Gen Z and millennials are more alike than banks may assume

Converging behaviors across digital adoption, financial apps, and data sharing reveal a unified customer segment with evolving expectations

Many banks have tried to decode the attitudes and behaviors of Gen Z customers, often seeing them as digitally native, yet skeptical of traditional institutions.1 Millennials, by contrast, tend to be perceived by banks as financially cautious and more predictable in their banking habits. If these characterizations are accurate, banks might need separate strategies for each group.2

However, a Deloitte survey of financial habits of 2,027 US banking customers challenges this view. It reveals that Gen Z and millennials seem to be converging into a single, digitally native segment with similar financial behaviors. Some of the differences may reflect life stage and financial needs rather than something unique to each generation, yet their expectations of digital banking appear largely the same.

This insight matters because banks continue to invest heavily in generational segmentation.3 A clearer understanding of these consumers, grounded in data, can help shape strategies to better meet their needs.

The survey, conducted in 2025, included respondents from different generations, sexes, and income levels. Generations were defined using the following ranges as birth years: silent generation (1928 to 1945); baby boomers (1946 to 1964); Generation X (1965 to 1980); millennials (1981 to 1996); and Generation Z (1997 to 2003).

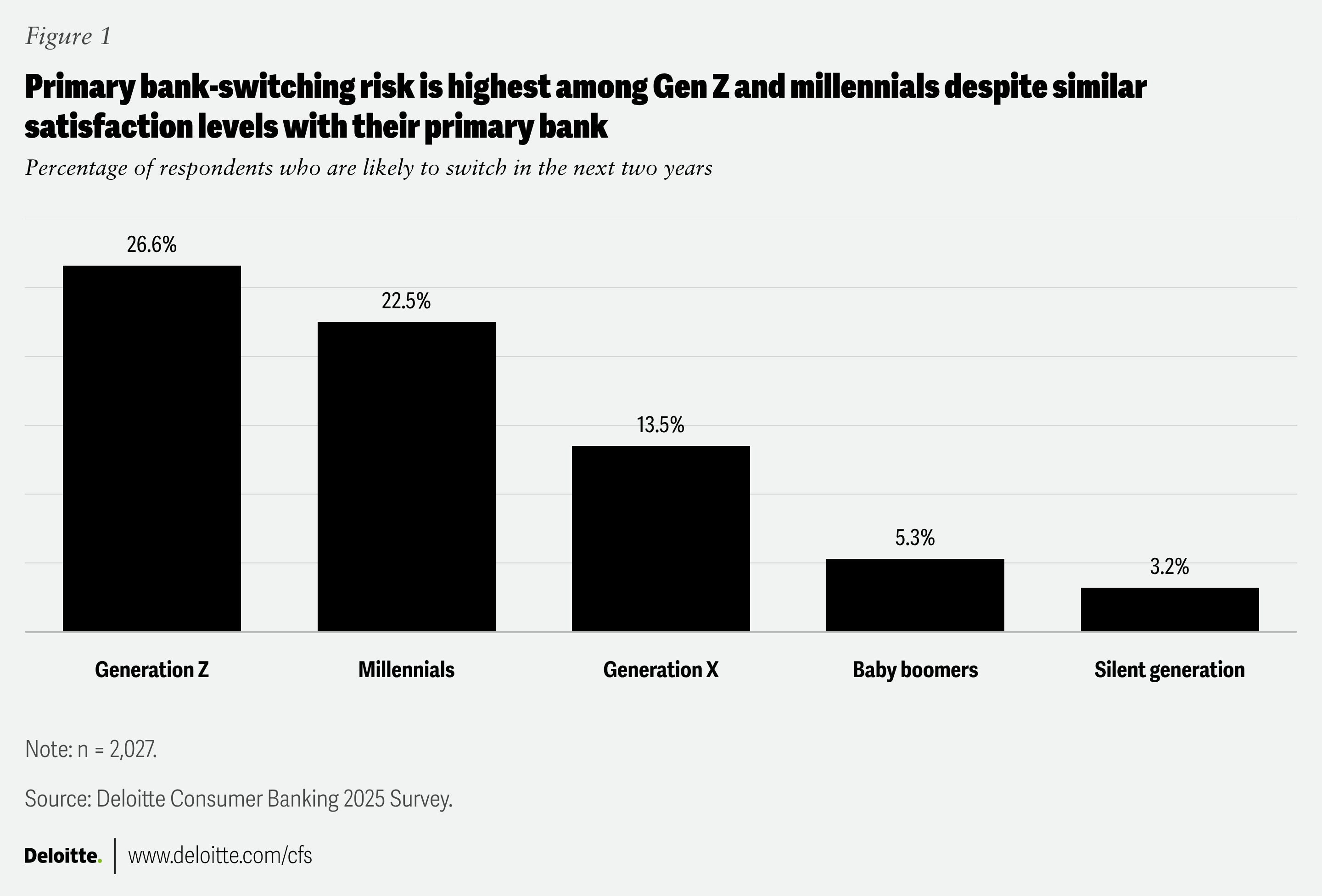

Switching risk rises even as satisfaction holds steady

