links below to read our previous Weekly Economic Briefings: