2026 Global Telecommunications Industry Outlook

The industry is making new use of “flanker brands,” facing tough choices about its B2B strategy, and looking to grow trust and loyalty with consumers

These days, readers may anticipate outlooks filled with unprecedented events and shocking inflection points. Neither is true of telecom in 2026: it’s a mature industry, taking advantage of artificial intelligence like every other industry, and hoping to see new growth. But the opportunities and challenges of the next year are likely to look a lot like last year’s, and perhaps even like those of the last decade. Telecom will likely be a low-growth industry and with solid margins, driven mainly by providing basic connectivity, primarily to consumers.

Read more from the collection

TMT Outlooks

This outlook focuses on three themes:

- In 2026, “flanker brands” (secondary brands targeting a new segment to protect brand share) will likely evolve into strategic, digital-first growth engines, enabling telecom operators to sharpen segmentation, reduce churn, protect flagship brands, and expand across mobile, broadband, and emerging services.

- Telecoms face a massive but challenging opportunity to grow beyond connectivity into business-to-business tech services such as cloud, cybersecurity, and Internet of Things; however, they will likely have to overcome low margins, hyperscaler competition, and execution complexity to make the “techco” pivot (from being primarily a network provider to becoming a platform- and software-driven digital services company) pay off.

- As connectivity becomes commoditized and customer satisfaction erodes, telecom operators should consider shifting from product-centric models to value-driven ecosystems built on personalization, emotional relevance, proactive service, and seamless digital experiences in order to rebuild loyalty.

Telecom “fast facts”

Below, we’ve put together some “fast facts” that provide an overview of some important statistics that make up this critical—but sometimes underappreciated—industry:

- Telco stocks were up 15% in 2025, slightly less than the S&P 500 (18%) but well behind the NASDAQ (21%).1 North American telcos were down 2%, while Latin American and Caribbean telcos were up about 38%, with Asia Pacific increasing by 18% and Europe, the Middle East, and Africa by 28% to 30%.2

