Digital disruption for health plans: It isn’t coming, it’s here

An analysis of health tech investment trends shows that health innovators in three digital health categories—chronic condition management, care navigation, and digital benefits—are disrupting core health plan functions.

Executive summary

In our recent study, Breaking the cost curve, we predicted health spending as a percentage of GDP will decelerate over the next 20 years, driven by a move away from treatment and care toward well-being and prevention. Another study of ours shows that new entrants and health tech investors are pumping in record funds through venture investments, M&A, and initial public offerings (IPOs).1 Health care industry incumbents, which currently command the lion’s share of industry revenues, will likely be disrupted in this vision of the Future of Health, spurred by new business models, technologies, and consumer agency.

An analysis of health tech investment trends shows us that many health innovators in three digital health categories—chronic condition management, care navigation, and digital benefits—work to solve something core to health plans—affordability for their members. The nimble, consumer-focused, and tech-centric business models of these new entrants are already beginning to disrupt some health plans’ traditional business models.

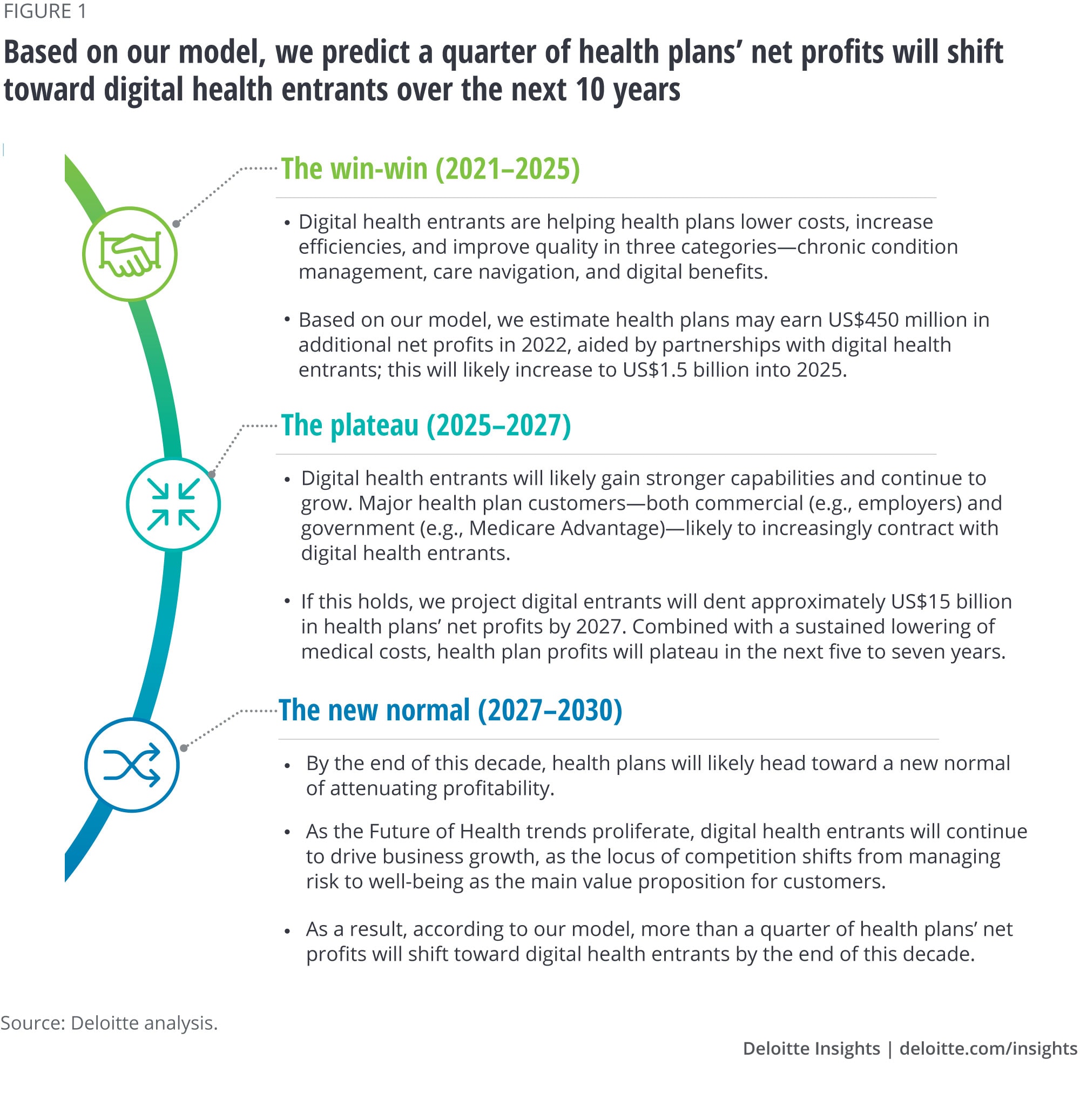

The new entrants in these categories have put in motion a set of changes that we predict will result in the shift of a significant share of net profits from health plans toward these digital business models in the coming decade. To test this hypothesis, we built an econometric model based on subscribed as well as publicly available government and industry data to quantify the financial disruption to health plans’ business through the end of this decade (figure 1).

Our analysis asserts that the moment of choice has arrived for health plans—the choice to evolve their core models, redefine the framework of their competitive landscape, and expedite capital deployment into market-ready innovation. Some leading health plans have already begun overhauling their business models to gain digital health capabilities. However, as the cost structure of care delivery shifts, with an increasing focus on well-being and prevention and personalized solutions, many incumbents may not realize that the locus of competition, for their core business of managing risk, is shifting rapidly toward wellbeing. A "wait and see" approach on evolving the core business might not be a viable option.

Introduction

Our past research focused on how health insurance is on the cusp of massive disruption that paves the way for the Future of Health. The rapid emergence and scaling of the digital health ecosystem—new business models, emerging technologies, and highly engaged consumers—are an example of how this disruption is already taking shape.

Digital health innovators (startups), along with leading incumbents and tech and retail giants, are building a digital health ecosystem centered around care, well-being, and consumer convenience. These players—at the intersection of health and technology—in many ways resemble several well-being, care delivery, data and platform, and care enablement archetypes laid out in the Future of Health vision.

