How stablecoins could power the next era of retail payments

The rise of crypto-backed cards, agentic commerce, and merchant-issued digital currency could drive more than US$200 billion in stablecoin-enabled US retail purchases by 2030

Stablecoins are moving from niche crypto platforms to the checkout line. Beyond the incremental growth of direct payments, these instruments could support an estimated 2.5% of US noncash transactions through backend settlement, processing, or funding mechanisms by 2030.

In the near term, multinational companies may capture the most value from stablecoin networks due to the costs and complexity of wholesale cross-border transactions.1 But opportunities should quickly extend to retail commerce as the payments industry responds to growing demand for faster and more flexible experiences on both sides of the register. For businesses, stablecoin payment methods can reduce processing fees and improve cash flows.2 Consumers, meanwhile, are seeking easier ways to spend their stablecoin holdings on everyday purchases.3

Financial institutions are laying the groundwork for this shift by investing in infrastructure that can support higher transaction volumes on blockchain-based networks. Banks, for example, are ramping up issuance of tokenized deposits—a digital form of commercial bank money that offers stablecoin-like speed and programmability.4 Moreover, major card networks are expanding capabilities for multi-rail payments and stablecoin settlement to position themselves at the center of emerging payment flows.5 As stablecoins and tokenized deposits gain traction, money movement could eventually take place almost entirely on-chain.6