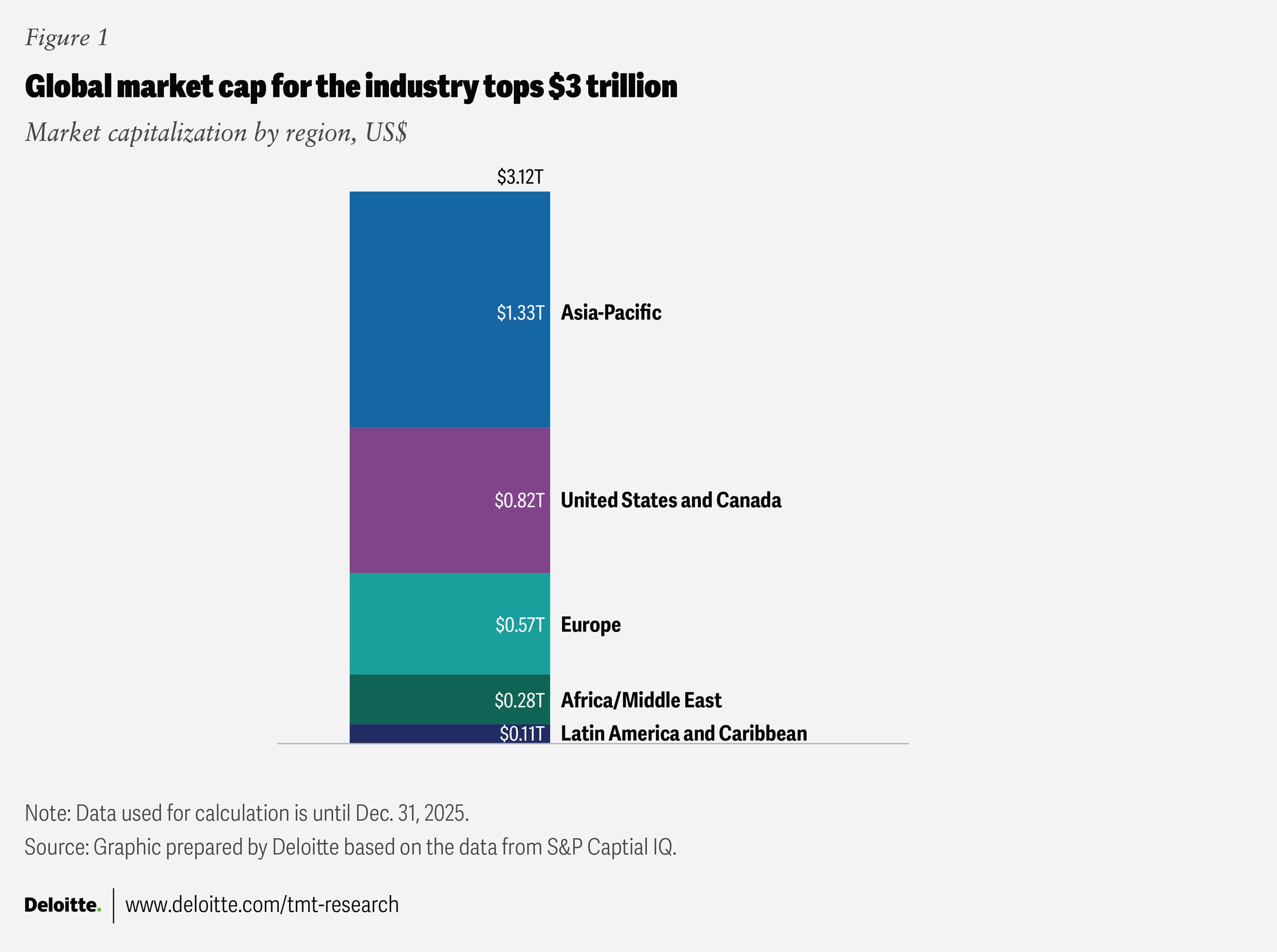

- Globally, the telecommunications industry is expected to generate revenue of about US$1.55 trillion in 2025, up roughly 1.7% from the prior year.3 By market cap, the sector is worth about US$3.1 trillion globally (figure 1).

- Global telecom operators continue to show broadly stable financial performance. Earnings before interest, taxes, depreciation, and amortization margins are stable at around 35%, capex intensity is also stable at around 18%, and average revenue per user remains largely stagnant, with only a minority of operators reporting growth, underscoring persistent pricing pressure and the fragility of mobile monetization in mature markets.4

- By the end of 2026, the global mobile industry association expects just under five billion people to have mobile internet access, up from 4.8 billion in 2025.5 Around 24 million jobs were directly supported by the mobile ecosystem in 2024.6