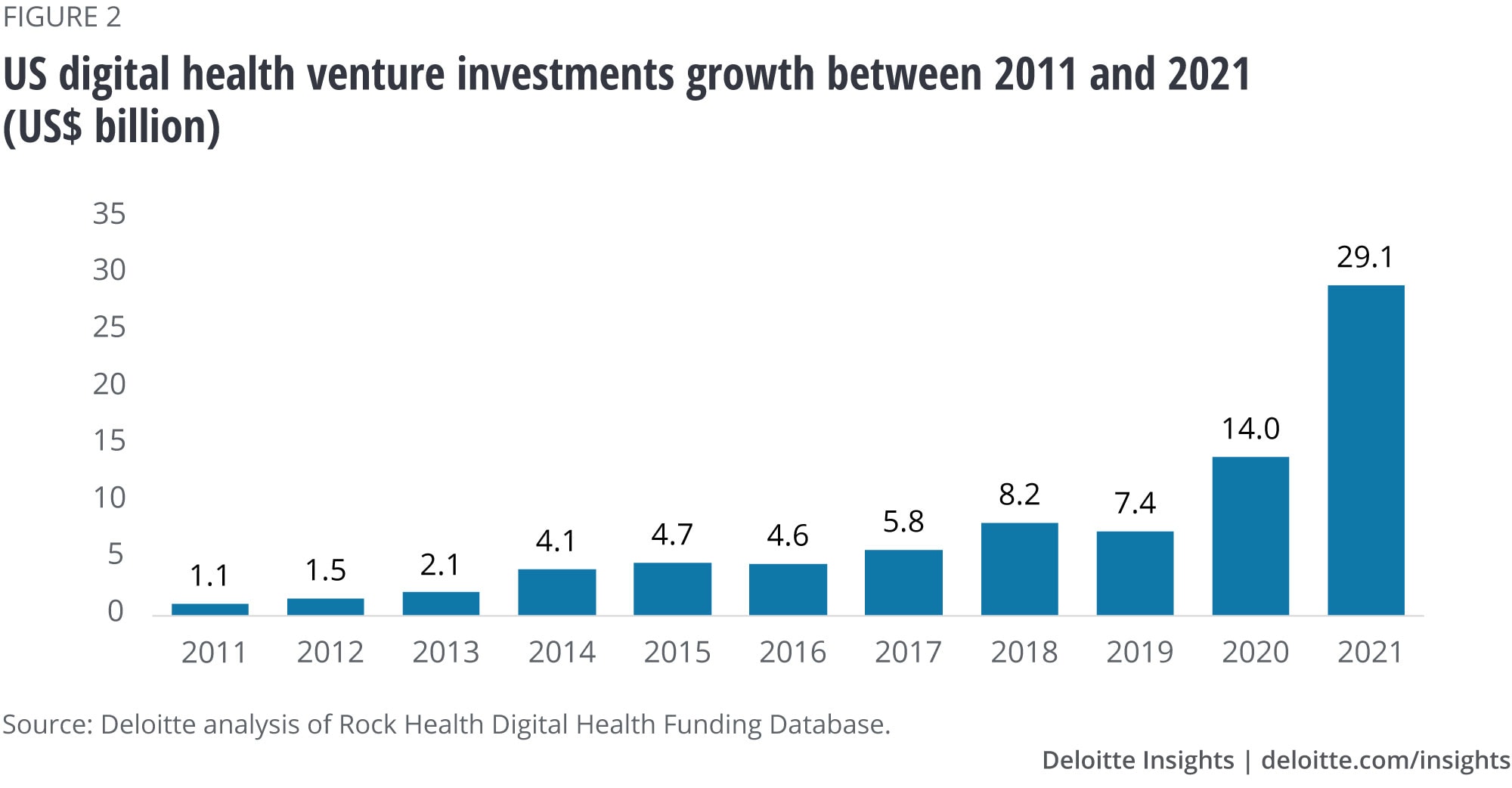

As a testament to the strength of the new-age business models, venture investments in digital health in 2021 stood at US$29 billion (almost double compared to 2020), according to Rock Health (figure 2). Apart from venture investments, heightened investment activities in the form of IPOs, M&A, and special purpose acquisition companies (SPACs) indicate broader investor and market confidence in the digital health ecosystem.

These digital health technologies are demonstrably bringing down health care costs and improving clinical outcomes as well as the overall consumer experience. In particular, health innovators in three digital health categories are working in the same realm as health plans.

- Chronic condition management: Sixty percent of adults in the United States have a chronic disease, according to Centers for Disease Control and Prevention (CDC).2 The health and economic burden of chronic diseases is nearly 20% of GDP.3 Digital health tools, including digital therapeutics, sensors and wearables, and remote patient monitoring, coupled with coaching and education are helping address condition-specific factors promptly and effectively. For instance, one of the leading digital innovators, using digital interventions and nudges, improved their diabetes members’ HbA1c levels by 0.8 points and helped them save US$1,900 per year.4

- Care navigation: Only one in 10 Americans has the health literacy necessary to navigate the complex US health care system, according to the Agency for Healthcare Research and Quality (AHRQ).5 Digital care navigation solutions that provide patient advocacy, member engagement, utilization management, and care coordination are helping consumers access quality, hassle-free care, while also helping employers save costs. For example, a digital care navigation innovator helped its employer clients reduce their yearly medical costs by US$976 per member through health advocacy, navigation, and personalized communications.6

- Digital insurance and benefits: One in every four dollars spent on US health care is wasted, and the biggest culprits are overpricing and administrative complexity, according to a Journal of the American Medical Association (JAMA) study.7 Digital insurance and benefits solutions that include self-service tools, paperless communications, process automation, clinical/EMR integration, and analytics-driven pricing offer cost savings and member satisfaction. Case in point: One of the digital insurers has a customer satisfaction rating that is three times higher than the industry average.8

The business models of these new entrants—nimble, consumer-focused, tech-centric—are beginning to disrupt health plans’ traditional models. We hypothesize that the new entrants in these categories will carve out both revenue and profits from health plans in the coming decade. To test this hypothesis, we built an econometric model to quantify the impact of disruption to health plans’ business (see the appendix for the methodology). The following section will discuss our findings.