Conventional wisdom in the banking industry equates customer satisfaction with customer loyalty.4 Historically, that has been true. But our survey findings challenge this premise (figure 1). Among all generations, Gen Z and millennials exhibit the highest risk of switching from their primary bank, even though their satisfaction levels are only marginally lower than those of older consumers. Satisfaction levels among all generations range between 93% and 95%, with the younger generations leaning toward the former. This pattern is not new. According to a FICO survey in 2014, millennials, even then, were five times more likely than those over 50 years old to close their existing bank account.5 This mirrors the current behavior of Gen Z, suggesting that younger generations have long been less likely to equate satisfaction with loyalty.

This disconnect between satisfaction and loyalty among Gen Z and millennials possibly signals a deeper shift,6 but it may also reflect something more practical: Younger consumers face fewer obstacles to switching. Their financial lives tend to be less complex—with fewer products, fewer long-standing relationships, and less friction in transferring accounts—so the perceived risk of moving to a new provider is lower. As a result, switching becomes easier, and the stakes likely feel smaller.

Even so, the pattern suggests that younger consumers, more so than older generations, do not view satisfaction as a reason to stay. A single moment of friction, whether a slow transfer of funds, confusing fees or a clunky customer experience overall, could trigger flight. Loyalty seems to have become more conditional among them, more so than among Gen X, the baby boomers, and the silent generation.7

Our survey data suggests millennials also show nearly identical switching intentions as Gen Z. Together, respondents seem to behave like a unified segment defined less by age and more by their digital expectations and variety-seeking behavior.