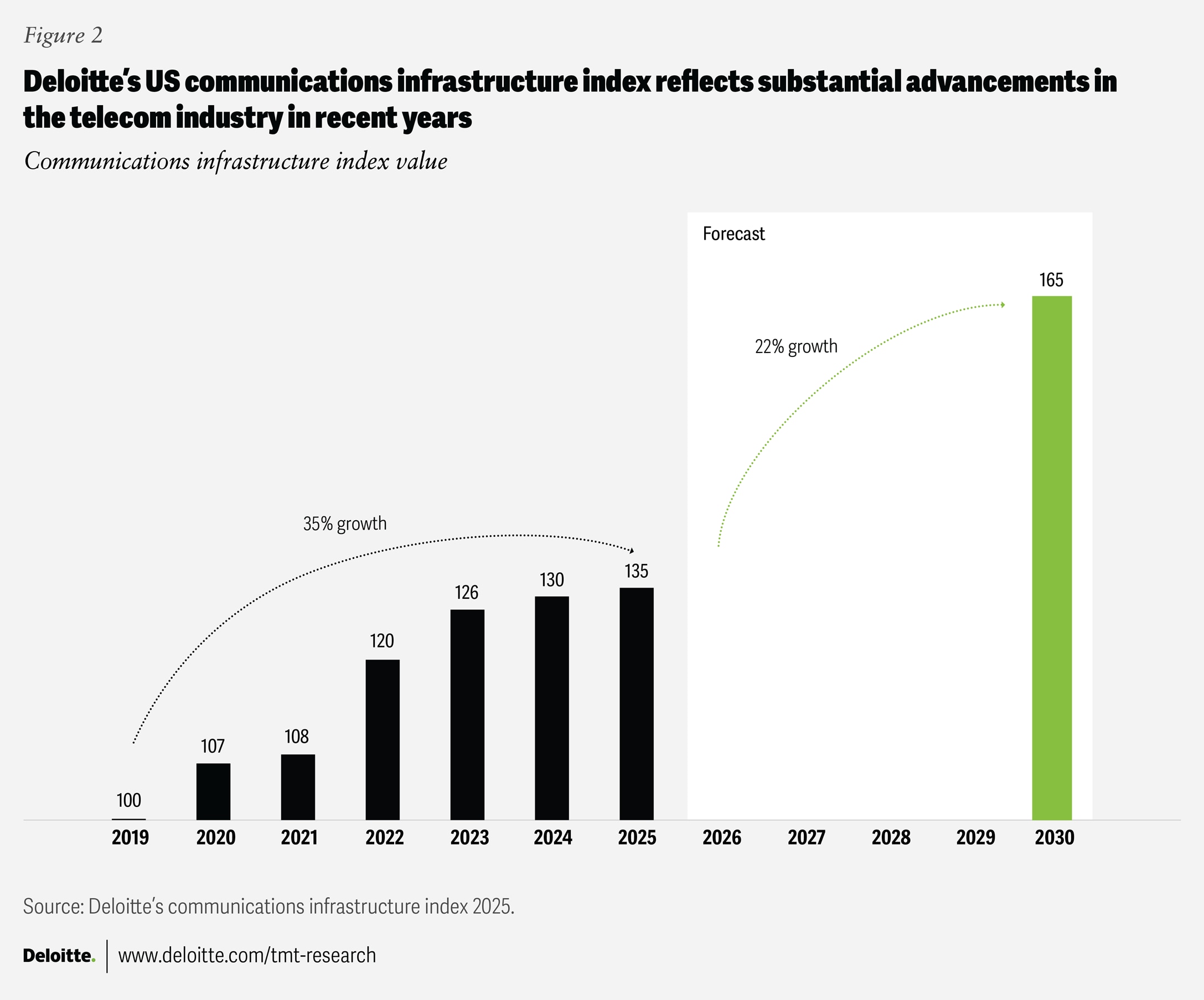

The US communications infrastructure index

Introduced in 2025, Deloitte’s US communications infrastructure index showed better-than-expected growth in 2024, up 3.2% compared to our expectation of a 1% rise, driven largely by increased wireless speeds and usage, in part due to growth in fixed wireless access (figure 2). It grew an estimated 4% in 2025.

Next-gen flanker brands are emerging as growth engines

Flanker brands are helping protect and enhance portfolio economics, stabilize markets, and support expansion across mobile, broadband, and evolving digital services

Across global telecom markets, a quiet shift is underway. Brand extensions that once played a relatively limited supporting role have become important tools for helping connect with price-sensitive customers, adding new digital services and features, and dealing with growing competitive pressures. Operators are now typically relying on these secondary brands to test new propositions, manage churn, and protect their flagship identities, often with leaner, more agile models than before.

A flanker brand is defined as “a new brand that is introduced into a category by a company and is designed to capture a different segment, with little overlap in consumers’ perception of the existing brand.”7 In the telecom space, flanker brands have existed since the mid-2000s,8 with Canadian telcos pioneering this strategy.9

Historically, telco flanker brands were positioned as low-price, low-feature brand extensions of flagship brands. As a result, they were often seen mainly as “discount” single-product brands and tended to make up a lower percentage of revenue than of subscribers. They frequently competed not with the carrier’s flagship brand, but with low-cost carriers and mobile virtual network operators. Further, they also tended to exhibit higher churn and lower margins.10

More recently, however, the role and design of flanker brands have evolved.11 A defining characteristic of modern flanker brands is business-model simplicity.12 What once differentiated flankers primarily as prepaid offerings has evolved into transparent, single-line pricing, fewer add-ons, and what-you-see-is-what-you-pay propositions,13 while also providing operators with low-risk environments to test new digital experiences, pricing models, and operating approaches before selectively scaling them across the broader portfolio.14

Flanker strategies can also carry risks that require careful management. Maintaining multiple brands can dilute marketing spending, fragment brand investment, and increase organizational complexity if roles are not clearly defined,15 making it essential for operators to tightly constrain flanker scope, channels, and propositions to avoid internal cannibalization.16

