WA Index

Issue 226 | May 2024

Welcome to the 226th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices

The aggregate market capitalisation of Western Australian listed companies increased by 0.8% during the month of April to close at $384.6 billion. Commodities such as base metals were a large driver for the positive performance.

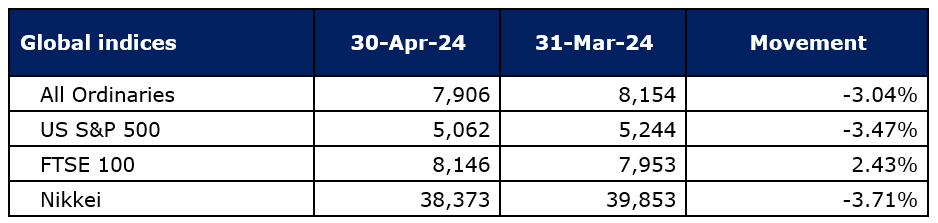

The tracked indices showed mixed signals comparative to the WA market, led by a 2.4% increase by the FTSE 100 while the S&P 500 registered a decline of 2.5%. The FTSE 100 performed strongly in April 2024, following UK inflation declining to below that of the US, fueling expectations a rate cut could arrive in the UK well before the US.

Download the list of WA’s top 100 listed companies, as of 30 April 2024, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

Commodity review

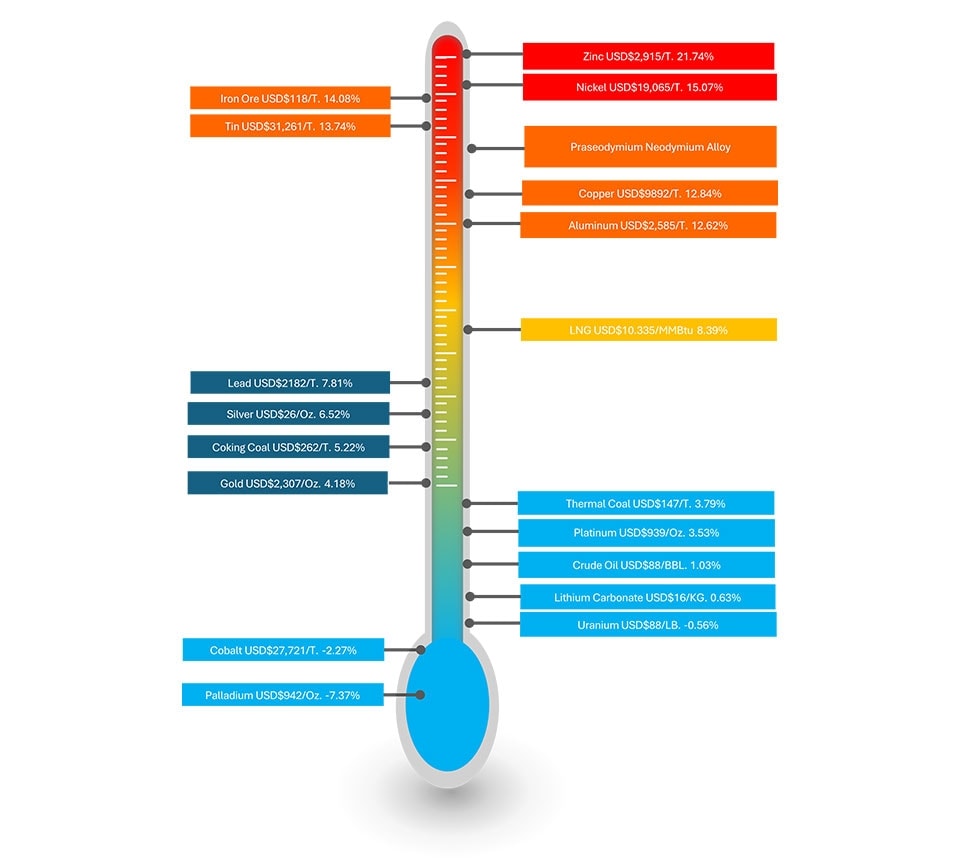

Global commodity indices have performed well in the month of April in particular across gold and the base metals space. This is the result of continued global uncertainty in the face of interest rate changes, increased manufacturing activities within US and China, and the LME imposing a ban on Russian metal produced on or after the 13th of April, namely benefitting zinc, nickel, tin and copper.

