Building circularity into the claims process can move the insurance industry closer toward resiliency

Deloitte’s survey of insurance executives reveals opportunities for the property and casualty industry to embed sustainable practices in claims management.

Customer experiences during the claims process are often considered a key ‘moment of truth’ for policyholders, helping to shape long-term loyalty to an insurer.1 And claims are, by far, a property and casualty (P&C) insurer’s biggest cost component;2 paid losses combined with investigative and settlement expenses accounted for about 76% of US premiums collected for 2022.3 However, finding an optimal balance between customer satisfaction and profitability is becoming ever more challenging to achieve in an environment of soaring expenses and climate related losses. The combined ratio4 for the US P&C insurance industry climbed from 98.8% in 2000 to 102.4% in 2022 and 102.6% in the first quarter of 2023.5

The impact of inflation, the rising frequency and severity of catastrophic events, and increasing litigation costs amid growing stakeholder and regulatory expectations are putting increased pressure on carriers. While adopting advanced technology and minimizing organizational silos can help, another differentiating strategy for insurers could be the integration of sustainability into the claims process. Insurers are in a unique position as society’s risk managers to lead sustainability efforts from the front by encouraging purpose-driven decisions and strategies within the web of relationships over which the industry has an influence.6

Insurers can encourage value chain partners, such as vendors, customers, and employees, to minimize the use of the world’s resources, cut waste, and reduce carbon emissions. But this is not just a “check the box” activity of opting for greener solutions or eco-friendly products. Instead, the approach should embed environmental resiliency and circularity throughout the claims management process, from first notice of claim and triage through resolution and future prevention.

According to research by the Deloitte Center for Financial Services, however, industry progress in this direction is just beginning: A November 2022 survey of sustainability executives on climate risk governance7 revealed that although most insurers have committed significant time and resources to integrating decarbonization strategies in underwriting and investing, progress is farther behind in claims management. To further investigate these sustainability gaps, the Deloitte Center for Financial Services surveyed 51 claims executives at US-based P&C insurance companies in July 2023. The results revealed what insurers are doing to implement sustainable practices in claims management, as well as challenges they face in embedding sustainability throughout the process.

Who we surveyed

Deloitte’s Center for Financial Services surveyed 51 claims executives from P&C insurance companies in July 2023 spanning a mix of personal lines (63%), commercial lines (31%), and reinsurers (6%). Companies were mostly privately held (63%); 37% were publicly listed. The annual revenues broke down as follows:

- US$500 million to US$1 billion: 27%,

- US$1 billion to US$5 billion: 43%,

- US$5 billion to US$10 billion: 20%, and

- US$10 billion or more: 10%.