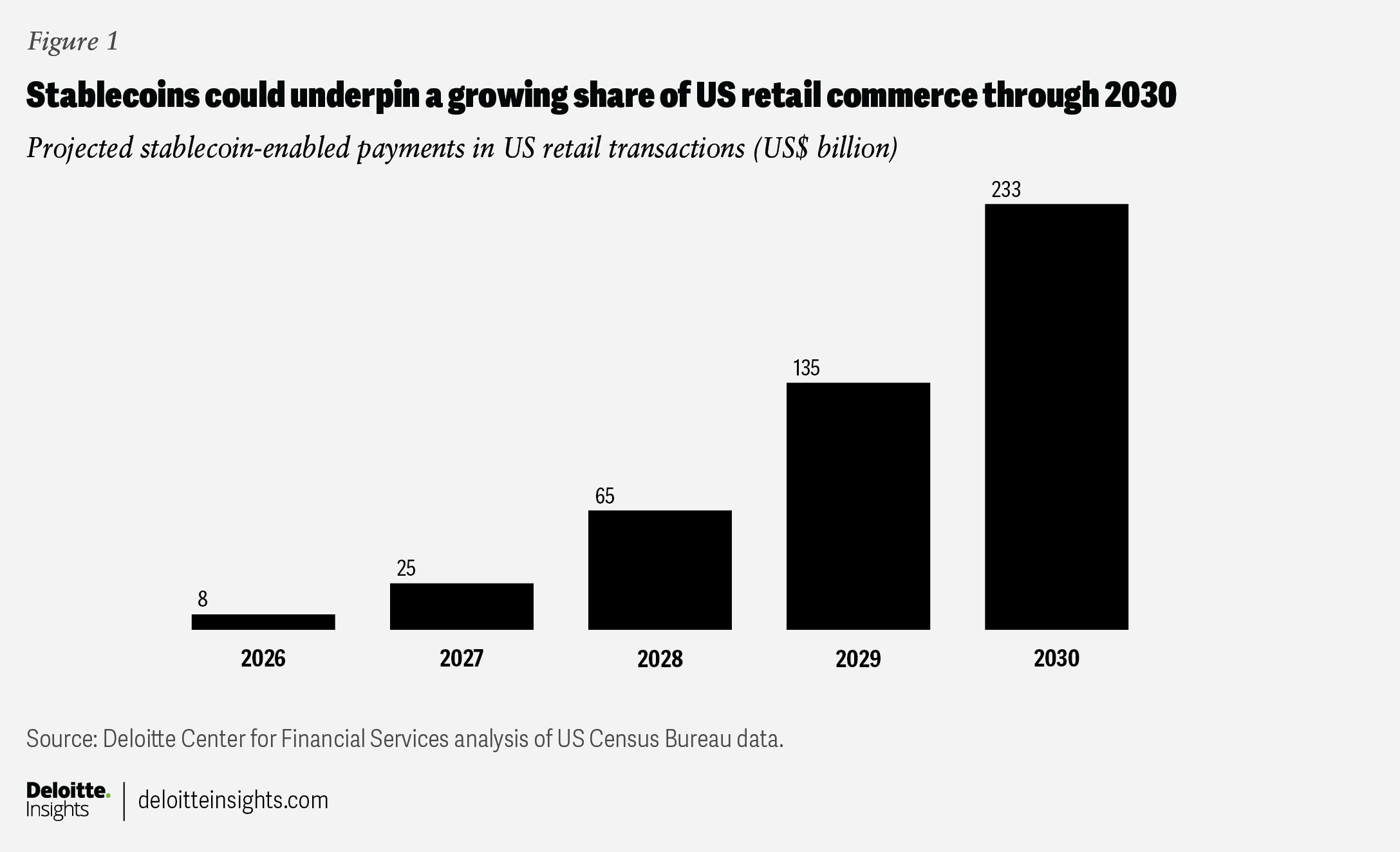

Over the next several years, three market developments could make stablecoins a more prominent fixture of mainstream commerce: the growth of stablecoin-linked debit and credit cards, artificial intelligence-assisted shopping, and branded loyalty programs. As these models take hold, Deloitte predicts that more than US$200 billion of US retail payments will be stablecoin-enabled by 2030 (see “About this prediction”).

What’s generating interest in stablecoin-enabled payments

Since last year’s GENIUS Act helped legitimize stablecoins as regulated financial instruments, retailers have been evaluating whether new payment flows may help relieve margin pressure. In the United States, payment processing fees often exceed 2% per transaction,7 making them one of the largest operating expenses for small- to mid-sized businesses.8 In addition, evidence suggests that early crypto adopters are gaining more spending power,9 and more Americans are using stablecoins for commercial payments.10

Businesses, however, face an uphill battle in enabling customers to pay with stablecoins directly at the register. Technical integration is a key hurdle, given that many point-of-sale terminals are configured to process payments through traditional card networks.11 Similar to the extensive hardware upgrades and industrywide coordination required for the multiyear transition to chip readers, integrating stablecoin payments could be a gradual and complex process.12 Even when plug-and-play options are available, businesses may need to invest in add-ons for their enterprise software to track on-chain transactions and comply with unique considerations for stablecoin accounting and tax reporting.13 For this reason, the first wave of domestic adoption will likely be driven by debit and credit cards issued by large networks with extensive merchant reach.

Agentic commerce could trigger the next stage of growth. As AI agents increasingly research, compare, and execute purchases on consumers’ behalf, they could prioritize the speed and adaptability of stablecoins. Further down the line, merchants may deepen adoption by tying rewards and incentives to branded stablecoins, creating network effects that drive more habitual use. Taken together, these developments could expand stablecoins’ role in US retail payments, with broader adoption reaching a potential tipping point around 2028 (figure 1).

Same swipe, new rails: How card networks are spurring early adoption

Major providers such as Visa and Mastercard could lead the push with stablecoin-backed cards that replicate the traditional card experience. In these transactions, customers swipe a card that draws on their stablecoin balance, much like a debit card.14 However, funds are converted into fiat currency at the point of sale, allowing merchants to accept payments in US dollars. Behind the scenes, the card networks coordinate settlement across relevant banks and intermediaries. These processes may be conducted through traditional channels such as Fedwire and automated clearing house systems or, in many emerging cases, by executing settlement in stablecoins using partner-supported programs.15

Since these debit-like transactions are funded by existing balances in users’ digital wallets, stablecoin-backed cards face minimal credit risk. They also bypass the need to fund credit card-like reward programs, another key driver of interchange fees. As a result, merchants may benefit from lower overall processing costs or receive a portion of the fee savings back from issuers through rebates or incentives. Customers, in the meantime, receive all the protections afforded by an established card network, including chargebacks, dispute resolution, and fraud management.

Looking ahead, financial institutions may use stablecoins to redesign credit products. Rather than relying on traditional lending models, issuers may offer credit tied to stablecoin balances held on-chain as collateral. Businesses using smart contracts to automate payments could also gain access to credit lines that dynamically adjust to their stablecoin holdings. In parallel, companies could issue treasury-backed corporate cards to employees, programmed with spending controls aligned with internal policies.