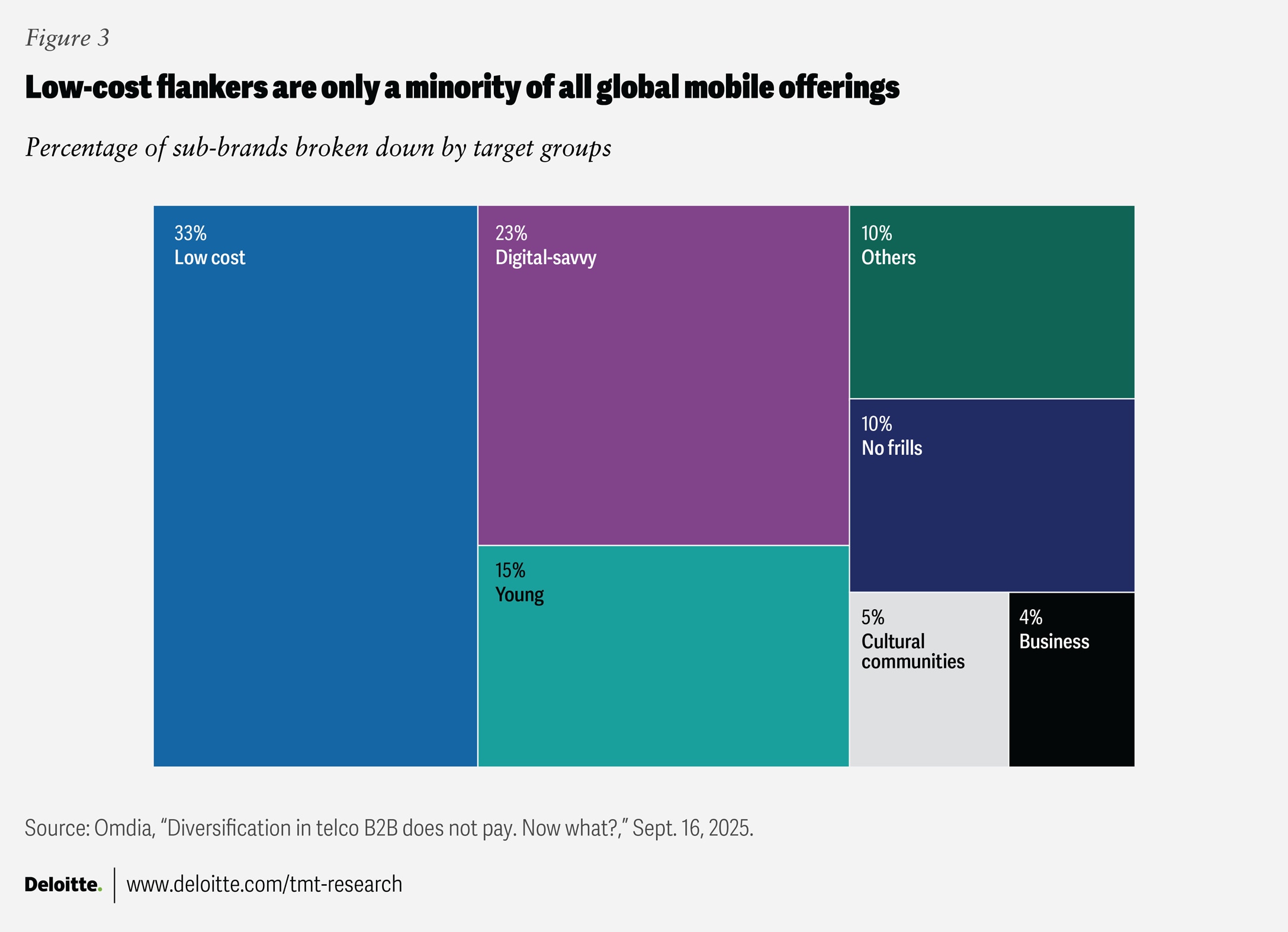

That said, flankers are widely used: over half of Western European mobile network operators use them, and they are about 10% of the subscriber base on average.17 But in some markets, flankers make up a more significant portion of both subscribers and revenue. In Canada, flankers account for 24% of revenues and 30% of subscribers for major carriers. In Switzerland, flankers account for 30% to 40% of the base,18 and in some developing world markets, they represent up to 23% of subscribers only 12 months after launch.19 While low-cost flankers are the single biggest category globally, other categories together account for roughly twice as many offerings (figure 3).