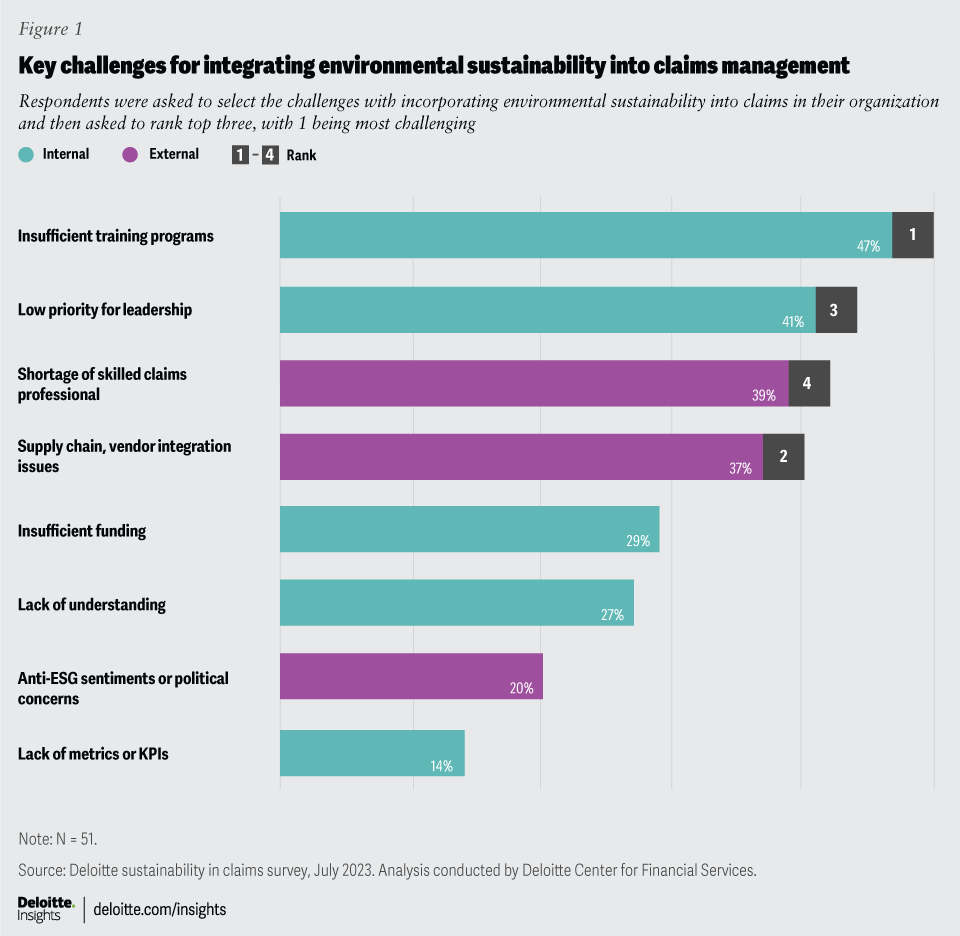

The survey showed that while 80% of claims executives think that embedding sustainability in claims management is important, only 29% of those surveyed are in advanced stages of implementing their strategies, due to challenges such as insufficiently trained staff, low levels of leadership support, and the immaturity of sustainability programs among value chain partners (figure 1).

{kind=link}

Whereas training needs and leadership sponsorship may be addressed through internal awareness programs, supply chain issues and a shortage of claims personnel will likely require more alignment with vendors and a skills-based recruitment approach.8

To assess the progress of their sustainability integration efforts, the survey asked executives to describe the action steps they have already taken across each of five core aspects of the claims management process. The research identified several key gaps the industry should bridge to help advance circularity both within their own operations and beyond.