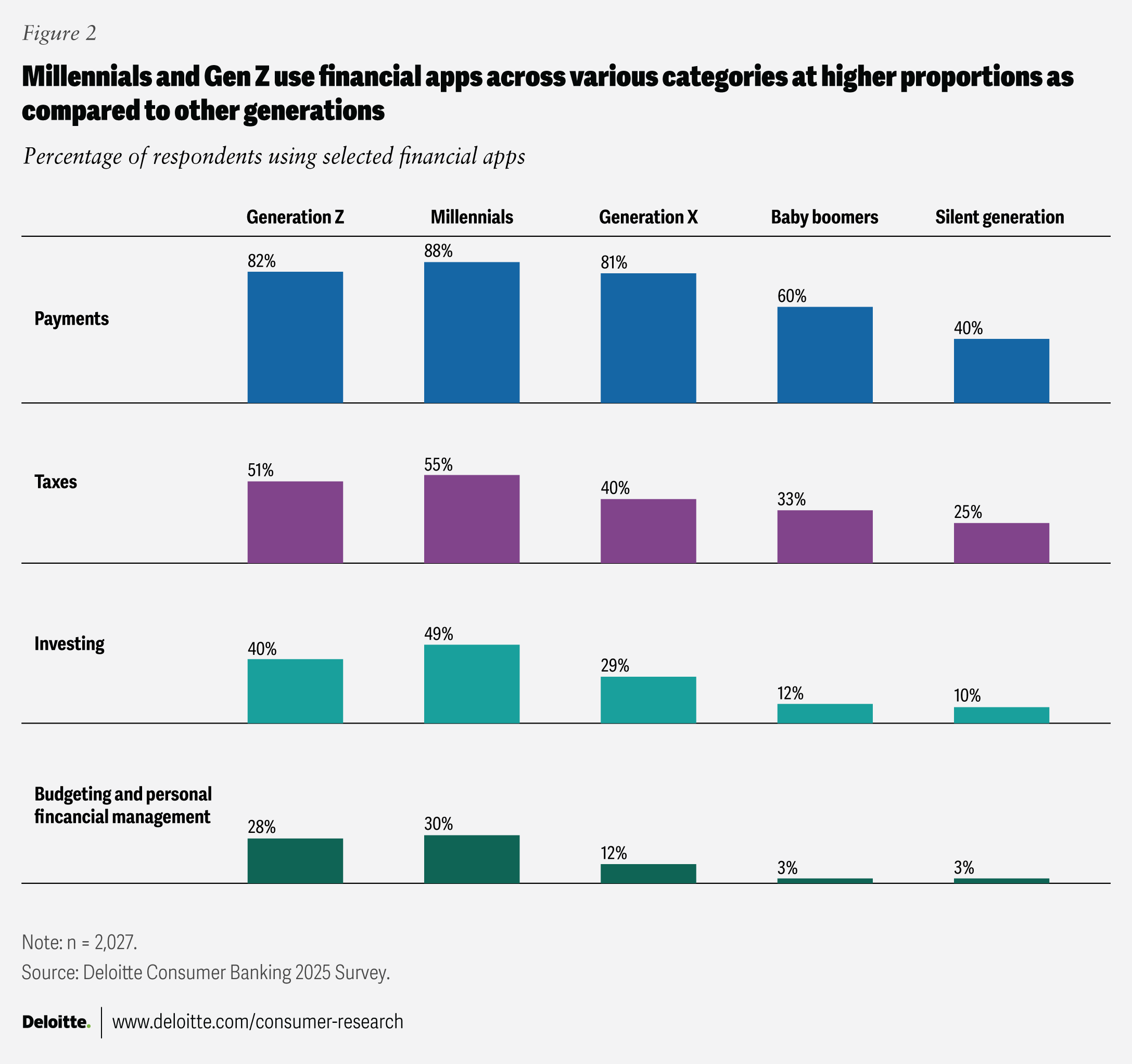

Financial lives are now built around apps

Many bank consumers use various financial apps—ranging from budgeting to taxes and investing—to manage their financial lives. Figure 2 shows how deeply both surveyed millennials and Gen Z depend on financial apps. In most categories, millennials lead in usage, but Gen Z respondents track closely behind, except for payments, where Gen X, millennial, and Gen Z respondents exhibit a similar level of preference.

This trend suggests something significant about the mindset of younger consumers. They do not tend to see banking as a contained relationship between themselves and a single institution. They seem to view their financial options in a more nuanced way—interconnected with tools and platforms, each optimized for a specific function,8 and not limited just to their financial lives. In response, banking applications in recent years have evolved into comprehensive ecosystems, offering users a wide range of additional services beyond traditional banking such as travel-related services, insurance options, and real estate tools. These apps enable customers to manage various aspects of their lives via a single platform.9 In this context, personal financial management tools could become a true differentiator for banks. To some degree, this is already evident in the strategies of neobanks in Europe.10

What older generations might consider fragmentation—such as the use of multiple financial apps and platforms—younger consumers seem to view as a desire for more variety and flexibility. This tendency further supports the idea that Gen Z and millennials are aligned in their banking behaviors.

