{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Trend 1: Building resilience amid volatility has been saved

Cover image by: Stephanie Dalton Cowan

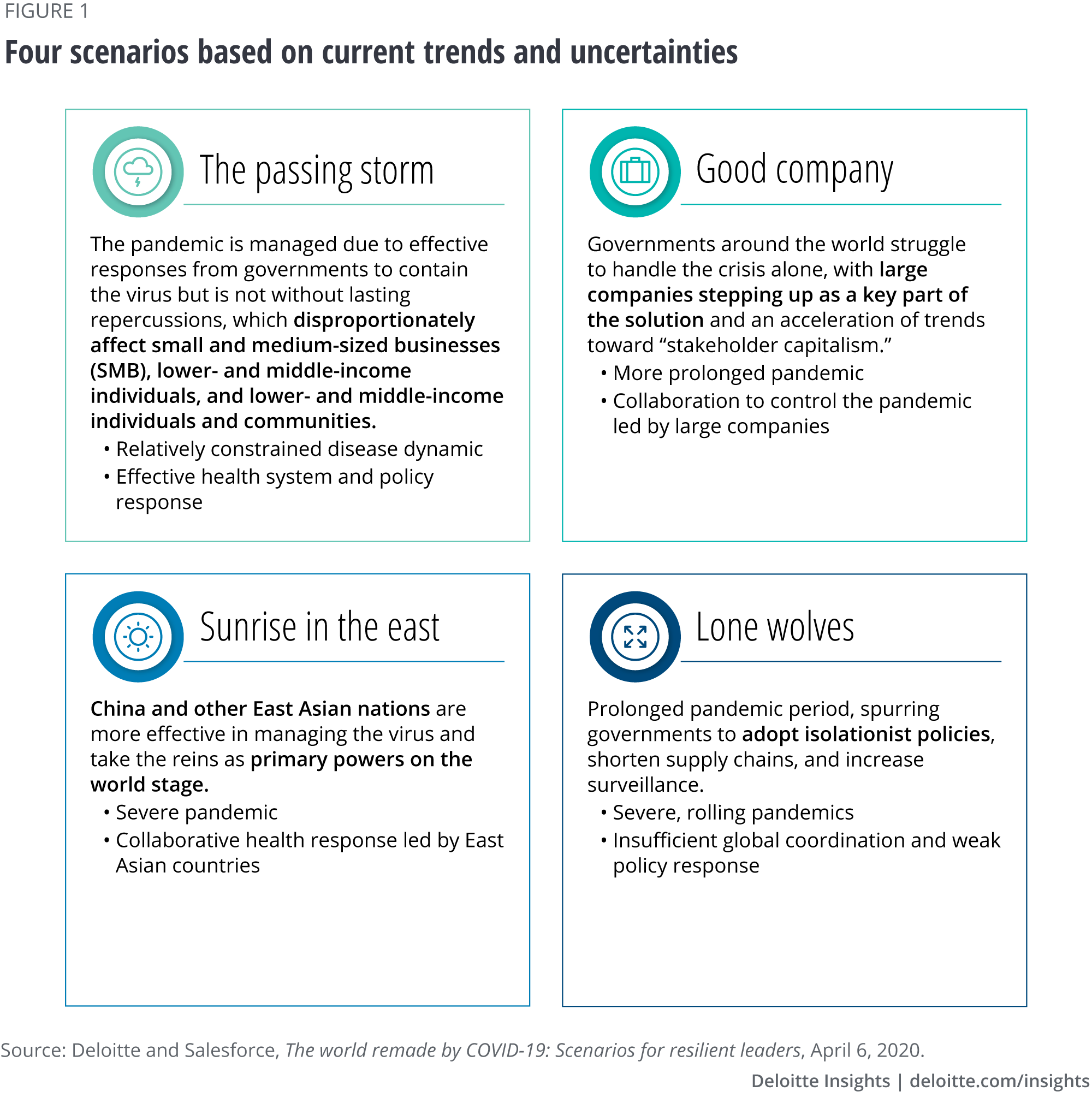

While COVID-19 has had a range of impacts on mining companies, varying by commodity and geography, the one thing the past year has taught leaders is the value of building resilient organizations to navigate uncertain futures. To build a resilient organization, mining companies should embrace scenario planning as part of their strategic planning processes. Doing this effectively can position miners to better anticipate a range of global disruptors that could affect their organizations. To help companies on this path, we outline four divergent scenarios based on current trends and uncertainties and consider how they might play out in the mining sector.

Setting strategy and mitigating risk have always required an element of prediction. The further into the future a company needs to peer, the harder it is to develop accurate forecasts. Mining companies that work on decades-long time horizons are all too familiar with this challenge.

When a wrench is thrown into this process, companies often scramble to recalibrate. This has certainly been the case with COVID-19. As the pandemic began taking a toll on the global economy, mining companies found themselves reacting to emergency measures, regional regulations, and supply chain disruptions.

To protect worker health and safety, many companies quickly canceled nonessential travel and moved to remote work, where possible. In addition to imposing stricter hygiene and social distancing measures, some also scaled down production on specific sites in response to cases of COVID-19 and/or supply chain disruptions.