More than a quarter of health plans’ net profits will shift to digital health entrants by the end of this decade

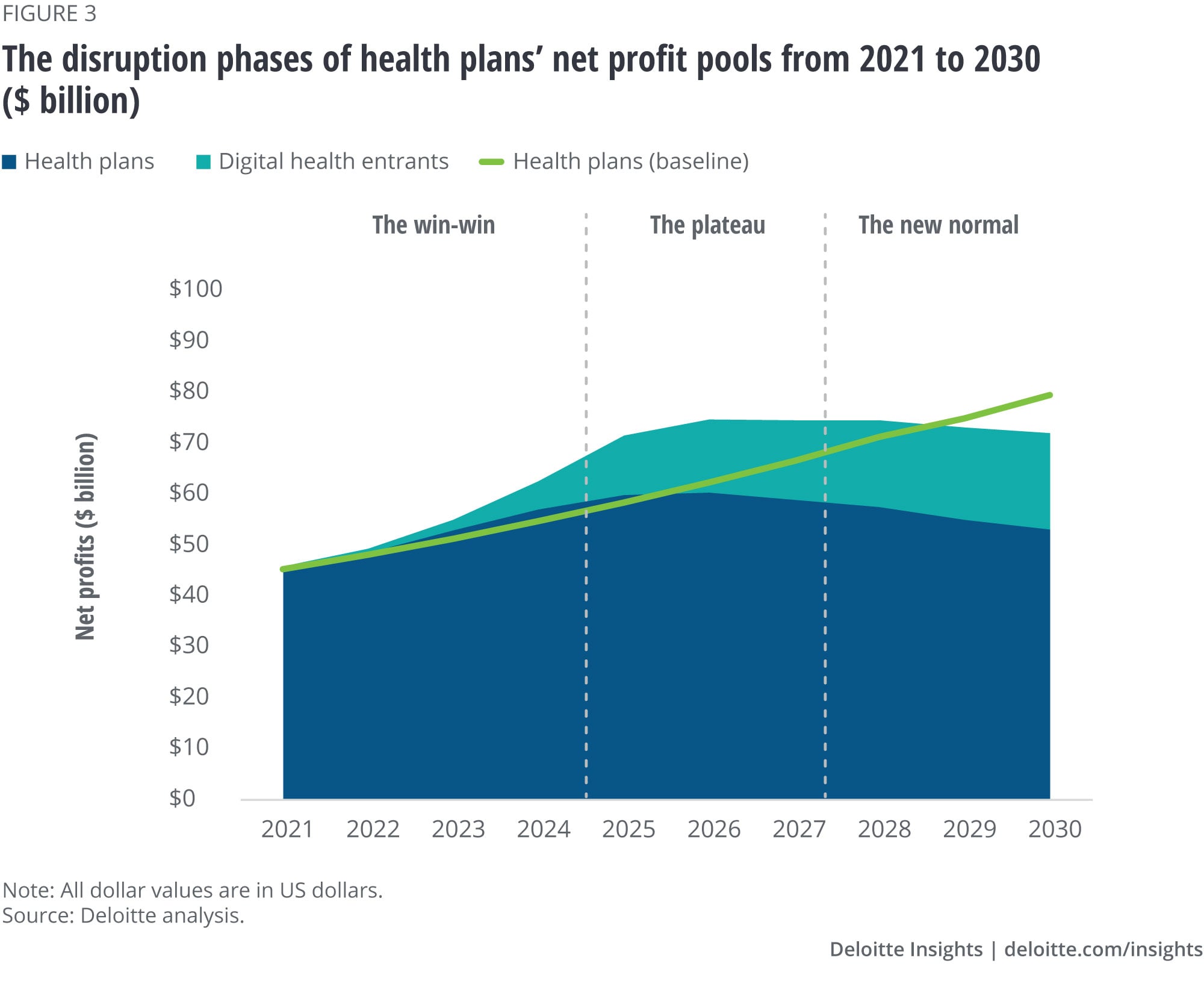

Based on our econometric modeling, we envisage that the impact of digital health on health plans’ net profits will fall into three distinct phases:

The win-win

Today, several digital entrants’ success is measured by how well they are helping incumbent health plans achieve their goals of keeping member costs down without impacting quality. For instance, diabetes, as a chronic disease, is one of the biggest cost burdens for many health plans.9 Over the years, health plans have built several ad-hoc diabetes management initiatives, but few have had the full desired impact. Digital innovators, using new approaches (e.g., a dedicated health coach), data (e.g., for personalization), and innovative technologies (e.g., real-time monitoring and intervention), have delivered quantified and consistent outcomes for health plans—reduced diabetes member costs and improved quality (e.g., by reducing BMI and HbA1c).

Apart from chronic condition management, innovators are also helping health plans with care coordination and offering other digital benefits. As a result, today, health plans are capturing the incremental profits due to muted claims costs and increased efficiencies. Based on our analysis, digital health entrants’ products will help health plans post additional net profits of US$450 million in 2022 compared to the baseline—what they are likely to earn without digital health; by 2025, this figure is likely to increase to US$1.5 billion (see figure 3).