Digitizing claims management

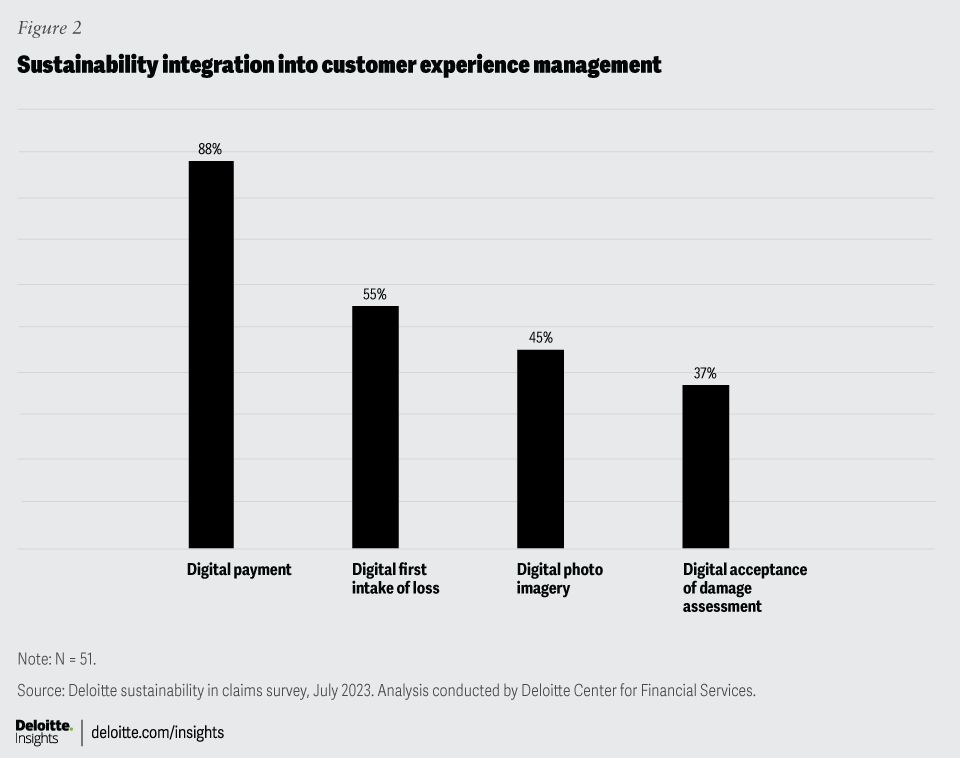

According to the survey, most respondents are enabling digital capabilities to make payments (88%) and register claims (55%), while fewer than half (45%) are using virtual imagery such as satellite or drone images at loss sites (figure 2). For faster and more efficient resolution, adjusters should be supported in leveraging technology to reduce the overall time needed to analyze complex claims and upload approvals. Supplementing this imagery with the use of virtual intelligence (artificial intelligence) can further help to categorize the extent and cause of damage remotely and assign appropriate solutions. For example, using drones for virtual site inspections can help ensure safe and efficient assessment of property claims. Not only can the use of technology increase processing speed by eliminating physical travel for claims adjusters but it can also help lower the insurer’s carbon footprint.