To mitigate risk, numerous companies created specialized internal task forces to develop site-specific pandemic plans, began screening onsite workers for symptoms, and took steps to solidify their finances through cash-flow planning. Several miners in remote regions also found themselves stepping up donations to help local health authorities meet their urgent needs for personal protective equipment (PPE).

“Now that the initial shock has passed, companies are facing challenging environments, alternating between restriction and relaxation,” says Andrew Swart, Global sector leader, Mining & Metals, Deloitte Touche Tohmatsu Limited. “The differential impact of COVID-19 on different commodities and geographies has heightened both volatility and uncertainty. Despite being in uncharted waters, leaders should take decisive action to ensure their organizations are resilient.”

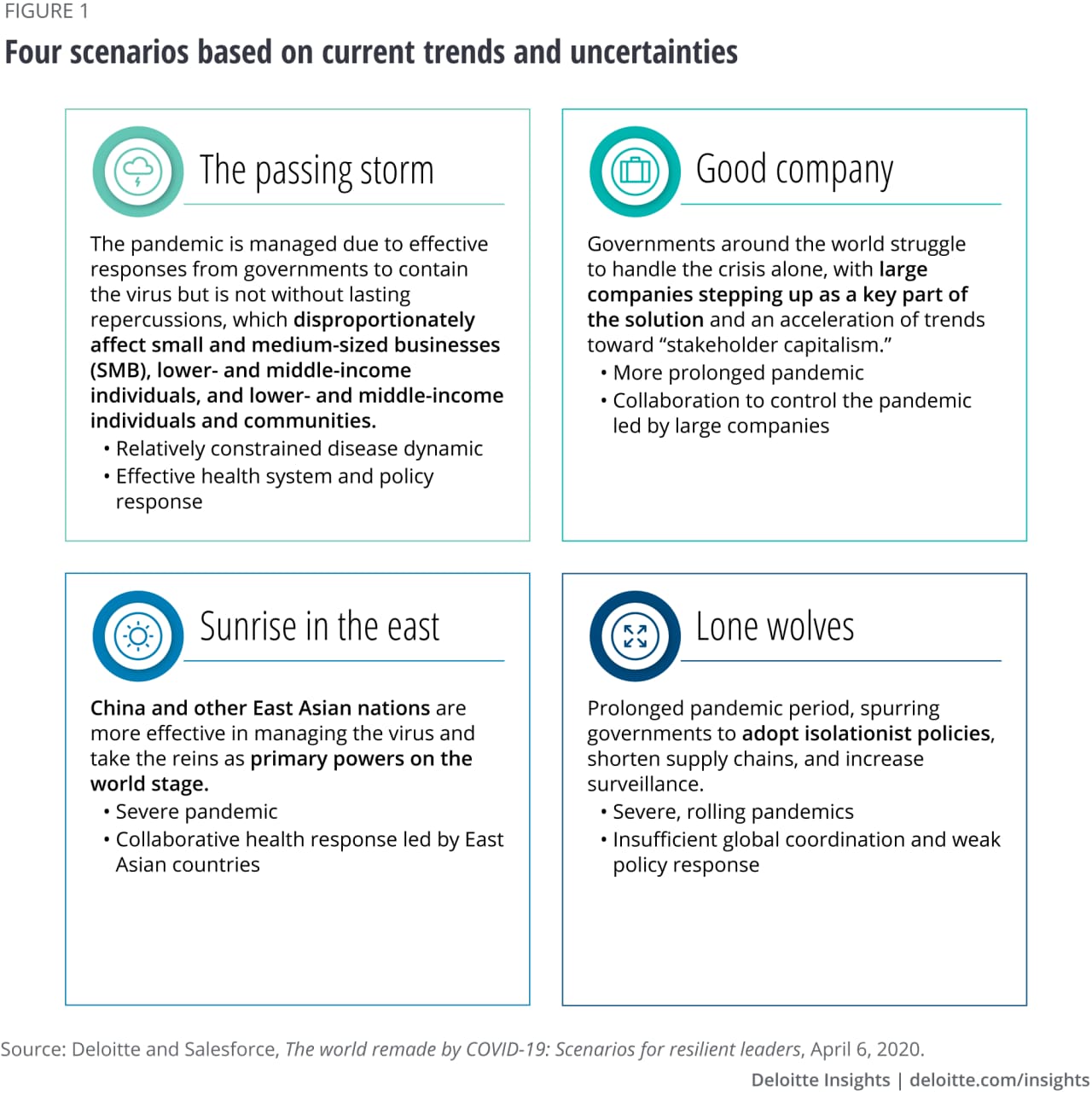

To help mining companies set their strategy and mitigate risk in the coming three to five years, Deloitte considered how the future might be affected by two uncertainties: (1) the severity of the pandemic, and (2) the level of collaboration within and between countries.

A set of scenarios developed by Deloitte and Salesforce1 was used as the basis for the development of four distinct scenarios related to the mining sector (figure 1).

While scenarios are merely stories of what the future may be like rather than predictions of what will happen, these hypotheses can help leaders open their eyes to new opportunities and hidden risks:

In assessing how these scenarios may play out, trust figures prominently. In many ways, an effective recovery hinges not only on citizens’ ability to trust in government, communities’ ability to trust in companies, and employees’ ability to trust in their employers’ leadership, but also on the trust of investors to deploy capital.