The plateau

With consumer adoption of digital health technologies reaching critical mass in the next five years, many risks, especially for high-cost chronic conditions, may not be as prevalent as they are today. Digital health entrants are likely to gain stronger capabilities to detect disease sooner or even prevent disease altogether through proactive microinterventions.

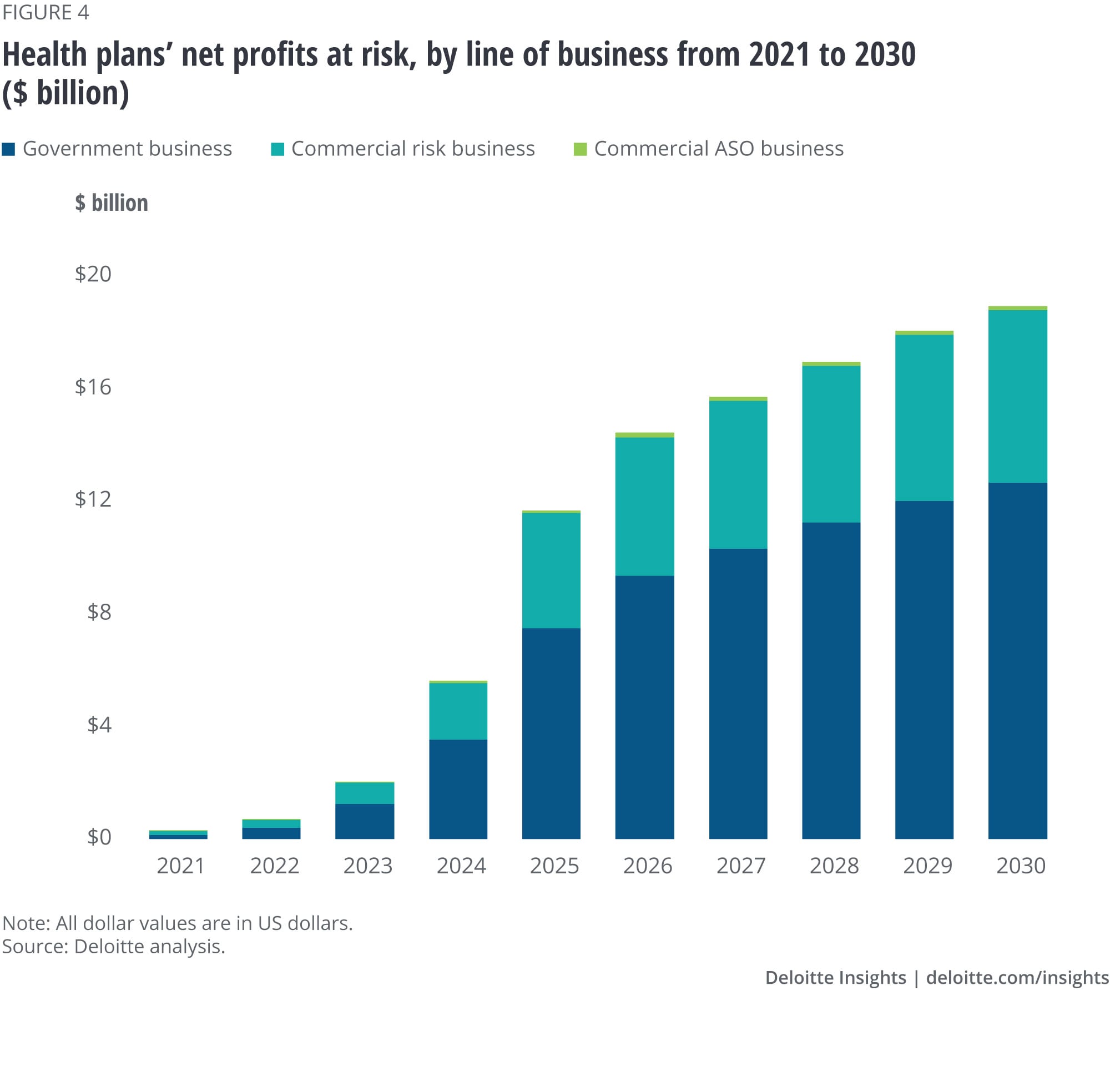

During this period (2025–2027), digital health entrants will continue to grow at the cost of health plans. On the commercial side, health plans may begin to lose more employer customers as employers increasingly desire to influence health outcomes and disparities and directly contract with digital health players.10 As these entrants succeed in maintaining members’ health and cost levels at scale, government programs, especially Medicare, may find them more compelling than traditional health plan contracts. If this holds, we project that by 2027, digital entrants will dent health plans’ net profits by approximately US$15 billion: commercial business by approximately US$5 billion and government business (Medicare, Medicaid) by approximately US$10 billion (see figure 4). Combined with the year-over-year impact of underlying medical cost trends, health plan profits will plateau in the next five to seven years.