Flankers are not merely “low cost,” but can be tailored for a variety of market segments, including age; ethnicity, culture, or language; digital savviness; enterprise type; and more.20 Although they tend to have lower average revenue per user, they also typically have lower acquisition costs (50%) and operating costs.21 Moreover, flanker brands are evolving beyond their discount-focused origins into strategic market stabilizers that capture price-sensitive segments while insulating flagship brands from competitive erosion. Some operators now deploy digital-first flankers to deliver full telecom services through lean operational models, achieving margins that rival those of premium brands while targeting distinct consumer cohorts.22

What is new for flankers in 2026? First, more mobile network operators will likely offer them. Second, flankers may make up a higher percentage of subscribers and sales over time. Third, growth is expected in the market for premium flanker brands, characterized by higher margins, faster speeds, guaranteed quality of service, or other forms of prestige. Rising user fragmentation can further position flankers as platforms for bespoke propositions, non-connectivity services, and ecosystem partnerships, increasingly activated through social media and digitally native channels.23 Finally, flankers are being increasingly deployed across the telecom spectrum, including mobile, fixed, broadband, satellite, content, and gaming.24

Strategic questions to consider

- What role should flanker brands play for a telecom company in improving subscriber acquisition costs, reducing churn, and stabilizing the portfolio’s overall revenue base?

- Are the company’s flanker brands contributing proportionally to revenue, or are they skewed toward a high share of subscribers but low monetization? And how can the company reengineer its flanker operating models to achieve leaner cost structures comparable to those of digital-first challengers?

The future of B2B in telecom is moving “beyond connectivity”

A trillion-dollar opportunity beckons telecoms, though competing with hyperscalers and managing complex solutions will likely be challenging