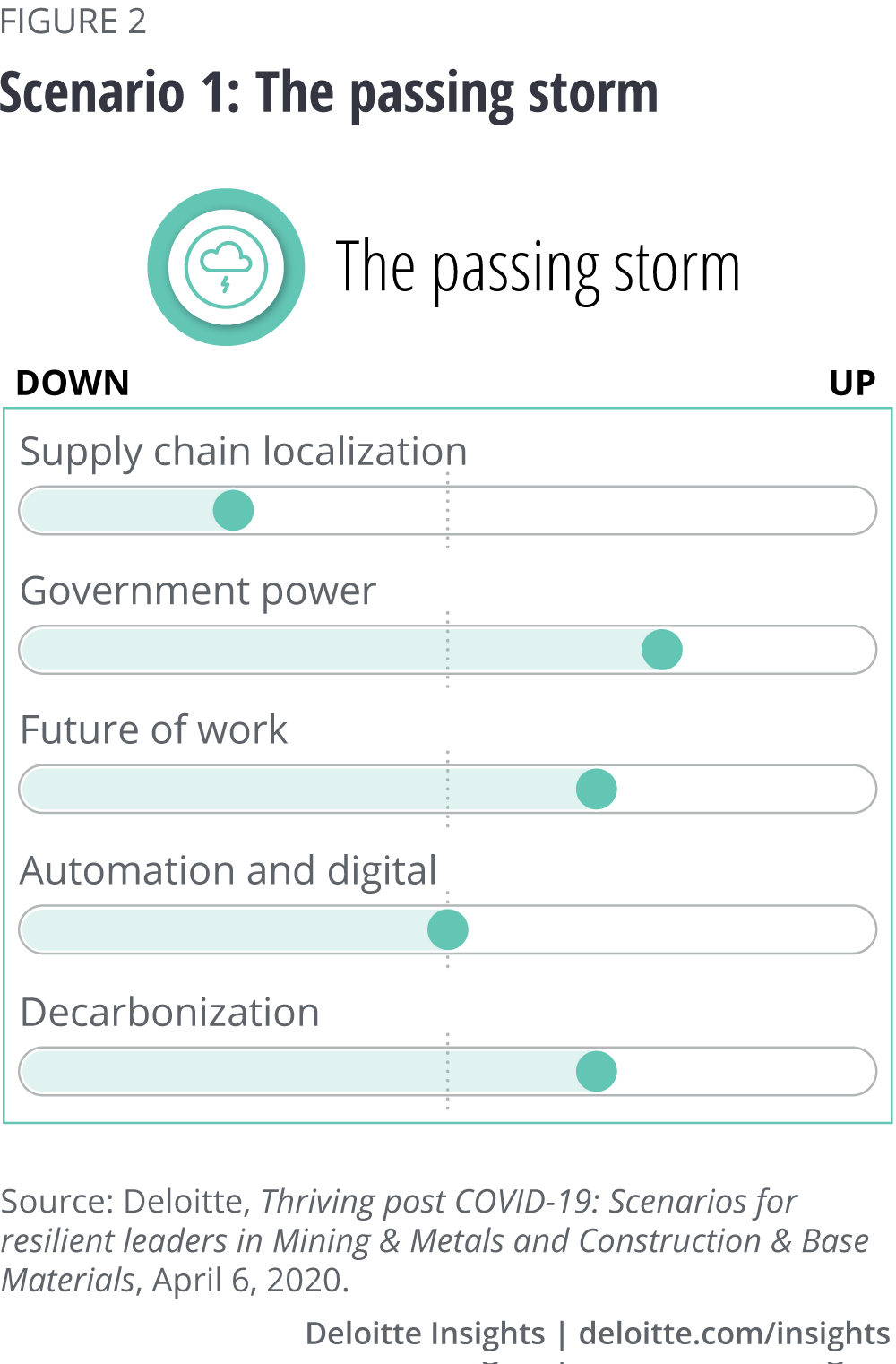

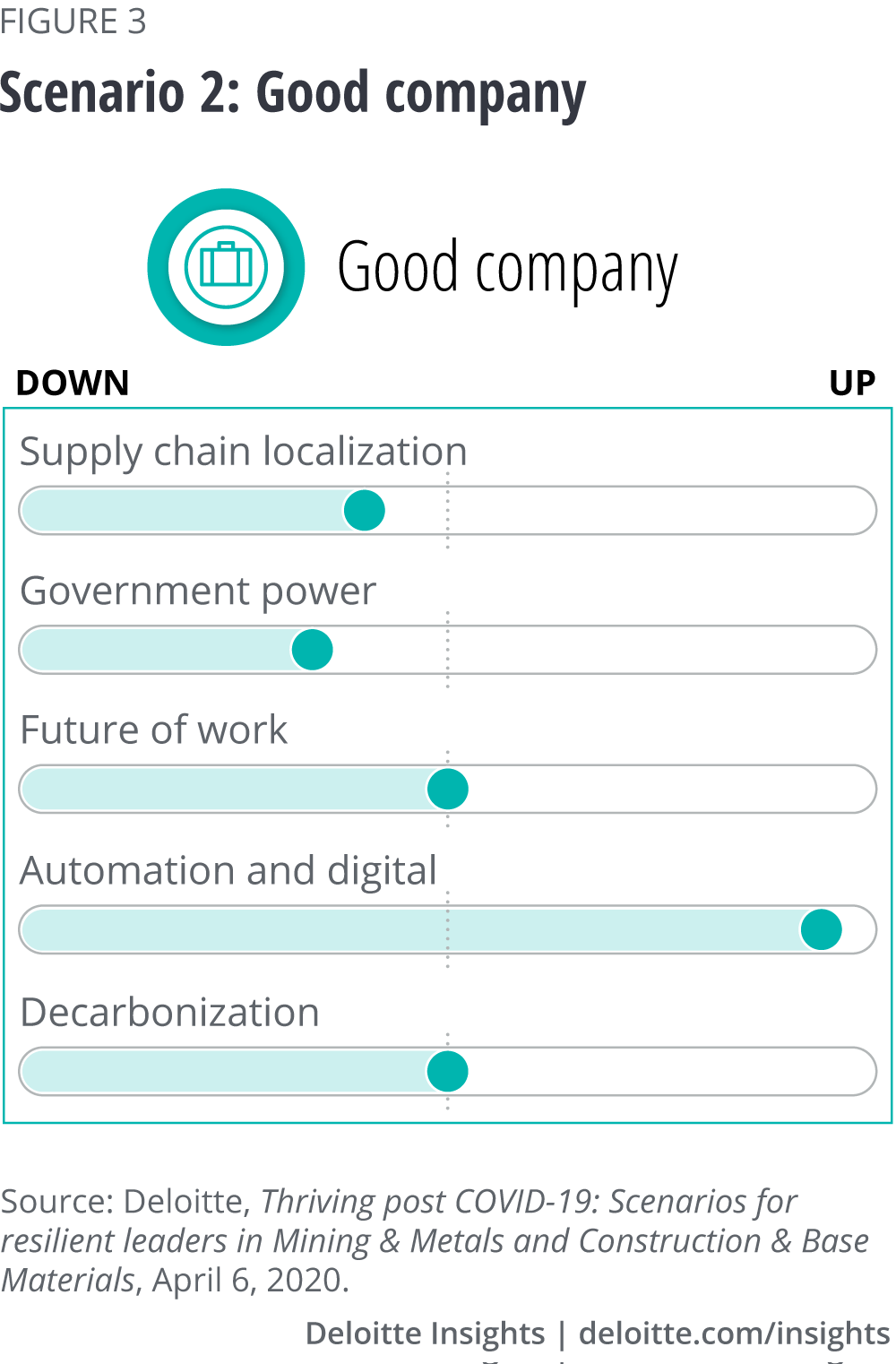

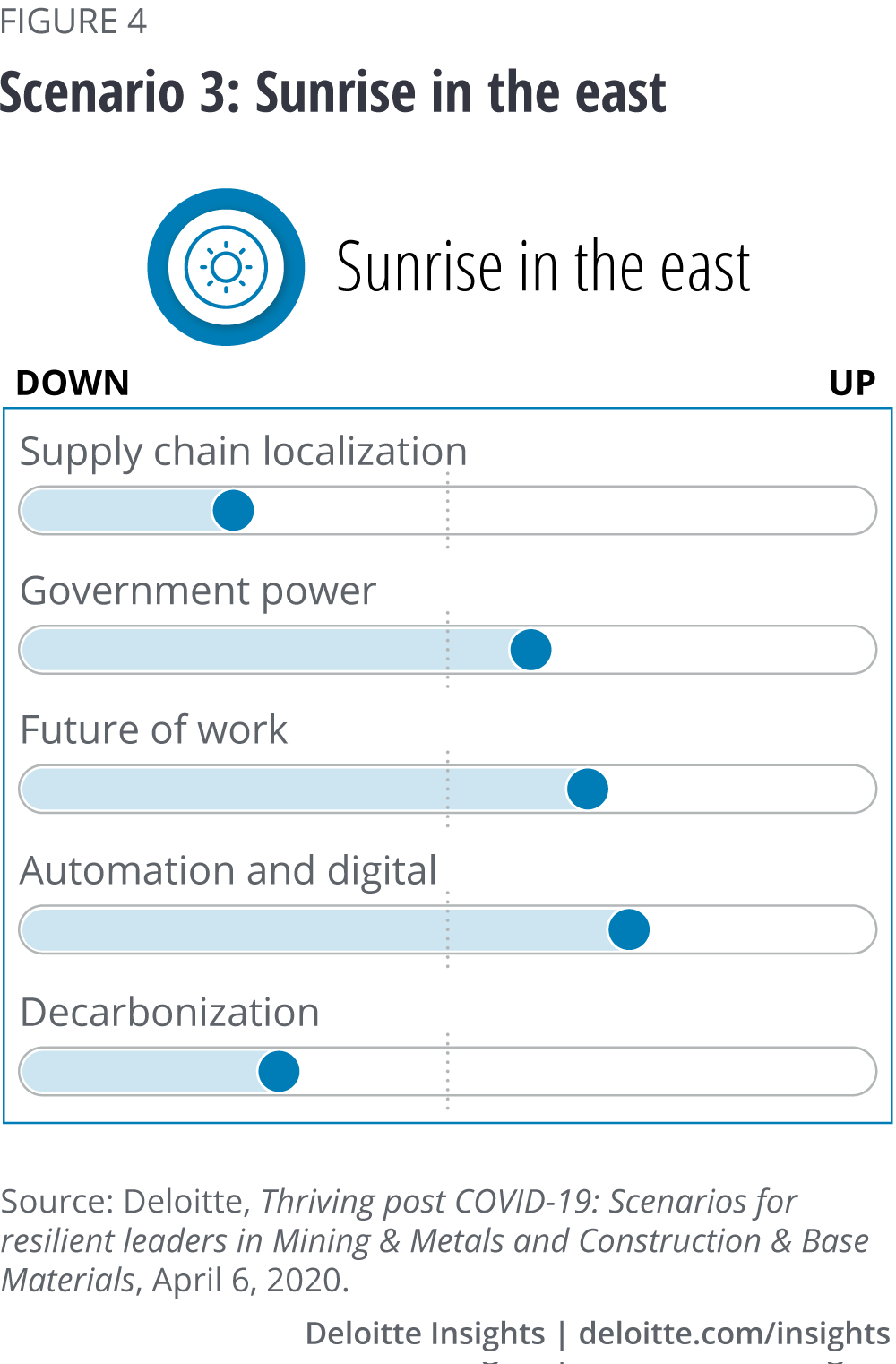

To determine how these scenarios might play out in the mining sector, we considered their impact on five industry megatrends, which have been illuminated because of the COVID-19 pandemic. Depending on which scenario plays out over the next three to five years, some of these trends can be accelerated, while others may slow down:

By lining these megatrends up to our four scenarios, we get a sense of how the global landscape might unfold in the next three to five years (figure 2).