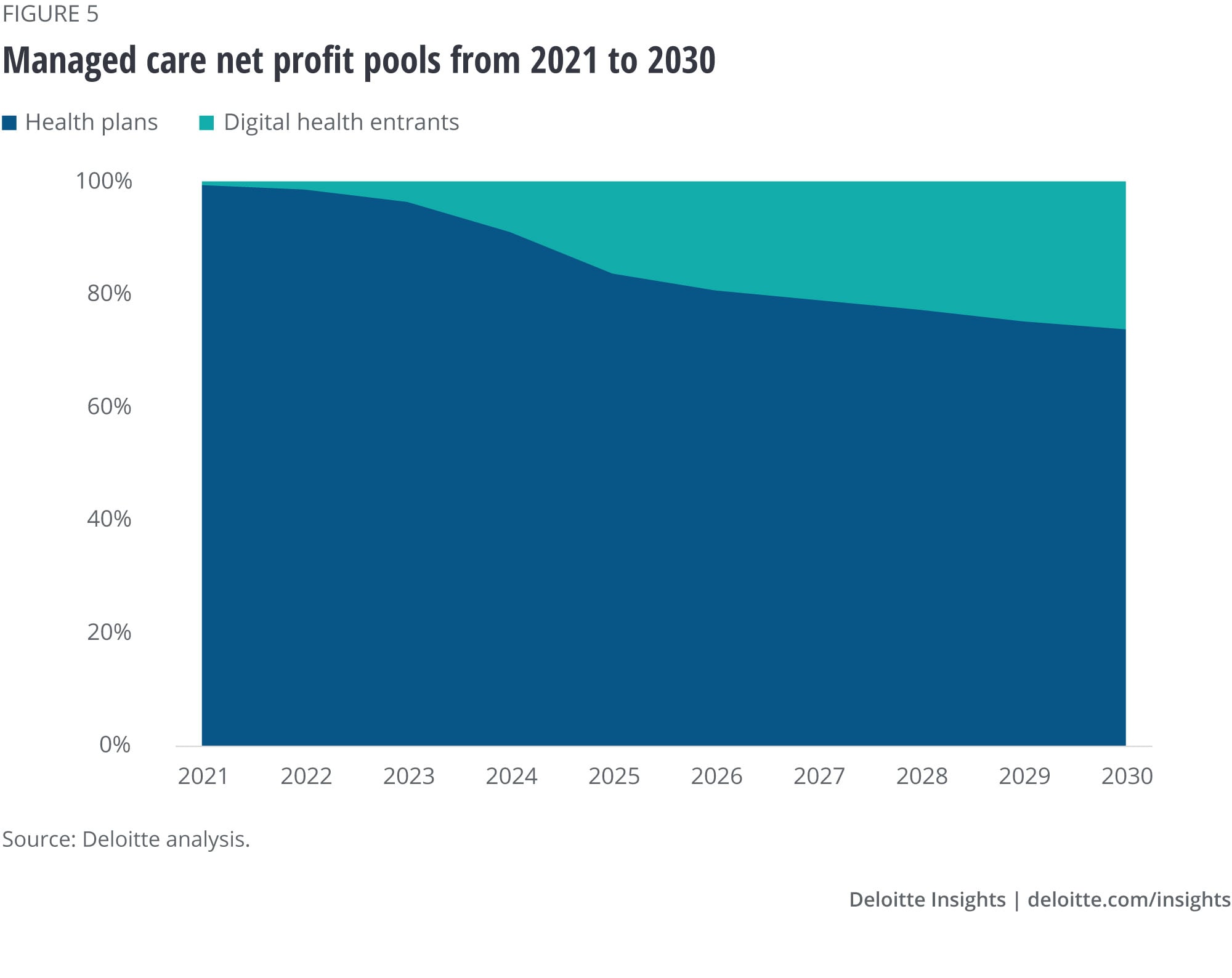

The new normal

By the end of this decade, health plans will likely head toward a new normal of attenuating profitability due to the confluence of two trends. First, as the Future of Health proliferates, the prevalence of high-cost health risks will likely shrink. Second, digital health entrants will continue to drive business growth, as the locus of competition shifts from managing risk to promoting well-being, and wellness features become a part of the total benefit value proposition for the client. As a result, according to our model, about 26% of health plans’ net profits will shift to digital health entrants (see figure 5).

When other industries realized the impact of digital disruption a tad late

Retailers and restaurants

Last-mile delivery is often a challenge for retailers and restaurants. If they do it right, it opens up avenues for business growth. In the past few years, online platform players such as Instacart (same-day grocery distribution) and DoorDash (on-demand food delivery) have aided grocery retailers and restaurants with last-mile delivery. Today, both platform players have a significant market presence, and the pandemic only fortified their business value; revenue for both grew nearly 300% year over year in 2020.11

On the face of it, this is a win-win for both incumbents (retailers and restaurants) and new entrants. However, many of the former may be ceding control on several crucial relationships, including with their customers. As discussed in our recent research, many retailers are developing partnerships with new digital players for data-driven services and experiences to create more value for their customers, but these strategies can lead to a profitability paradox in which they struggle to capture value in return.12 Some retailers are beginning to realize that they are in effect “competing with what they perceive to be a partner.”13 Working with Instacart means they become part of “a whole laundry list of retailers” available on the platform.14 Similarly, restaurants are also losing huge amounts to delivery partners—per-order fees are up from 5% in early 2000s to nearly 30% today.15

Additionally, the new entrants are expanding beyond their original solutions and diversifying their businesses. For example, DoorDash started on-demand grocery delivery in late 2020, and Instacart recently moved into prepared meals.16 As these companies increase their dominance, they are poised to become a much bigger threat to incumbents.

Banking and financial services

The proliferation of internet-based commerce since the early 2000s triggered merchant and consumer demand for efficient payment solutions. Banks were seen as the de facto go-to places for these solutions. However, startups such as PayPal, Stripe, and Block moved early into this rapidly disruptive segment of financial services, and now own significant market share (e.g., PayPal has 403 million active users; Stripe is the most valuable private fintech company).17

