Deloitte Access Economics Retail Forecasts

Pincer movement

29 May 2026: Australian retailers are being squeezed from both sides, with slowing growth, falling real wages and record-low consumer sentiment putting the brakes on turnover growth, while conflict in the Middle East is compounding already elevated inflationary pressures on retailers’ costbase.

According to the latest edition of Deloitte Access Economics’ quarterly Retail Forecasts, increases to fuel, gas, fertiliser and plastic prices due to the Middle East conflict could lead to a 2.1% increase in the Australian retail cost base1 on top of the inflation the economy is experiencing anyway.

Releasing the report, Deloitte Access Economics Partner and principal report author, David Rumbens, said: “Events over the first half of 2026 mean Australian retailers are facing a simultaneous attack from both flanks – rising costs and weakening demand.

“The Middle East conflict is pushing up costs as the prices of key inputs including fuel, energy, plastics and fertiliser rise. At the same time, the rising cost of living is once again squeezing household budgets, dampening the outlook for consumer spending.”

April’s inflation print suggests the effects of the conflict-driven global energy shock are starting to flow through the Australian economy, adding to price pressures. Underlying inflation rose to 3.4% over the year - well above the Reserve Bank’s target band.

This edition of Retail Forecasts calculates the average projected increase to the Australian retail cost base as a result of the conflict through an analysis using ABS Input Output (IO) tables, assessing the direct increase in the cost of doing business for retailers, as well as the impact of rising upstream costs like freight, wholesale costs and raw materials on retailers' cost of goods sold.

David Rumbens said: “Rising cost pressures in the sector are presenting a key strategic decision for retailers around what to do about prices and margins. Research suggests retailers typically pass cost shocks on to consumers relatively quickly during periods of high inflation.

“However, retailers also need to be aware that consumers can only take so much. Demand side pressures are threatening to bite. Rising inflation pushed the Reserve Bank of Australia to hike interest rates for the third consecutive time in May and has led to increasingly gloomy forecasts around the outlook for economic growth and real wages.

“March’s inflation print wiped out all the real wage gains Australian households had seen in 2025, with real wages down 1.3% in the year to March. In turn, recent months have seen some of the worst consumer sentiment readings on record with households increasingly worried about their finances.”

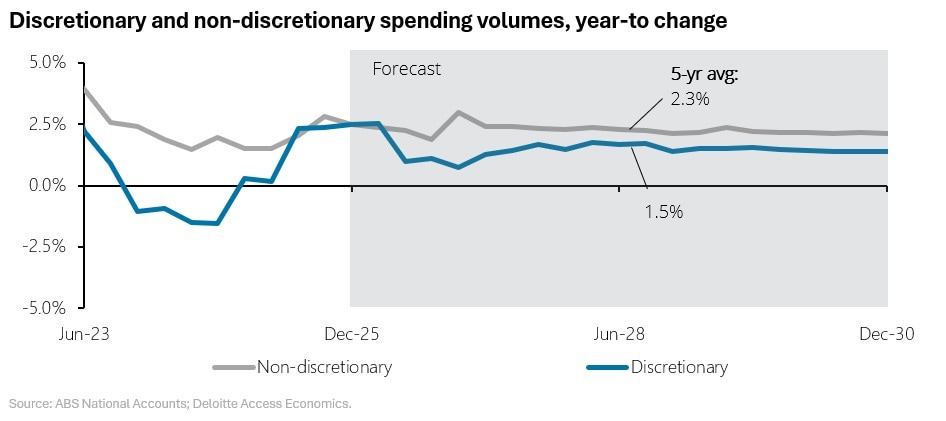

“Discretionary spending is likely to weaken further as the lagged effects of interest rate rises continue to flow through to household budgets, elevated inflation erodes consumers’ purchasing power, and uncertainty surrounding the Middle East conflict persists.”

Deloitte Access Economics expects discretionary spending growth will slow from 2.5% in the year to December 2025 to 0.7% in the year to December 2026. Non-discretionary spending on essentials is expected to increase from 2.5% to 3.0% over the same period but may subsequently pull back as households look to save money in any way they can.

David Rumbens concluded: “In this context, retail sector growth is set to moderate. In our baseline scenario retail turnover is expected to grow by 1.8% in 2026, down from 2.3% in 2025. Yet the risks are to the downside and should the crisis in the Middle East extend and amplify, consumer spending could see very little growth over the rest of 2026.”

1 Excluding fuel retailing

About Retail Forecasts

Retail Forecasts is produced quarterly and provides analysis of current retail spending and the economic drivers that influence this. It includes ten-year forecasts of retail sales by major category and of key economic drivers.

Download the executive summary

Further information (publications):

T: 1800 673 647

Email

Disclaimer

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. Please see www.deloitte.com/au to learn more.

Copyright © 2026 Deloitte Development LLC. All rights reserved.

Press contact(s):

Lachlan Moffet Gray

Media and Brand Communications

M: +61 413 739 290

lmoffetgray@deloitte.com.au

Media Enquiries

media@deloitte.com.au