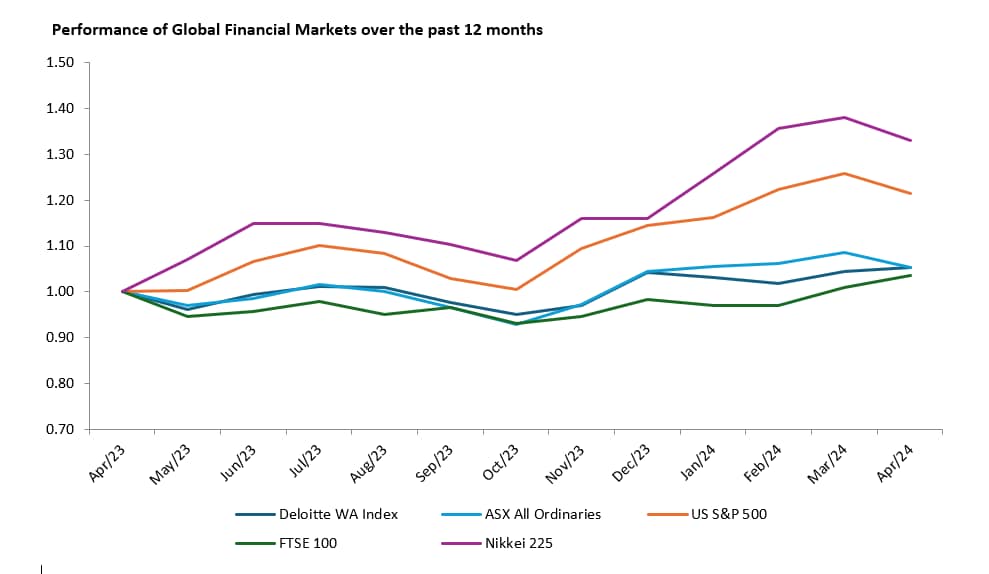

Performance of WA Index and Global indices

WA Index movement

Top 20 performers of the month

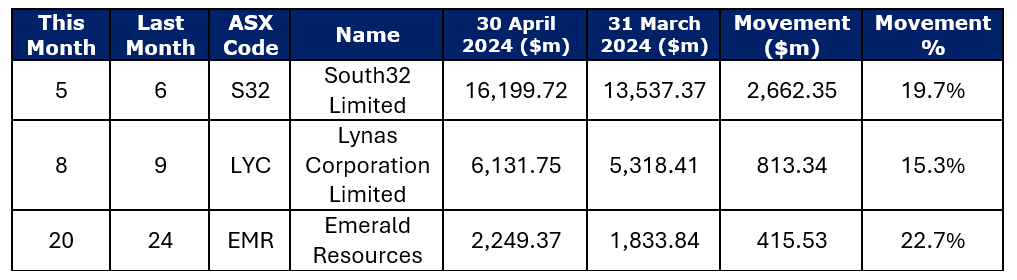

South32 Limited (ASX: S32) over the month of April South32’s market capitalisation finished up 19.7% with a share price of $3.59. Q1 results were released and provided some reassurance to the market, with unit cost and production cost guidance largely maintained. The share price held strong as base metal prices ramped up; set to benefit operating margins at Sierra Gorda, Cannington and Cerro Matoso.

Lynas Rare Earths Limited (ASX: LYC) Market capitalisation for April increased 15.3% as Hancock Prospecting increased its stake in Lynas to 5.82%. The allure of consolidation in the Rare Earth space was enough to interest the market and see market capitalization growth for the month despite reduced sales in Q3 FY24.

Emerald Resources NL (ASX: EMR) market capitalisation increased 22.7% and finished the month with a share price of $3.54. In April the longwinded takeover battle for Bullsye concluded – with the previous offer becoming unconditional and compulsory acquisition of remaining Bullseye shares taking place. Q1 results were released during the month, which showed strong cash generation and retained full year guidance for production and an AISC of US$780-US$850/oz.

The top 100 performers of this month were

WA1 Resources Limited (ASX:WA1) market capitalization had increased by 59.1% during the month of April. The increase was due to the market’s response to the announcement of continued exceptional assay results from the West Arunta Project on 28 March 2024 indicating shallow high-grade blanket of niobium mineralization at Luni. On 26 April 2024, a second announcement confirmed mineralisation extended east and south-easterly, and indicated potential for REE mineralisation. The market now awaits the return of metallurgical testwork on the project, and the initial mineral resource on the project.

Qoria Limited (ASX: QOR) has seen an increase in market capitalization of 50.2%. This was following the non-binding indicative proposal Qoria Limited received from K1 Investment Management proposing to buy 100% of issued capital at $0.40 per share. The board had unanimously rejected this proposal the following day. Buoyed by the attraction of possible increased bidding, the market capitalization remained strong. On the 21st of April, Qoria announced to market the divestment of Migiri, with anticipated reductions in marketing and operating costs by $3.2 million. The announcement also outlined early settlement of deferred consideration for a historical acquisition– utilising the strong share price to settle the consideration in scrip rather than cash.

Base Resources Limited (ASX: BSE) has seen the largest movement out of the top 100 performers with an increase in market capitalization of 117.4%. This movement was due to the market’s reaction to the Scheme Implementation Deed that BSE has entered into with Energy Fuels (EFR), ultimately resulting in EFR acquiring 100% of issued shares at an implied offer price of $0.302.