Many incumbent banking players have thus lost an opportunity to leverage new entrants as catalysts to evolve their core model. Moreover, the disrupters are also expanding into traditional banking services (e.g., lending, buy now pay later), posing a further threat to banks. To survive and thrive, many banks are increasingly partnering with these new entrants and using the experience and learnings to transform their business models.

Media distribution and production

Since its inception, Netflix has been proactive in embracing change, innovating, and adapting its strategies. It has disrupted many aspects of the entertainment industry. After pivoting from the online movie rental business, Netflix pioneered media streaming, forging a new channel of content distribution. For its streaming business, it grew manifold by partnering with/licensing content from incumbent movie and television studios.18 Many studios, with a new avenue to reach out to audiences, were happy to partner with Netflix. However, Netflix gradually forayed into content production, competing with large studios. Various factors—including rapidly shifting consumer preferences, technological innovations, and the pandemic forcing traditional movie theatres to close or making consumers averse to going out—have contributed to Netflix’s success. Today, it is a leader in the streaming business and not far behind on content creation, with operations in more than 190 countries and 214 million paying subscribers.19

Many studios were late to picture a partner morphing into a competitor. Once synonymous with entertainment itself, many studios are market-catchers today, with many introducing their own streaming services; but it may already be too late for some.20

The moment of choice is now

We are on the cusp of exponential growth in digital health, which, we estimate, will be instrumental in creating additional net profits of up to US$30 billion in managed care over the next five years. However, if health plan incumbents do not use new entrants as a catalyst to change the enterprise and evolve the core model (and instead, only view them as a different model), our analysis shows that many incumbents risk losing these dollars to digital health entrants. Health plans seeking to use digital health as a catalyst to win in the Future of Health should reframe their competitive landscape. A “fast follow” on what other incumbents are doing is not likely to lead to long-term success. Depending on the geographies, segments, and populations being served, incumbents can consider the following actions:

