WA Index

Issue 227 | June 2024

Welcome to the 227th edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices.

The aggregate market capitalisation of Western Australian listed companies decreased by 2.2% during the month of May to close at $376.0 billion on the back of volatility across commodity markets and the de-listing of Azure Minerals, AVZ Minerals and Orecorp.

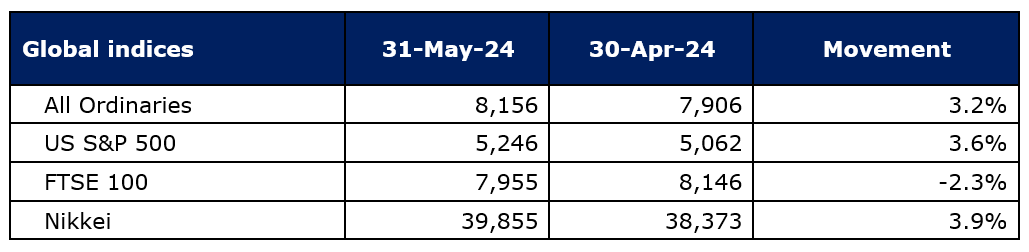

The tracked indices performed well in comparison, with the S&P 500 and Nikkei increasing by 3.6% and 3.9% respectively; with the US Market buoyed by strength in the technology sector. However, the FTSE decreased by 2.3%, with investors' fears over potential interest rate increases because of higher-than-expected inflation. Domestically, the All Ordinaries performed well in line with global markets, following the S&P and Nikkei by rising 3.2%.

Download the list of WA’s top 100 listed companies, as of 31 May 2024, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

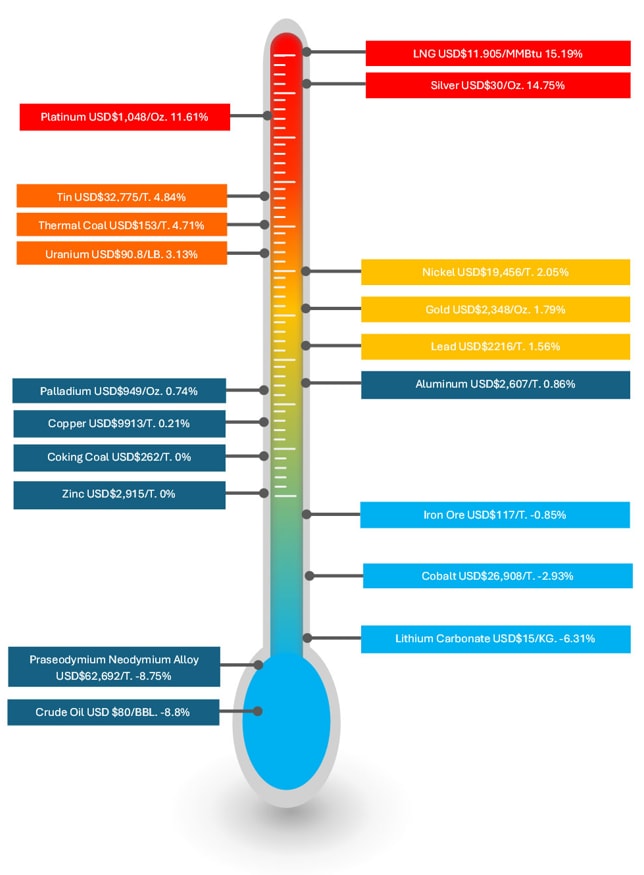

Commodity review

Commodity prices displayed volatility across groups, with various commodities, such as LNG and Platinum showing increases due to the current demand levels.