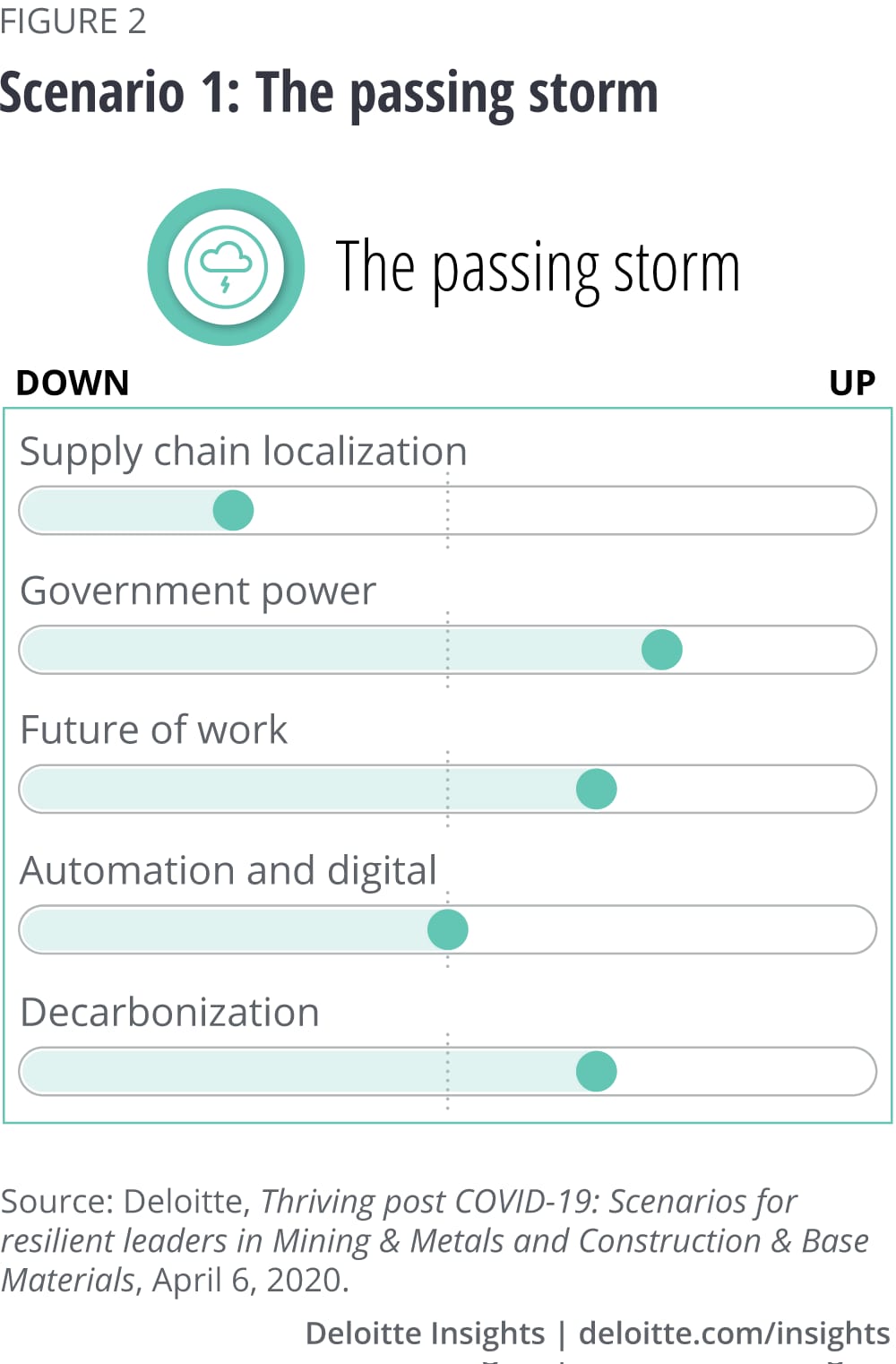

In response to the crisis, mining companies would likely keep automating and digitizing their operations and assets to mitigate risks. Governmental stimulus, including an accelerated infrastructure agenda, could help drive the demand for and prices of commodities. Less affected by the economic impacts, large companies would likely be better positioned to move forward by investing in new exploration and operations, technology innovations, and acquisitions of smaller players. Efforts to decarbonize the supply chain could also allow companies to respond to mounting ESG pressures and maintain social licenses.

Signposts that may indicate progression toward this scenario include:

Should this scenario come to pass, larger mining companies would likely have better access to resources and investment to combat COVID-19 in the short term and would