{kind=link}

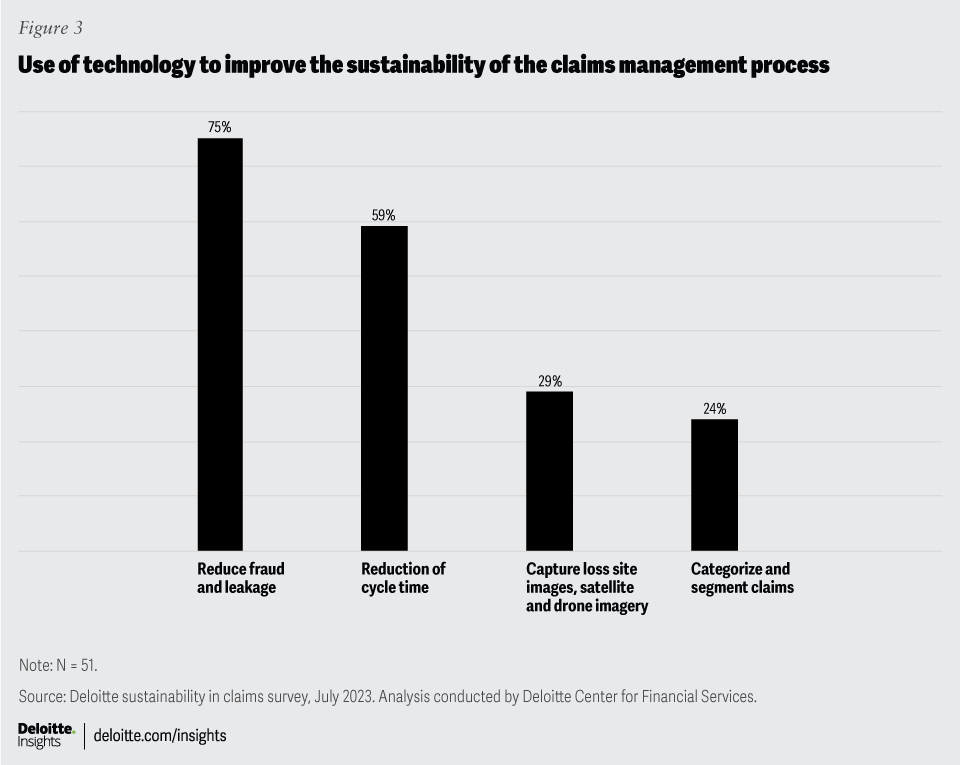

In addition to using technology to settle claims more efficiently, most respondents are also using it to weed out suspected fraud, thereby minimizing time and travel by fraud investigators (figure 3). Carriers can also make claims handling more efficient by digitally segmenting and categorizing claims according to criticality and complexity. This can help settle basic cases automatically and assign the more complex incidents to handlers.

{kind=link}

Recent advancements in technology, including generative AI, also offer opportunities to make claims management more sustainable. Hartford Steam Boiler Inspection and Insurance Co., for example, employs AI and advanced analytics, such as internet-of-things (IOT)-enabled hardware sensors and monitoring devices, to try to predict when and where potential disasters will happen so they can nudge policyholders to take preventive actions.9

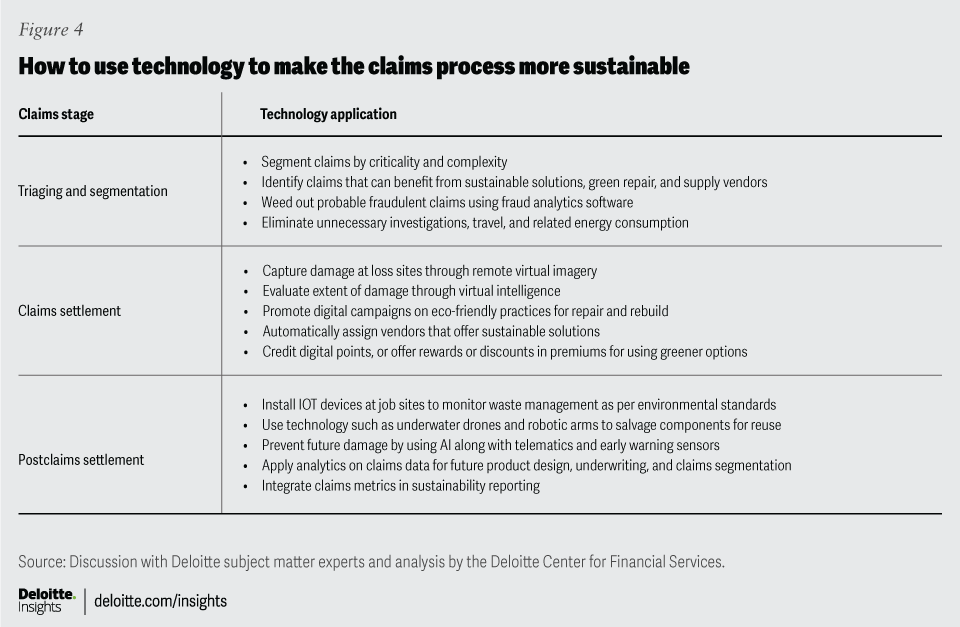

Providing a seamless digitized end-to-end claims experience, from triage and claims segmentation during the first intake of loss, to final settlement, can potentially improve profitability and enhance employee and customer experience and boost net-zero efforts. The following recommendations are a summary of leading practices that should be considered for advancing sustainability through technology solutions (figure 4).