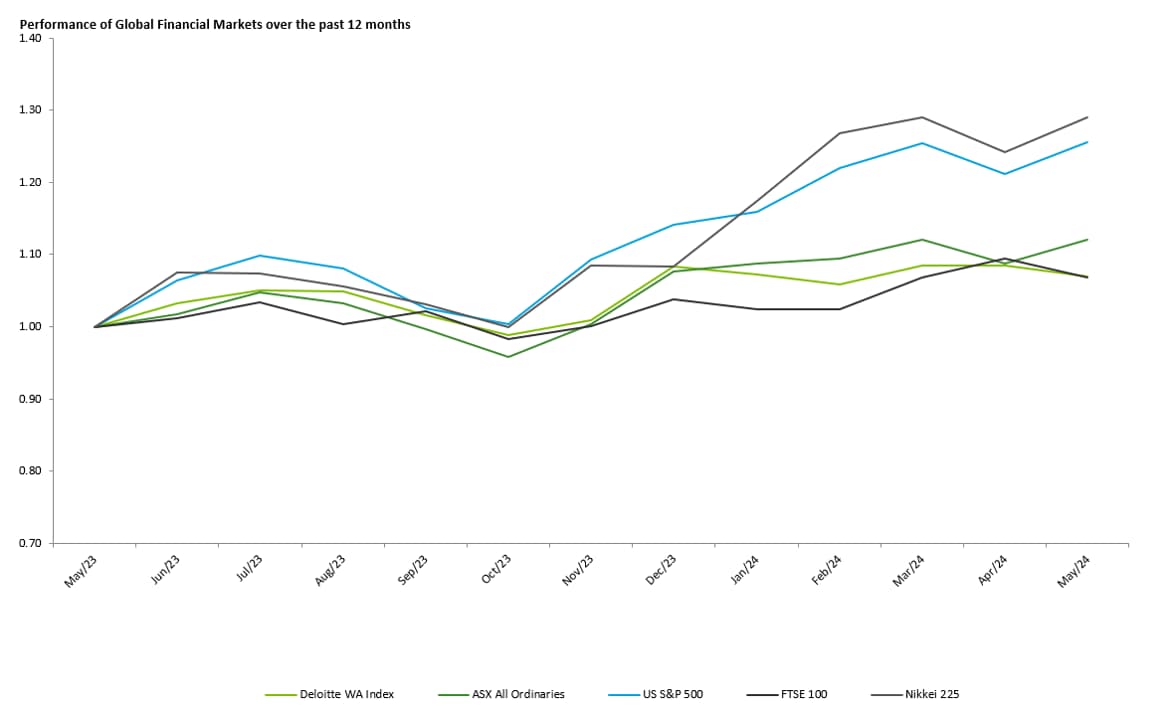

Performance of WA Index and Global indices

WA Index movement

Top 20 performers of the month

Paladin Energy Limited (ASX: PDN) Paladin Energy's market capitalisation saw a 14% increase during May. This growth is largely driven by the rising demand for nuclear energy as part of global decarbonisation efforts. Notably, China's demand for nuclear energy is expected to rise significantly, from 15% to 33% of the global total by 2040.A key factor in Paladin's strong performance is the restart of the Langer Heinrich mine. With this mine back in operation, with a 20 drums per day peak rate, Paladin is well-positioned to benefit from the increasing uranium prices.

South32 Limited (ASX: S32) During May 2024, South32 Limited (ASX: S32) saw its market capitalization jump by 10.6%. This boost came from a few key developments; with South32 acquiring a majority stake in the Chita Valley copper project in Argentina, advice released to the market noting the Illawarra Metallurgical Coal sale remains on track to be completed in H1 FY25 and released a FY25 capital expenditure update to the market advising $1.190 billion spend in FY25, broadly in line with analysts' expectations.

Bellevue Gold Limited (ASX: BGL) Market capitalisation increased 9.8% during the month, attributed to several positive developments and strategic initiatives announced by the company. Bellevue Gold announced they had declared commercial production; with the company on track to achieve production guidance for 6 months to June 2024 of 75Koz – 85Koz. The market responded given de-risking of the project through the ramp up phase, and with the company moving early to commence scoping level studies on mill expansion to 1.5Mtpa.

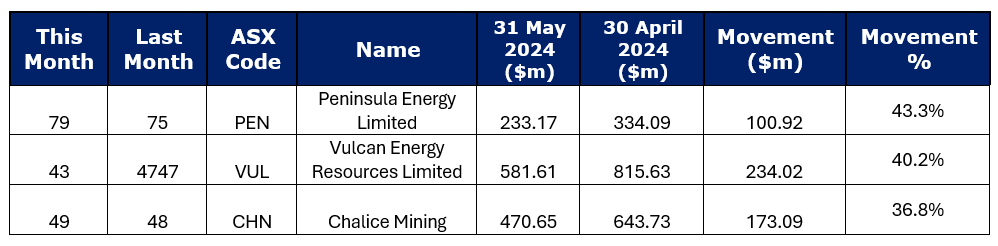

The top 100 performers of this month were

Peninsula Energy Limited (ASX:PEN) saw its market capitalisation grow 43.3% from April. This came post the completion of a $106m capital raise to develop the Lance Project; a Uranium In-Situ Recovery project in the USA with forecast capex to positive cash generation of US$52.2m. To fund the continued development Peninsula have continued discussion for debt financing with financial institutions and Government funding agencies while first delivery of produced yellowcake is anticipated for Q2 2025.

Vulcan Energy Resources Limited (ASX:VUL) saw its market capitalisation increase 40.2% during the month of May. The increase came on the back of the company announcing progress on its two-phase Project-level debt and equity financing, with Phase One now complete and significant interest from Government and financial investors outlined. The signing of anticipated agreements is slated for Q4 2024, with drawdown of funds expected in Q1 2025.

Chalice Mining Limited (ASX:CHN) saw its market capitalisation climb 36.8% from April. This came on the back of strength across some of the PGM commodities underpinning the project – with platinum prices up 12% in the month. Whilst these commodities have struggled longer-term in FY24, Chalice further released an updated Mineral Resource Estimate, in preparation for the Pre-Feasibility Study release in the current quarter; where the market will pay particular attention to pricing assumptions that brought into question previous scoping studies on the Julimar project.