rebound quicker. For their part, smaller mining companies may take longer to return to normal, given their lack of resources and reduced ability to change operations in the short term.

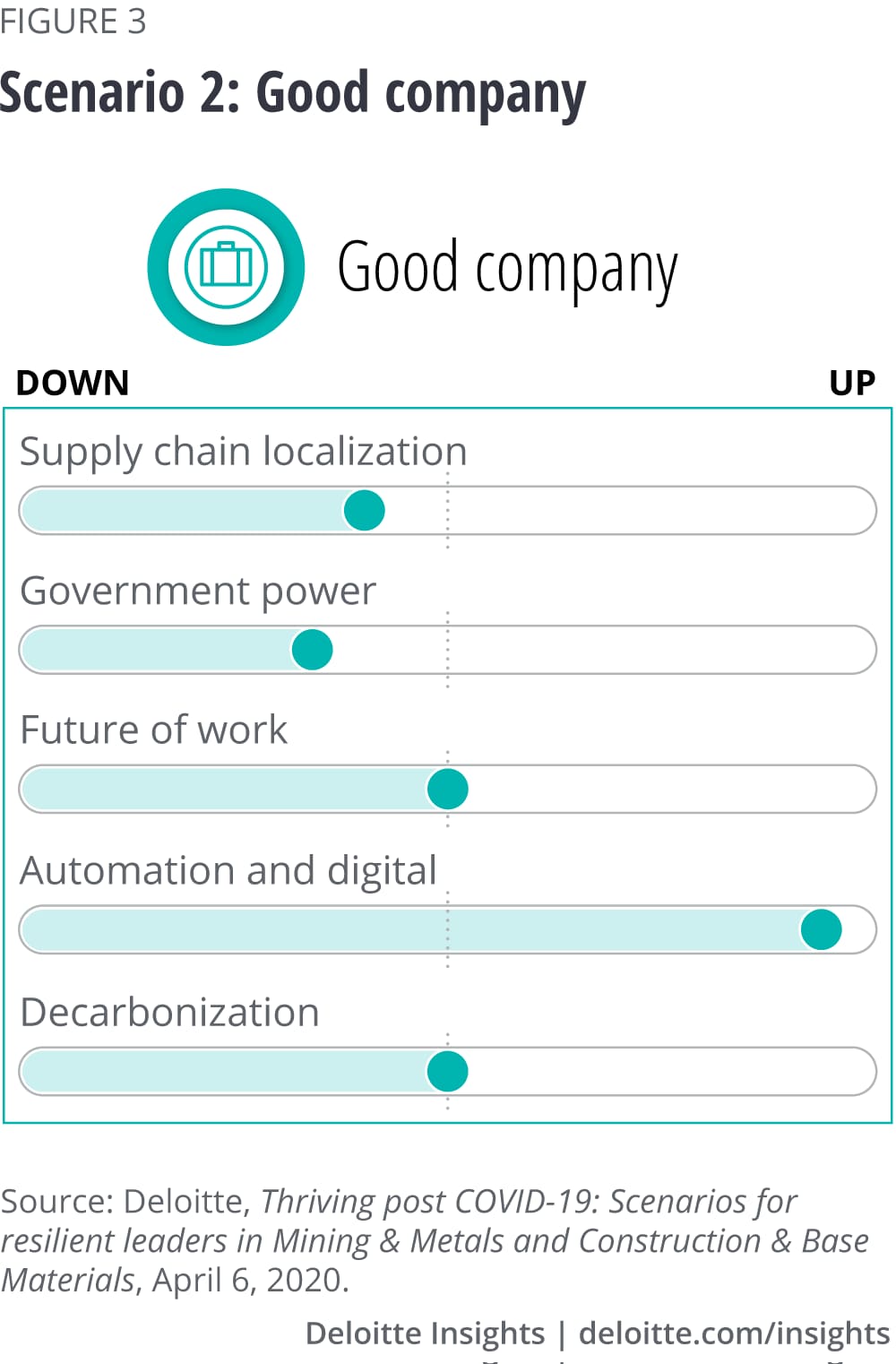

Mining companies could be forced to step up to the plate (figure 3). Companies can volunteer their resources to support and supplement containment, treatment, and recovery efforts. They would also be increasingly expected or required to make direct financial investments into their local communities to maintain their social license to operate and avoid a backlash from communities, governments, and the media. At the same time, mining companies would need to adapt to new realities by investing more heavily in areas such as wearables, virtual reality, AI, and 3D printing to combat significant supply chain shifts and workforce social distancing requirements.

