WA Index

Issue 222 | December 2023

Welcome to the 222nd edition of the Deloitte WA Index, a monthly review of Western Australian stocks and indices

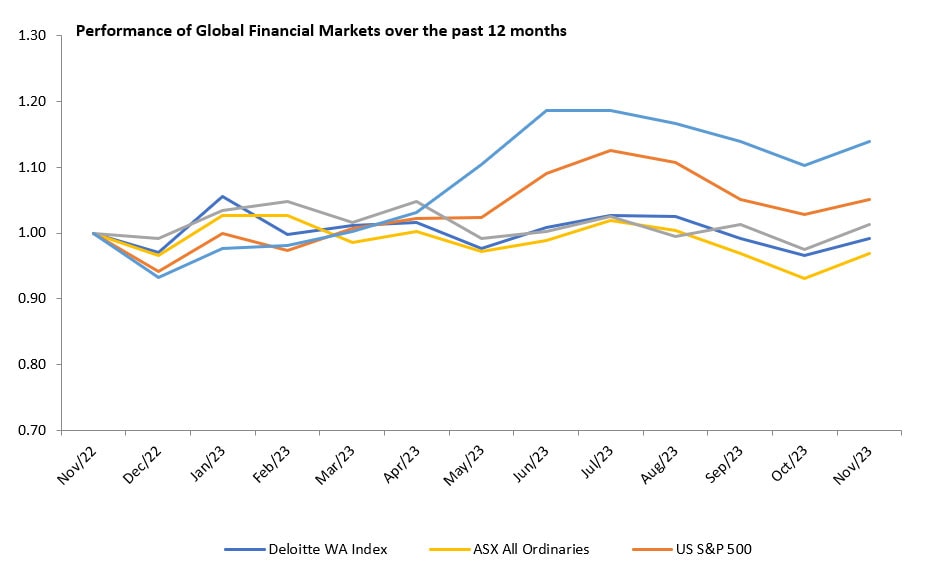

The aggregate market capitalisation of Western Australian listed companies stabilised during November – gaining 2.6% to close at $355.1 billion. All tracked indices experienced growth this month, led by strong performances for US S&P 500 and Nikkei.

Download the list of WA’s top 100 listed companies, as of 31 October 2023, explore the sections below, and if you do not currently receive our WA Index, please register to be added to our distribution list.

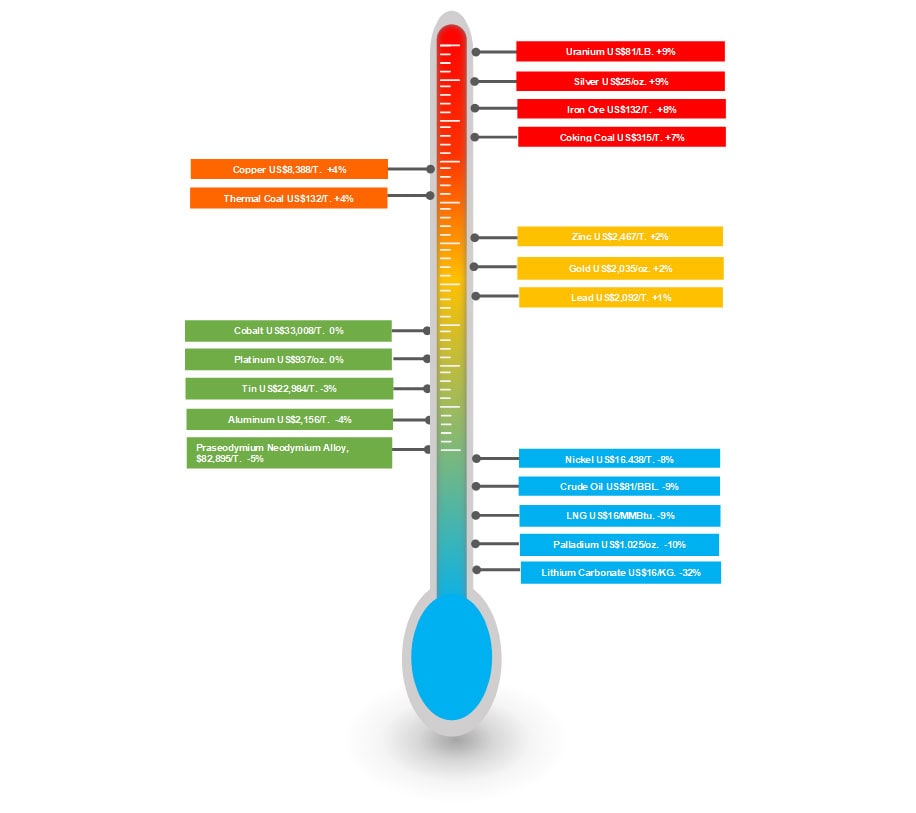

Commodity review

During November, commodity pricing exhibited mixed trends across key markets. Energy commodities have experienced a slight drop after notable surges for three months in a row.