{kind=link}

Aligning value chain partners

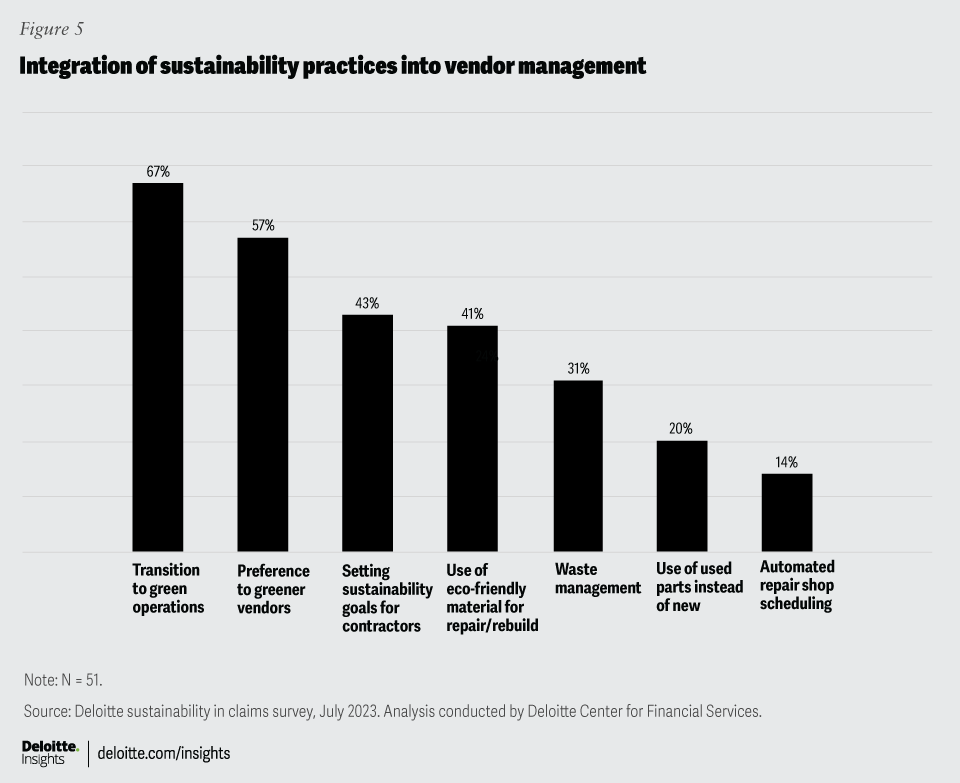

Seamlessly adopting emerging technologies such as these, however, will likely require insurers to closely collaborate with channel partners, such as contractors and vendors. While most survey respondents are already guiding vendors to transition to greener operations (67%) and seeking out more sustainable vendors and suppliers (57%), the results suggest more can be done to encourage vendors to choose repair (over replace), promote the use of eco-friendly and recycled materials in rebuilding, and to help ensure adequate waste management practices, especially for the disposal of hazardous by-products and salvaging undamaged parts for reuse (figure 5).

{kind=link}

Given the time and expense involved with inspecting, repairing, or replacing damaged assets, P&C insurers should consider how to “build back better” when a loss occurs to preempt risks and help prevent the occurrence of damage going forward. It might also mean encouraging the use of sustainable, resilient materials, for example, smart glass, engineered timber, green cement, and applications, such as early warning flood systems, that may mitigate and prevent future damage and consequent claims.10

Encouraging channel partners to adopt eco-friendly waste disposal practices can also help reduce the load on landfills. For example, the Allianz Group works with recycling companies to source green parts from damaged vehicles that can be used for subsequent vehicle repairs.11 And as vendors and suppliers embed circularity in their own repair, recycle, and redesign processes, it can increase the product shelf life and reusability and help reduce insurers’ Scope 3 emissions.