Signposts that may indicate progression toward this scenario include:

Should this scenario come to pass, miners with good community and government relations could build on their license to operate. Conversely, those with poor reputations might not be seen as strategic partners and could be left behind.

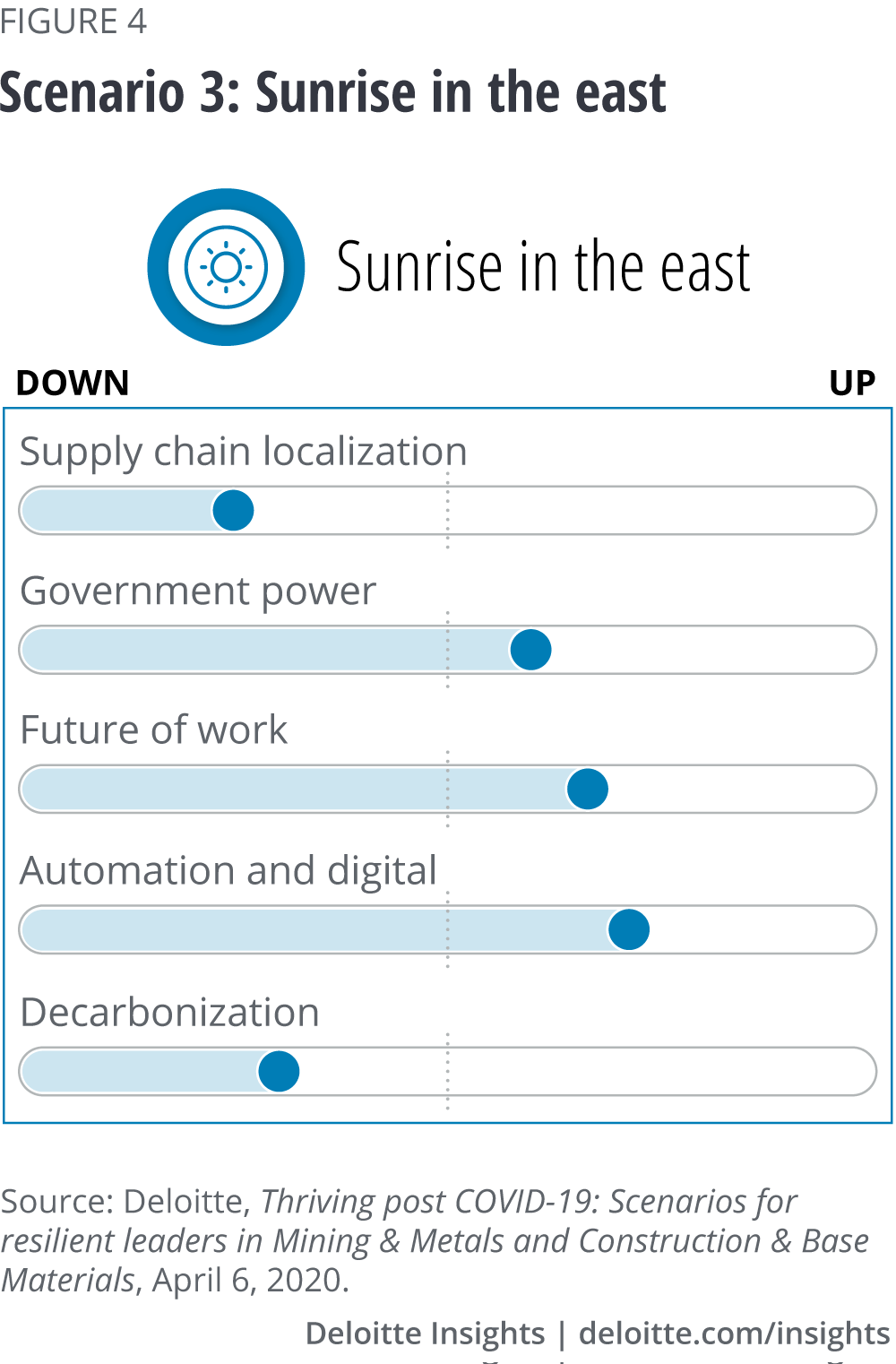

The severe and long-lasting impacts of the crisis would see mining companies prioritize and accelerate the implementation of digital technologies (see figure 4). Particularly in remote areas and developing countries, companies could develop programs in and around their operations to provide public services that highly indebted governments cannot afford. East Asian countries could take a central role in acquisitions and consolidating some sectors. Some governments may turn to nationalization to help their finances. Mining companies could shift away from decarbonization efforts and toward business models lighter in assets.