Agentic commerce could be another catalyst for growth

Agentic commerce could become the next pillar shaping new purchasing behavior. While today’s personal AI agents typically conduct one-off, human-initiated purchases, newer models may facilitate more continuous and rule-based transactions. For example, rather than checking if a retailer has replenished a clothing item, users can ask their agent to buy a jacket as soon as it’s available in their desired size and price range. Morgan Stanley estimates that almost half of e-commerce shoppers will use AI agents for personal spending decisions by 2030.16

The volume and velocity of autonomous transactions may require more seamless payment methods that reduce friction in agentic workflows. Traditional payment systems may obstruct agents with paywalls that require users to enter card credentials or complete human authentication. Because stablecoins can be held in preauthorized wallets and transferred programmatically on 24/7 payment rails, agents may prefer them for always-on payments that minimize interruptions in multistep transactions.17

For this reason, emerging protocols that govern how agents discover products and execute purchases are incorporating stablecoins as a native payment option alongside card and bank integrations.18 At the same time, card networks are looking to capture a dominant share of agentic transactions while preserving customer security. Major providers have launched virtual cards for agents that contain built-in fraud protection, spending limits, and merchant category restrictions.19 While many of these cards still run on traditional payment rails, they may integrate stablecoin funding or settlement over time.20

More advanced users may still opt to use stablecoins for more autonomous or high-frequency payments, especially microtransactions. Since stablecoins can be divided into very small increments, they may be more suitable for digital services priced too low to justify transaction fees. This growing class of digital resources includes application programming interface requests, AI compute, and access to specialized data.21

Merchants may hold the key to customer conversion

Merchant-led loyalty programs could help move stablecoins into everyday consumer use. By offering compelling incentives to pay with stablecoins, they may give customers a tangible reason to reconsider their choice of payment.

The structure of these programs may vary by merchant size and sophistication. Large, high-volume merchants may launch branded stablecoins to reinforce brand loyalty. While issuing proprietary stablecoins may demand large upfront investment, it can provide more flexibility to redistribute cost savings through customizable rewards, including immediate “cashback,” exclusive rebates, and targeted offers. Many large businesses may favor a closed-loop model that limits payments to their own stores, websites, and apps, possibly tying stablecoins to cards and wallets so the experience feels invisible to customers. Some retailers may join consortia to jointly launch a shared stablecoin with broader acceptance across their collective footprint.

Small- and mid-sized enterprises are also assessing reward strategies, although they may be more likely to adopt general-purpose or white-labeled stablecoins rather than issue their own. Many of these retailers may rely on third-party payment processors or e-commerce platforms to embed stablecoin acceptance into the checkout experience. Given these constraints, they may choose a more open approach, allowing stablecoins to be used across platforms, wallets, and vendors. In these arrangements, rewards programs could become more portable through partnerships with other merchants and platforms.

Merchants may also look for ways to channel yield generated from stablecoin reserves to fund additional customer incentives. The GENIUS Act prohibits direct interest payments to holders, but the forthcoming CLARITY Act on market structure may allow stablecoin sponsors to offer indirect rewards tied to payment activity.22 These perks may include product and shipping upgrades, voting power on company decisions, or subsidy programs that lower the interest rate on large purchases. Over time, competitive dynamics could shift toward retail brands that differentiate on the economic value embedded within their payment channels.