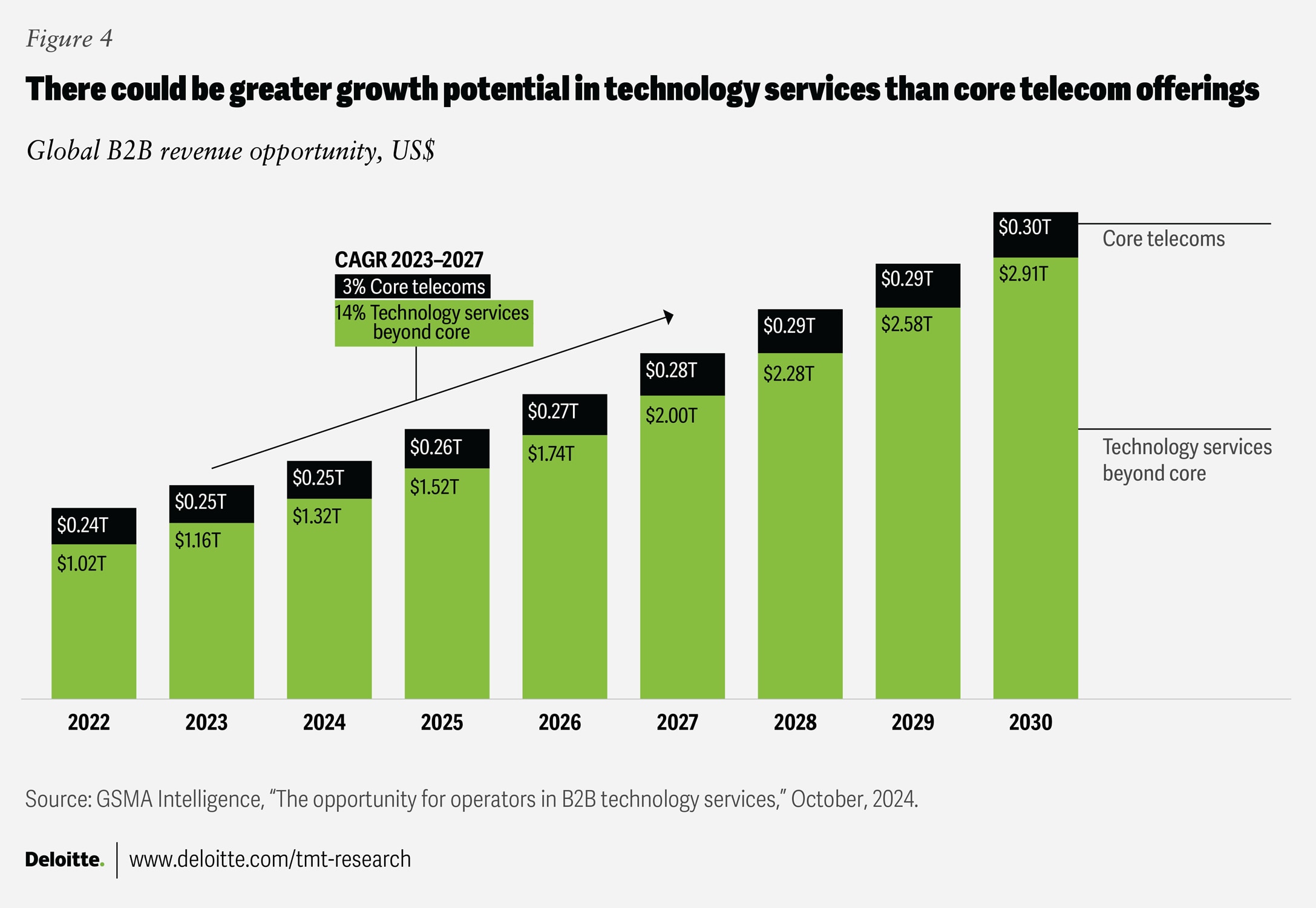

On average, telecom companies generate about 70% of their revenues from consumers and 30% from businesses.25 Of those B2B revenues, about 70% come from providing connectivity services,26 but some speculate that telcos could provide significant “beyond connectivity” services (such as AI, cybersecurity, and cloud platforms) to the B2B market. Success in this market could provide telecoms with a growth lever that would help them grow faster than the low single-digit growth of their core business-to-consumer markets.27 One estimate suggests that the core telecoms B2B market will be about US$270 billion in 2026 with low growth, while the tech services beyond that exceed US$1.7 trillion and are growing at double-digit rates through 2030 (figure 4).28 To be clear, only a portion of that market is potentially addressable by telecoms, and it’s worth about US$620 billion in 2026.29

Given this potential, many telecoms are addressing this market, spurred by competition in their legacy B2B connectivity business from hyperscalers that are capturing a growing share of value in higher-layer services and platforms.30 This is shifting enterprises toward integrated, outcome-based solutions like SD-WAN, SASE, and device-as-a-service models.31

In parallel, telecoms face margin pressure as connectivity becomes more standardized and buyers increasingly expect integrated, outcome-based solutions rather than standalone network products.32 In response, telecoms have expanded their B2B service portfolios beyond connectivity, focusing on areas such as cloud and data centers, cybersecurity, and IoT services.33 However, intense competition in core cloud services often leaves telecoms with lower margins and complex deal structures, resulting in less control.34 Their strongest opportunity in managing complex enterprise environments likely lies in integrating fixed and wireless networks, edge computing, security, and regulated or mission-critical workloads.35

Emerging opportunities, such as network APIs, AI, and data services, are currently small in 2026 but could become material over time. In particular, AI is beginning to reshape enterprise network design and operations, enabling automated provisioning, self-healing networks, and tighter integration across wireless, fiber, and edge environments.36 Major technology vendors are increasingly embedding AI into enterprise networking platforms, creating a growing need for integration partners that can deploy, manage, and operate these solutions at scale. Telecoms, with their network experience and operational capabilities, could play a meaningful role in this ecosystem.37