Vendors that incorporate sustainable solutions such as these into their operating models can be recommended to customers as a preferred channel partner by the insurer and automatically be assigned when a claim arises. Aviva, for example, provides motor vehicle insurance customers with access to local garages that deliver sustainable products and services.12

Elevating the strategic focus on sustainability

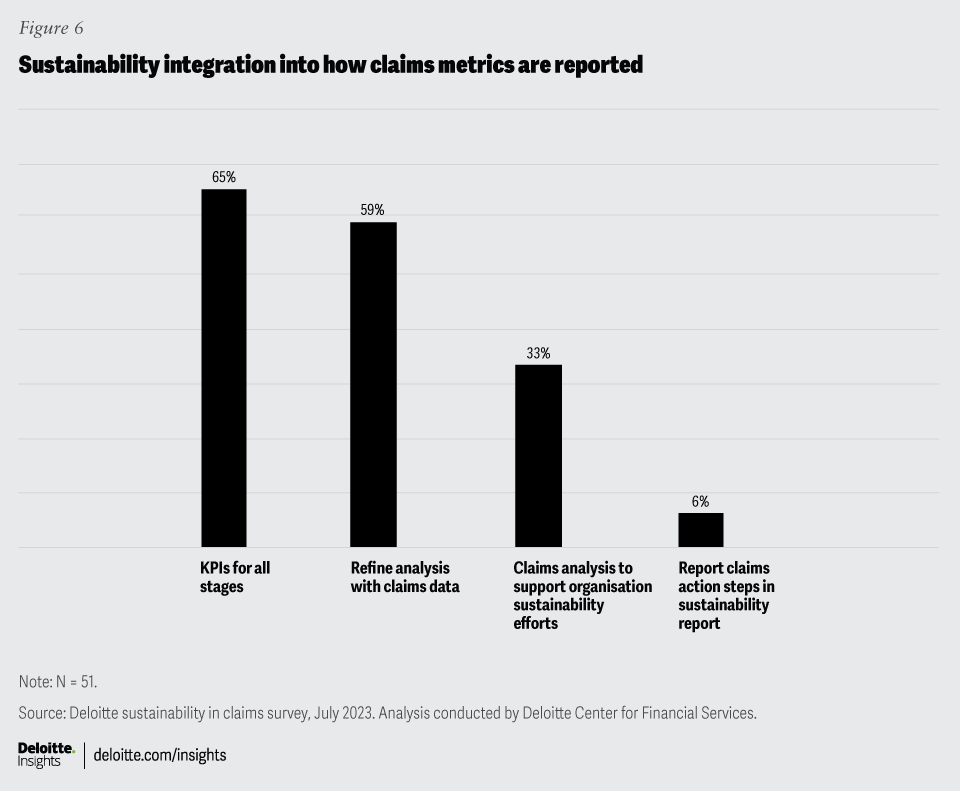

When it comes to sustainability reporting practices, 65% of survey respondents have established key performance indicators for all stages of the claims process, but only 33% are leveraging claims data analysis to drive overall sustainability targets. This can be a missed opportunity insofar as sustainable claims practices are good for the bottom line: They not only help improve overall profitability by preventing future claims, but they can also generate insights for business decisions around product design and underwriting. In response to rising claims from certain flood-prone areas in Florida, for example, Swiss Reinsurance Co. Ltd, in partnership with Security First Insurance, enabled residents to include water damage, such as flood coverage which was previously uninsurable under their homeowners’ policy.13

{kind=link}

Until leadership prioritizes these imperatives, sustainability efforts for claims management may not add sufficient value to either clients or insurers. When respondents were asked how often they interact with sustainability leaders,14 only 10% met monthly, 25% quarterly, 45% annually, and 20% had no regular discussion. Claims executives can increase focus on claims management by engaging more frequently with their sustainability leaders to brainstorm ideas and industry leading practices, frame pathways to embed sustainability in the claims management process, and establish metrics to inform decision-making.

Building a skilled workforce

Elevating the strategic importance of claims in an organization’s net-zero roadmap also often means earmarking adequate funds for new talent acquisition and upskilling the existing workforce to strengthen the company’s technological capabilities.