Signposts that may indicate progression toward this scenario include:

Should this scenario come to pass, mining companies based in East Asian countries will likely rebound quickly, and those with demand based in Asia could see stronger results than others. All other jurisdictions could be at a productivity disadvantage given local restrictions and social distancing measures, and would see softer demand as a result.

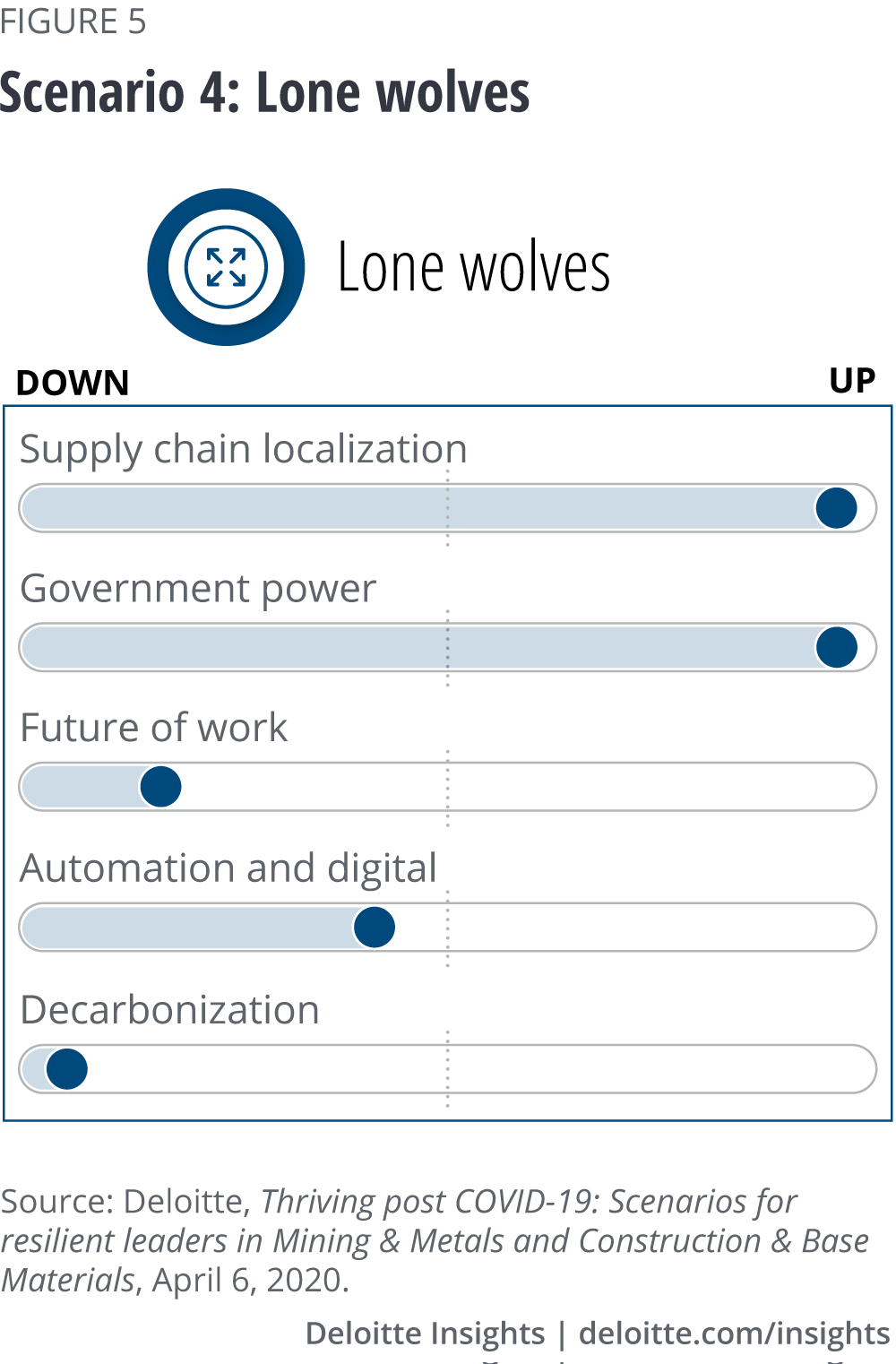

In response to the impacts of the crisis, mining companies could see drastic disruptions to their production and supply chains. With strict social distancing and tracking measures, companies could be forced to halt production or to suffer large productivity declines. If countries adopt isolationist policies and global supply chains are cut, companies would likely seek local suppliers and customers (figure 5). The strength of local supply chains could determine who will survive. In regions with strong local demand, companies could thrive; in regions where metals are heavily exported, companies could struggle.

Signposts that may indicate progression toward this scenario include:

Should this scenario come to pass, mining companies with their own integrated processing operations could be better positioned to weather the storm. Those with largely global supply chains could have to navigate a complicated international landscape in order to continue operating.

In order for companies to navigate the next few years, they will likely require dynamic strategies, resilient leadership, and a constant reevaluation of the environment around them. Scenario planning could be an invaluable tool for leaders as they embark on the next few years.

The four scenarios set out here suggest a range of possible impacts as the COVID-19 crisis evolves. To build resilience, leaders should take several key steps:

Knotch card

Cover image by: Stephanie Dalton Cowan