Younger consumers in the survey seem to feel more in control of and are more willing to share financial data

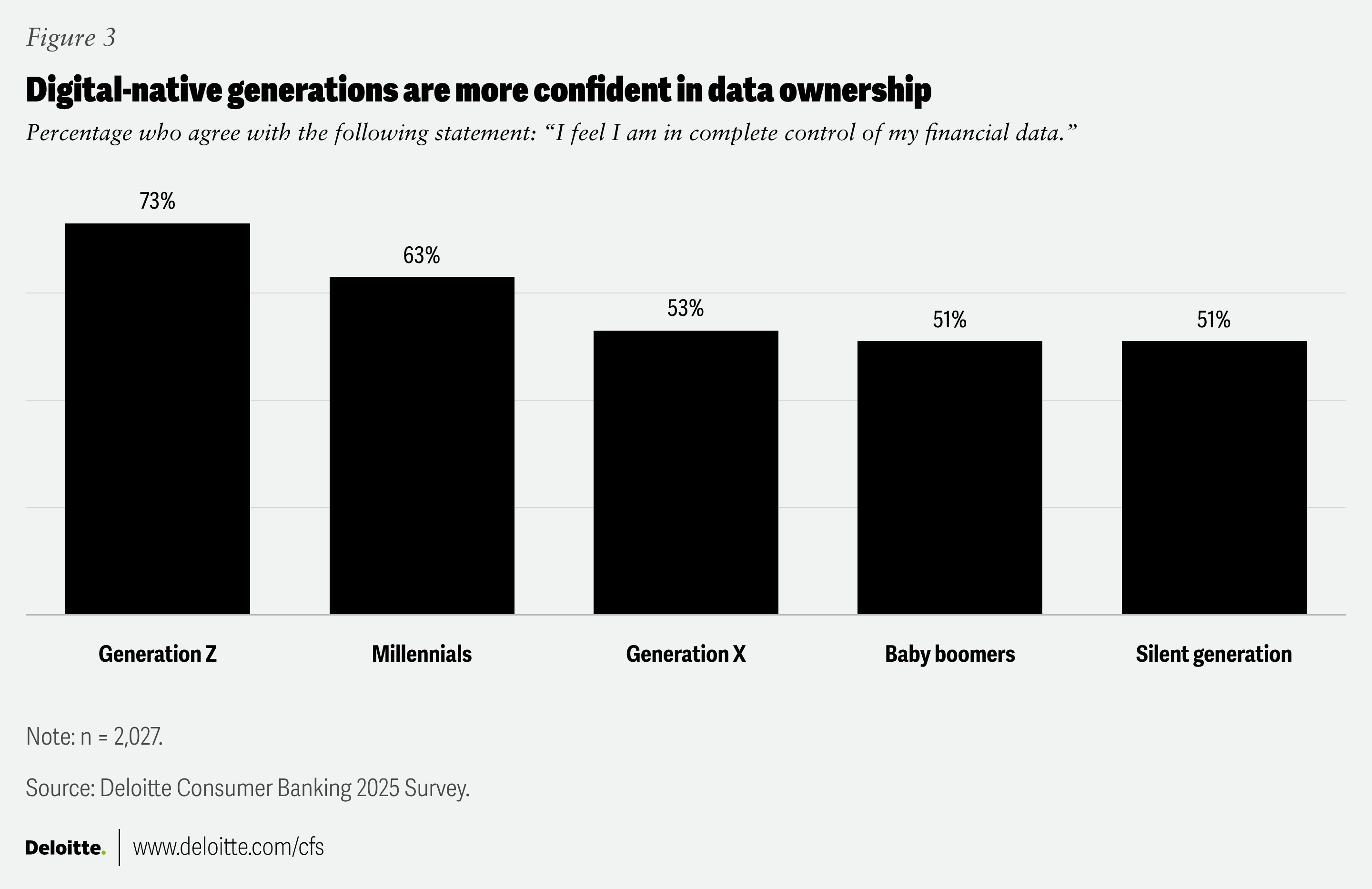

Perhaps the most counterintuitive finding appears in figure 3. Despite connecting their accounts to more apps and services than any other generation, surveyed Gen Z and millennials report feeling more in control of their financial data than baby boomers or Gen X.