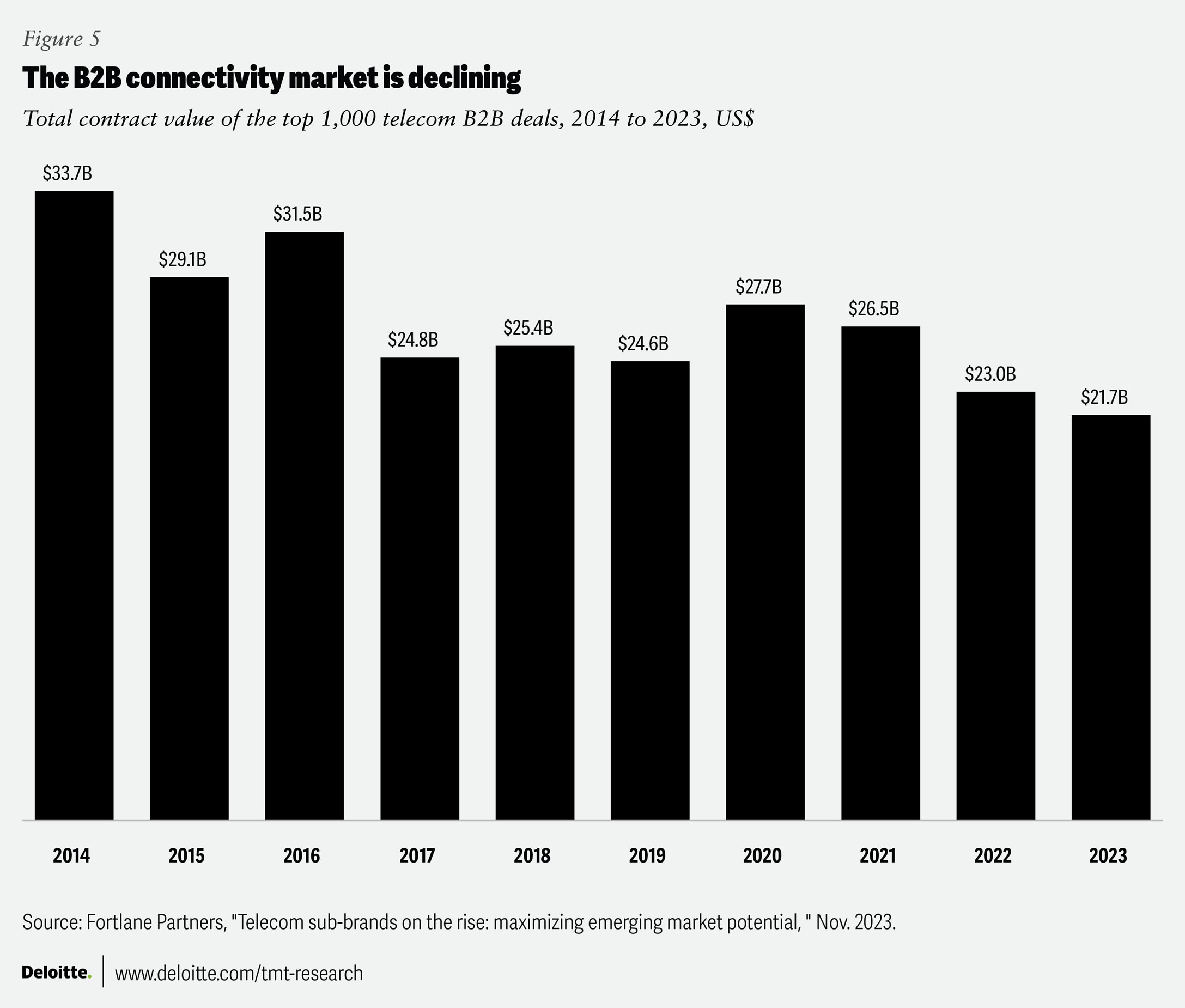

This pivot toward seeking growth through non-connectivity services is referred to by some as “telco to techco.”38 Despite the promise, progress so far has been modest. The value of large B2B deals for telecoms over the last decade has declined (figure 5).39 The challenge is that gains telecoms make in the “techco” space are real… but not enough to offset declines in B2B connectivity.40 Furthermore, margins in these new businesses tend to be low due to competition, telecoms tend not to be the system integrators (and therefore don’t capture all the value), and these deals are complex in ways that telecoms sometimes struggle to manage.41

Strategic questions to consider

- Should telecoms stop pursuing this techco business, or spin it off, to focus on their core connectivity business?

- Could the techco strategy work better by being more focused (for example, cyber only), or by moving downmarket and targeting small and medium-sized B2B market rather than larger enterprise B2B?

- The AI data center market, specifically for sovereign AI, represents a 2026 opportunity. But it has high capital costs, rapid depreciation of advanced chips, and the risk that, if the AI market contracts, telecom AI data centers could become white elephants.

Reconnecting with the customer: Restoring customer satisfaction and loyalty in telecom

Telecom operators enter 2026 amid eroding customer satisfaction and loyalty, needing a shift from utility-driven offerings to valued, relevant, and emotionally resonant experiences

Telecommunications companies are rethinking loyalty, although adoption remains uneven across markets, particularly in the United States.42 In parts of Asia and Europe, however, operators are moving beyond traditional discounts toward ecosystem-based models that integrate digital services, lifestyle benefits, and personalized engagement.43 The priority is sustained, relevant engagement that frames every customer interaction as part of a unified relationship. Through hyper-personalization and seamless connectivity, operators are hoping to restore trust and deepen long-term commitment.