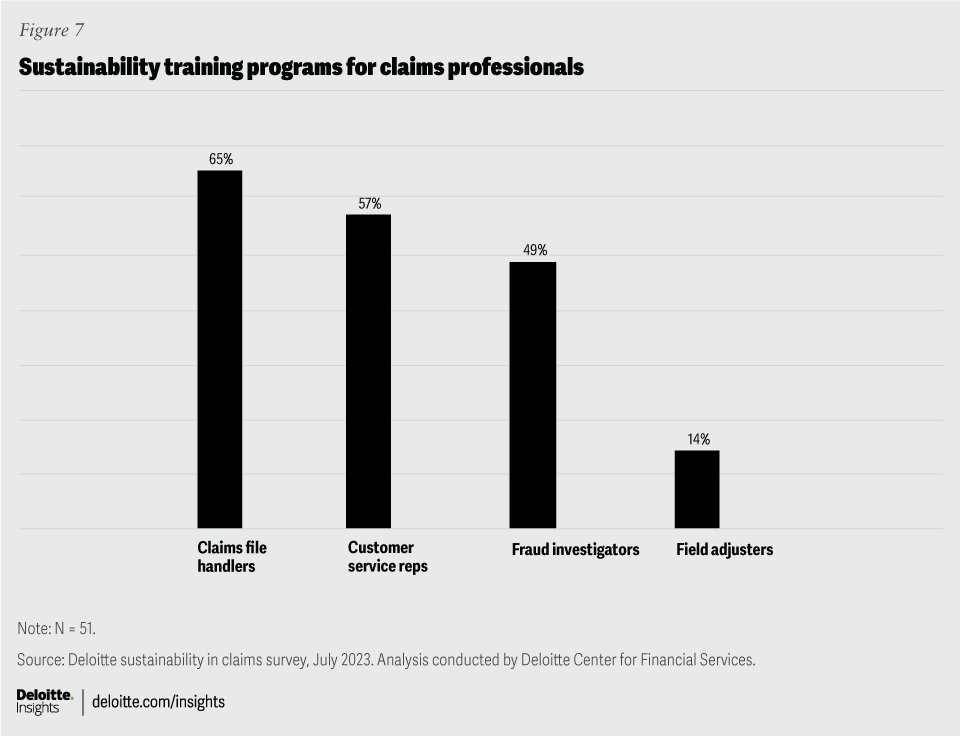

Incorporating digitalization and other strategies related to sustainability in claims management will likely be unsuccessful or underwhelming without sufficient training on the usage of new technology, processes, and services for all involved. Yet according to our survey results, 86% of respondents said their companies had no training programs for field adjusters, indicating advanced technologies like satellite imagery and virtual intelligence in claims assessment may be underutilized for remote capture, assessment, and assignment of sustainable solutions.

The survey data also shows that while 75% of respondents say they are using technology to help reduce fraud (figure 3), only 49% are offering related training (figure 7). Carriers may need to invest in training modules and simulation workshops for fraud investigators if they are to apply advanced analytics to weed out suspected fraud or minimize unnecessary travel for investigations.

{kind=link}

Embedding sustainability throughout the claims process warrants calibrated action steps and a more efficient alignment with all stakeholders. This may require insurers to move beyond the role of a coverage provider to that of an asset protector that advances sustainable practices through business relationships, helps preempt and prevent future losses, and builds resiliency into the business. It involves creating awareness of sustainable solutions, incentivizing customers to select these options, and collaborating with vendors and suppliers to deliver such solutions. Embracing these strategies can also mean improving business viability and helping insurers find a more optimal balance between customer satisfaction and profitability while elevating their brand.

By

Michael Cline

Kedar Kamalapurkar

Namrata Sharma

The authors would like to thank Elizabeth Payes; Dilip Kotlapati Sekhar and Harris Ahmad from Deloitte Consulting LLP for their contribution to this article; as well as Rajesh Medisetti from the Data Science and Survey Advisory team.

Cover image by: Sylvia Chang

Visit the Deloitte Center for Financial Services

Access more insights for the banking and capital markets, commercial real estate, insurance, and investment management sectors.