Similar to the prior month, metals faced slowed movement amid weakening demand due to uncertainties around China’s stimulus measures; nickel, lead and aluminium slowed, with lithium carbonate experiencing another significant decrease, this month falling 32%.

Performance of WA Index and Global indices

WA Index movement

Top 20 performers of the month

Genesis Minerals Limited (ASX:GMD) experienced the most significant increase in market capitalisation in the top 20 WA listed companies during the month. The company’s market capitalisation rose 28.2%, closing at $2,006m. During the month, Genesis has announced the off-market acquisition of Dacian Gold Limited (ASX:DCN) and is proceeding with post-bid compulsory acquisition of all remaining shares not initially accepted in the takeover offer.

De Grey Mining Ltd (ASX:DEG) saw a further market capitalisation increase of 18.0% during the month, following an increase of 23.5% in the prior month of October. De Grey released a highly encouraging DFS at Hemi gold discovery, forecasting an average annual gold production of 530,000oz over the first 10 years for pre-tax free cashflow of $6.3 billion. First gold is expected in H2 2026.

Perseus Mining Limited (ASX:PRU) closed out the month with a 13.2% increase in market capitalisation, increasing to $2,650m. Perseus Mining has utilised a portion of its US$600 million cash reserve to acquire a significant stake in OreCorp, a competing African mining company, to block a bid from Canadian firm Silvercorp. Perseus now holds 19.9% of OreCorp.

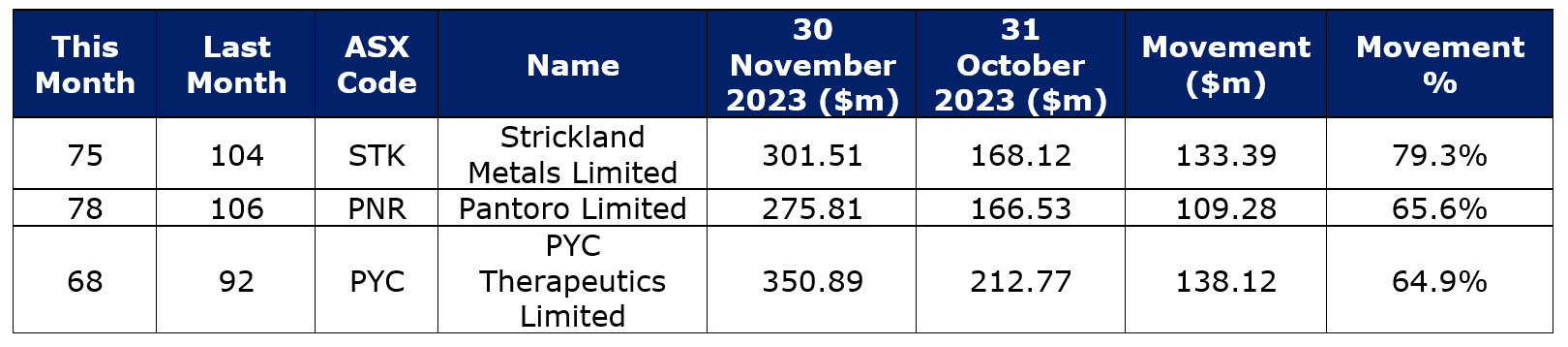

The top Deloitte WA Index Movers and Shakers in September

Strickland Metals Limited (ASX: STK) saw a market capitalisation increase of $133m in November, representing an increase of 79.3% from the prior month. Strickland this month had promising gold drills at its Marwari site, including 31m at 5.6 grams per tonne, with further RC drilling announced throughout the month.

Pantoro Limited (ASX: PNR) market capitalisation climbed by $109m in November, representing an increase of 65.6% on October numbers. Announced in November included the binding agreement to sell lithium and base metal rights at its Norseman project to Mineral Resources for $60m. Included in the consideration was $30m cash, a deferred payment of $30m upon the announcement of the final investment decisions, and net smelter and lithium use royalties.

PYC Therapeutics Limited (ASX: PYC) rose 64.9% in November, raising its market capitalisation by $138m from October. The main growth came on the back of announcements relating to ongoing medicinal trials. Notable updates on these trials include the completion of dosing in a second patient cohort with a blinding eye disease, and the development of a drug candidate for patients with end stage renal failure, showing efficacy in human models.