Over the past decade, operators have focused on network expansion and speed as their primary differentiation levers.44 Yet these investments have not translated into better customer sentiment, with telecommunications providers showing limited improvement relative to broader net promoter score benchmarks in 2025.45 By the early 2020s, connectivity had come to be viewed as table stakes, driving commoditization and intensifying price sensitivity.46 Moreover, legacy systems have led to fragmented customer experiences, characterized by long wait times and disjointed support channels.47

In 2026, the industry faces what some refer to as a crisis of customer value and brand loyalty.48 Despite investments in fiber, 5G expansion, and digital service layers, customers perceive little meaningful differentiation among telecoms.49 Consumer sentiment data indicates that up to 77% of consumers feel no loyalty to their provider, and only 47% remain with their primary telecom operator for more than five years, while annual churn rates across telecom providers are around 22%.50

A widening discrepancy exists between network improvements and customer-perceived value. Broader customer-experience research shows that 86% of consumers are willing to pay more for a better experience, and 73% consider experience a key driver of loyalty; yet few telecom brands consistently deliver personalization, proactive service, or coherent digital journeys.51

In industries such as airlines, hospitality, and retail, where core offerings have been commoditized, loyalty programs have become important tools for differentiation, engagement, and ecosystem expansion. Telecoms face a similar challenge: Connectivity alone offers limited differentiation and lower average customer spending, making partnerships and ecosystem-based loyalty models a possible way to extend relevance and perceived value beyond the network.52 Many operators are now transitioning from product-centric models to value ecosystems designed to drive engagement, unlock emotional relevance, and differentiate their brands. These ecosystems integrate rewards, digital entertainment, lifestyle benefits, and targeted offers within unified customer platforms. Early pilots demonstrate measurable outcomes: Loyalty programs can increase customer sentiment by up to 15% and reduce churn by approximately 8%.53

Recovering customer satisfaction is also important. Customers expect proactive service, reliability, and fairness, especially during outages or disruptions. Measures such as automatic bill credits during service interruptions, real-time network transparency, and AI-enabled support can help.54

Telecom operators should increasingly utilize AI agents to automate routine support, freeing human teams to focus on more complex issues. Many operators are likely to implement unified omnichannel platforms to deliver more consistent and transparent customer experiences. However, it will be interesting to see whether personalization builds trust or heightens privacy concerns in regulatory environments.

Strategic questions to consider

- Which approaches—strategic partnerships, enhanced loyalty programs, or exclusive products and offers—will most effectively drive customer stickiness and brand affinity.

- How do companies scale AI agents to automate routine support while elevating human teams to handle complex, high-empathy interactions?

- What new key performance indicators beyond net promoter score should companies build to define success in the next era of loyalty and trust?

Potential signposts for the future

- We were too cautious about the number of telecoms that announced they would build AI factories. It now seems to be the new normal. How many more will be announced in 2026?

- We continue to be cautious about the deployment of AI-enabled radio-access networks, but will keep our eyes open.

- Net fixed wireless access additions in the United States and select European countries remained strong in 2025, but speeds in the US market were down a little toward the end of the year.55 This could be a sign that providers may be reaching capacity limits—something else to watch.

- As of January 2026, there are now requests from various companies to place an additional 1.2 million satellites to be placed in low Earth orbit over time, roughly 100 times more than the approximately 12,000 in orbit at the end of 2025. A key signpost will be the ability to get permissions for those satellites, build them, and especially launch them.56

- We’re predicting that the US communications infrastructure index keeps climbing through 2030 (figure 2). We’ll see if that climb happens in 2026.

Continue the conversation

Meet the industry leaders

Doug Van Dyke

Dan Littmann

Jack Fritz

Jeff Loucks

Duncan Stewart

Jody McDermott

by

Tim Bottke

Jody McDermott

Santosh Anoo

Dan Littmann

Doug Van Dyke

Duncan Stewart

This report was researched and co-authored by Prashant Raman. The center would like to thank Tim Bottke, Jody McDermott, Santosh Anoo, Dan Littmann, Dieter Trimmel, and Jack Fritz for their valuable insights and perspectives in developing this outlook. The authors would also like to thank Kristen Tatro and Prem Kumar for marketing and PR support and Pankaj Bansal for providing the data used in this report.

Editorial (including production and copyediting): Andy Bayiates, Prodyut Borah, Sayanika Bordoloi, and Anu Augustine

Design: Molly Piersol

Cover artist: Rahul Bodiga; Adobe Stock

Knowledge Services: Vanapalli Viswa Teja

Visit the Deloitte Center for Technology, Media & Telecommunications

Access more insights for the technology, media, and entertainment; semiconductor; telecommunication; and sports sectors.