WA Index

Issue 223 | February 2024

Welcome to the 223rd edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices

The aggregate market capitalisation of Western Australian listed companies contracted during January – decreasing 3.2% to close at $357.2 billion. The WA Index struggled in January due to its strong correlation to the commodities market. Commodities such as uranium provided some optimism in the largely dull, commodity heavy index. Opposingly, the majority of tracked indices experienced growth this month, led by a strong performance by Nikkei, registering a gain of 8.4% over the month, driven by shippers and financials, a reduction in US bond yields and exchange rate stability. The FTSE 100 was the only key index deteriorating over the month, down 1.3%.

Download the list of WA’s top 100 listed companies, as of 31 January 2024, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

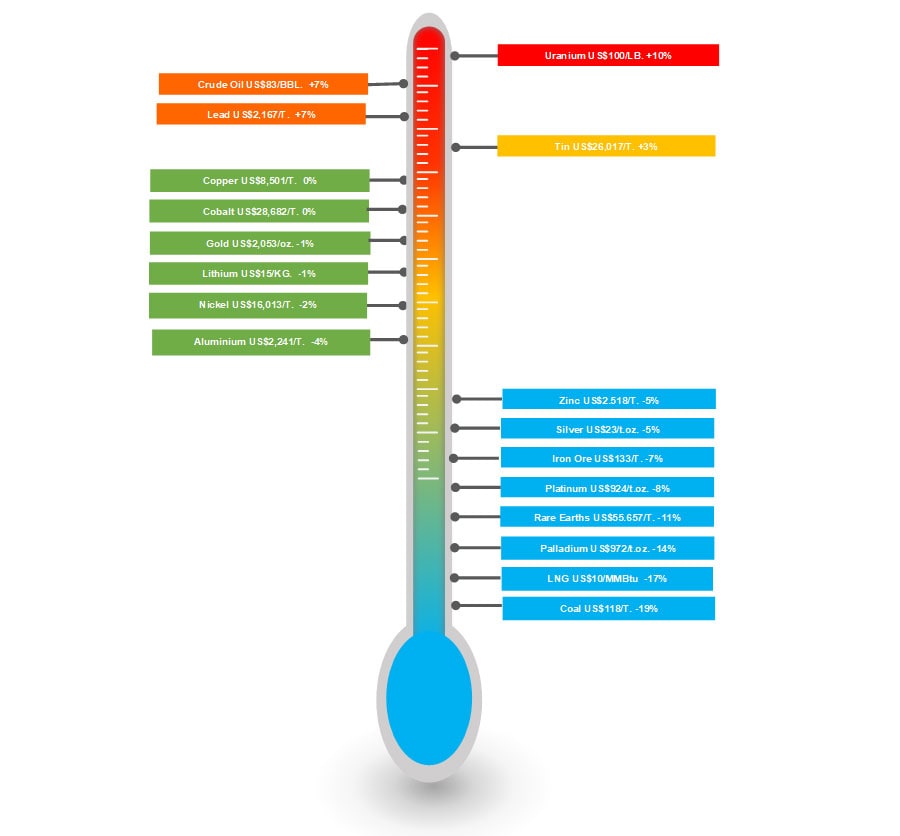

Commodity review

During January, commodity pricing exhibited mixed trends across key markets. Uranium continues to surge whilst other key resources saw a tougher start to the year.

Performance of WA Index and Global indices

WA Index movement

Top 20 performers of the month

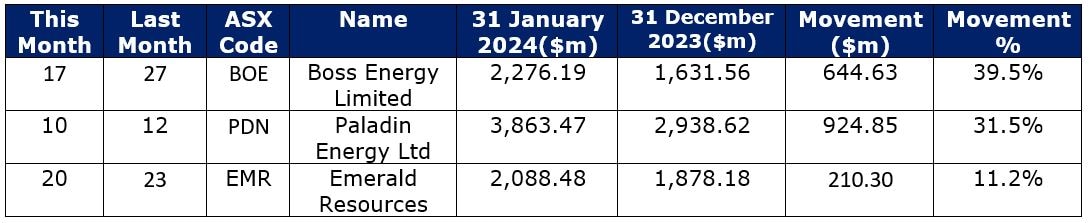

Uranium exploration and development companies dominated the top 20 performers as well as the movers and shakers in January, with many companies benefiting from the rise in uranium prices.

Boss Energy Limited (ASX: BOE) experienced the most significant increase in market capitalisation in the top 20 WA listed companies during the month. The company’s market capitalisation rose 39.5%, closing at $2.276b. This was brought about by several key announcements throughout the month including encouraging drill results from the Honeymoon Uranium project in South Australia.

Paladin Energy Ltd (ASX: PDN) saw a significant rise in market capitalisation within the month of January, rising 31.5% to $3.863b as the market reacted to positive news flow. The company executed a US$150m syndicated debt facility which will provide the company with capital flexibility as they recommence operations at the Langer Heinrich Uranium mine in Namibia. The company also released its positive quarterly results where it noted that first ore feed from the Langer Heinrich mine was processed through the processing plant on 20th of January.

Emerald Resources (ASX: EMR) extended on its rapid growth over the past year, closing at a market capitalisation of $2.088b on 31 January 2024, up 11.2% for the month. Strong exploration results continue at the company’s Bullseye Gold project and Okvau Gold Mine. Quarterly gold production from the company’s Okvau mine impressed the market, with the company noting it is on track to meet gold production guidance. The company continues in its efforts to takeover Bullseye Mining Limited, extending the date for Bullseye shareholders to accept the offer.

The top Deloitte WA Index Movers and Shakers in September

Peninsula Energy Limited (ASX: PEN) saw its market capitalisation more than double in the month of January, up 102.4% for the period. January saw the company complete a share purchase plan and placement. The total proceeds from the SPP and placement amounted to $60m. The funds received will be used to continue construction work and wellfield development to restart production at the Lance Uranium Project.

Bannerman Energy Ltd (ASX: BMN) benefited from the recent positive uranium market sentiment, with its market capitalisation rising to $554.8m as at January 31, up 35.3% for the month. Bannerman released its quarterly activities report which noted strong progress on the company’s Etango Project. The company also announced changes to its Board and key management personnel – with Gavin Chamberlain announced as the Company’s new Chief Executive Officer.

Deep Yellow Limited (ASX: DYL) market capitalisation grew 34% over the month, closing at $1.116b on 31 January 2024. January saw the company issue its December quarterly activities report – this report outlined the significant advancements the company made at its Tumas Uranium Project in Namibia including obtaining a mining license from the Namibian Ministry of Mines and Energy.