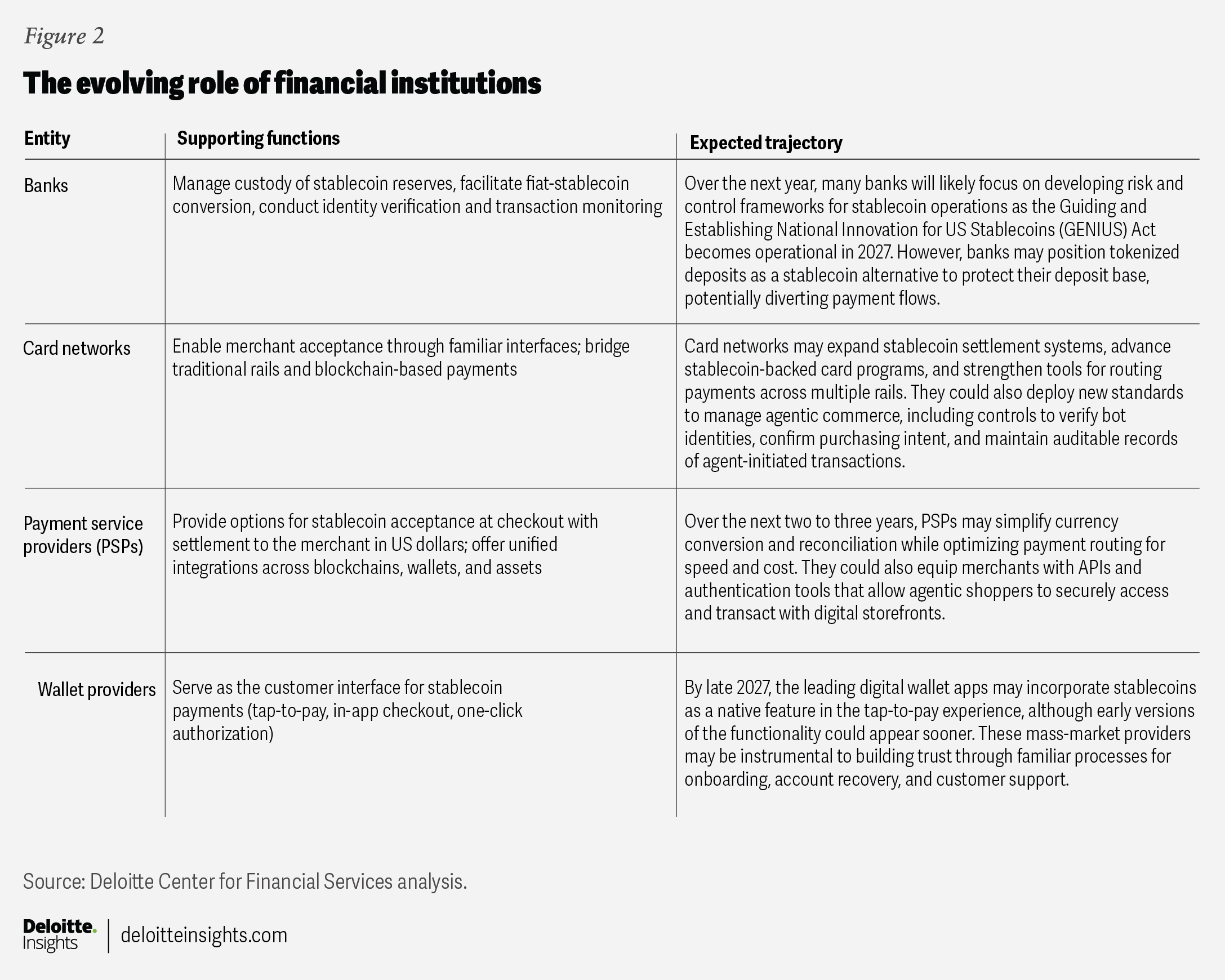

Roles financial institutions could play as stablecoin-enabled payments evolve

As stablecoin-enabled payments mature, the market is likely to evolve into a hybrid model in which established financial institutions support transactions through a mix of traditional payment infrastructure and stablecoin-based processes. Each entity can play a distinct role in accelerating payments innovation and the growth of agentic commerce (figure 2).

Collectively, these entities form an interconnected value chain in which banks provide safekeeping and credibility, card networks extend merchant acceptance, payment service providers orchestrate connectivity, and digital wallets serve as the customer interface. The inflection point for mass adoption may come when these capabilities converge into a cohesive experience that feels intuitive for both merchants and consumers.

About this prediction

Our forecast for stablecoin-enabled retail payments is based on the US Census Bureau’s monthly retail and food services sales data. We projected retail sales through 2030 using reasonable growth assumptions informed by historical trends, adjusting totals to exclude cash transactions that are less likely to transition to stablecoin-linked payment methods. Retail categories were then segmented into four groups with distinct adoption profiles (for example, where purchases are more commonly made in-store or online). Finally, we estimated what share of payments in each bucket could incorporate stablecoin capabilities, based on input from Deloitte specialists in blockchain, digital assets, and payments, as well as evidence from past payment adoption trends, customer research, and expected market conditions.

By

Tim Davis

Jill Gregorie

The authors would like to thank John Labate, Karen Edelman, and Rajiv Shah for their extensive contributions to this article.

They also extend their sincere gratitude to Patricia Danielecki, Anuja Sandeep Mhatre, Paul Kaiser, and Hannah Bachman for their invaluable guidance and support.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover artist: Sofia Laviano

Knowledge services: Agni Wagh

Visit the Deloitte Center for Financial Services

Access more insights for the banking & capital markets, commercial real estate, insurance, and investment management sectors.