How can the most data-sharing consumers feel so confident? Younger consumers are accustomed to permission screens, and toggles that grant or revoke access.11 Many are also very active on social media and appear comfortable with sharing their personal lives. This appears to make many seem less worried about their privacy.

Interestingly, other studies show that many have a lower desire for control over data.12 This mindset possibly influences behaviors on data-sharing. When people already feel in control of their finances, they often don’t seek additional control. The need for “more control” shows up mainly among those who feel they lack it in the first place and that’s what we see in our data.

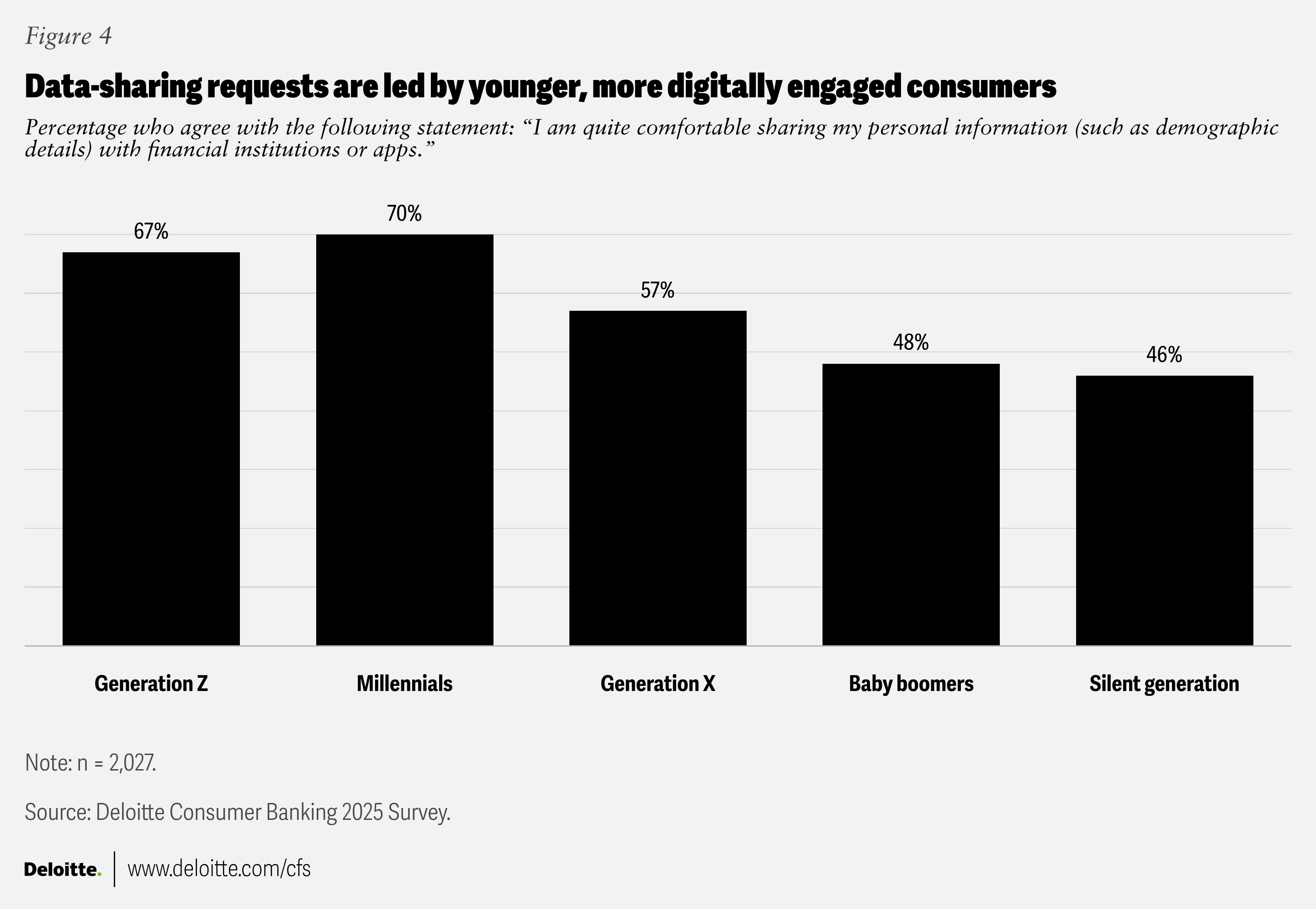

Figure 4 illustrates the logical extension of the “data control” notion. Nearly 70% of surveyed millennials and Gen Z have authorized their banks to share data with other financial providers.13 This is an active choice. Younger consumers appear to share data when it provides something meaningful such as better recommendations, loyalty benefits, or easier checkout and payment experiences.14

This suggests that open banking—where customers have the choice to share their financial data with other third parties—is already embedded in their expectations. They seem to want the flexibility to integrate apps, compare offers, and automate financial tasks across platforms.

The data points to overwhelming similarity among Gen Z and millennials respondents, but differences still matter though. Gen Z tends to be more spontaneous15 in spending and more reliant on social media for financial advice.16 Many also report lower financial literacy and are less swayed by legacy brand trust.17 Millennials, having lived through the global financial crisis, appear more financially resilient and confident in their saving and investing habits.18

Rethinking the generational playbook for banking

Banks should stop treating Gen Z and millennials as separate segments. The data shows they form a single continuum of digital-native customers with largely converged expectations. Their digital adoption, loyalty patterns, data-sharing comfort, and app usage all track the same.