- Choose business models based on core competencies: As the cost structure of care delivery shifts toward well-being and prevention and personalized solutions, health plans should create differentiated modular products based on their core competencies. For instance, they could modularize well-being products in commercial segments for defined market segments, based on chronic condition, drivers of health, or subscription model. In addition, despite the increasing traction of digital health solutions in government programs (Medicare Advantage, Managed Medicaid), there is tremendous potential for health plans to play and win in this space. Through their current and potential contracts, incumbents have built-in advantages such as health care expertise to manage the complex needs of these populations, operational excellence on a large scale, and existing member relationships. This presents a unique opportunity to shape and win these businesses with digital-first, clinically integrated, customized, whole-person care management solutions.

- Understand the broadening horizon of competition: Health plans should realize their competition is no longer limited to peers in specific lines of risk business and geographies. New entrants, many of which are nimble, well-capitalized, and free from the constraints of traditional business models, are now their biggest competitors. These companies understand consumer preferences, offer different clinical models, and use digital technologies pervasively. It is essential for health plan leadership to acknowledge the broadening horizon of competition and shape their go-to-market strategies accordingly.

- Expedite capital deployment: Health plans should consider expediting capital deployment to access market-ready innovation in digital health and pilot market-ready solutions in targeted segments and geographies. They may need to create alliances and partner with or even acquire what might today be considered strange bedfellows: traditional competitors, digital health innovators, transactional sector companies, or organizations from other industries (technology, retail, life insurance, etc.).

Our analysis asserts that the moment of choice for health plans is now. Some leading health plans have already begun overhauling their business models to invest in digital health capabilities. However, many incumbents may not realize that an undeniable set of changes are already in motion, with the locus of market and competition shifting rapidly toward well-being: making it imperative to evolve the core health plan business, without much delay

Appendix: Methodology

Deloitte’s health care team built an econometric model to quantify the impact of digital health entrants on revenue and net profits of health plans. The model is based on forward-looking sensitivity analysis performed using publicly available information on historic data and forecasts such as the US Population Census, National Health Expenditure, SEC filings, IBIS reports, CB Insights reports, and industry analyst reports, among other sources. Baseline health plan net profits were also considered from publicly available historical health plan net profit data. We lay down the key considerations and assumptions of our model:

1. Considerations for the baseline revenue of digital health entrants

For this analysis, we considered three digital health categories that are focused on reducing health care spending: chronic condition management, care navigation and member engagement, and digital insurance and benefits/digital health plans. For the baseline, we utilized publicly referenced 2020 revenue estimates for the top five to 10 digital health organizations in each of these categories (“sample”), based on our analysis of data from CB Insights and Rock Health, and extrapolated it for the entire category.

2. Assumptions about the growth and profitability of digital health entrants

The model assumes the following for the sample organizations in the three categories:

- Chronic condition management: Revenue growth of 120% year over year until 2025, and 20% year over year thereafter. Net profit as a percentage of revenue may rise from 10% in 2021 to 25% by 2024 and remain constant thereafter.

- Care navigation: Revenue growth of 50% year over year until 2026, and 20% year over year thereafter. Net profit as a percentage of revenue may rise from 10% in 2021 to 25% by 2024 and remain constant thereafter.

- Digital benefits: Revenue growth of 50% year over year until 2026, and 20% year over year thereafter. Net profit as a percentage of revenue at 7% of revenue through 2030.

3. Factors considered to determine the influence of digital health entrants on health plan profits

This model assumes that digital health businesses will be decreasingly accretive to health plan profits (for the three digital health categories considered in this paper), and that risk-based profit pools will attenuate as a result of predicted impacts to medical cost trends.

- In 2021, we assume digital health entrant net profits were accretive to health plans by as much as 200%, declining to 100% in 2024, and to minus 10% by 2030.

- Health plans’ profits will likely begin to attenuate by about 7–8%, compared to baseline profits, beginning 2027.

Leveraging these assumptions and variables, we then performed sensitivity calculations on the potential growth and profitability of digital entrants to estimate the range of impact on incumbent health plans’ net profits.

Deloitte's vision for the Future of Health™

By 2040, there will be a fundamental shift from “health care” to “health.” The future will be focused on well-being and managed by companies that assume new roles to drive value in a transformed health ecosystem. As traditional life sciences and health care roles are being redefined, Deloitte is your trusted guide in transforming the role your organization will play.