Similarly, take the case of “buy now, pay later” (BNPL) services. Recent research suggests that millennials and Gen Z are more likely to use BNPL than older consumers.19 As younger consumers show greater preference for debit and BNPL solutions, debit rewards are likely to become even more important in customer acquisition and retention.20

The differences, where they exist, are likely to be due to financial needs based on their life stage as opposed to purely generational.21 For example, a Gen Z worker starting out and a millennial managing a household need different guidance and tools, but not different platforms. One digital core, enhanced with personalization features, can effectively serve both.

In practice, they function as one digital generation moving through different phases of financial life. The opportunity for banks may be to design for this unified segment based more on life stage needs rather than for outdated generational labels. Those who do may meet younger consumers in environments they are largely already familiar with: digitally fluent, value-driven, and expecting transparency at every step.

The future of banking is likely to be shaped less by generational divides and more by the rapid, irreversible integration of digital technology into every aspect of financial life. This could further be accelerated through the adoption of generative AI and agentic technologies across the banking value chain.

Consumer expectations—across age, background, or life stage—are converging around a few core truths: seamless digital access, hyper-personalization, and the ability to manage finances on consumers’ terms, whenever and wherever they choose. This is the wave of the future, and banks should consider redoubling their efforts to serve customers in such an environment.

Continue the Conversation

Meet the industry leaders

Nick Cowell

Val Srinivas

Shivalik Srivastav

by

Nick Cowell

Val Srinivas

Shivalik Srivastav

The authors would like to thank Hannah Bachman and Cintia Cheong for their contributions to this article.

Editorial: Cintia Cheong, Hannah Bachman, and Pubali Dey

Design: Meena Meena and Molly Piersol

Cover image:

Knowledge services: Rohan Singh

Visit the Deloitte Center for Financial Services

Access more insights for the banking & capital markets, commercial real estate, insurance, and investment management sectors.