Crypto and smart contracts unlock efficiencies across the commercial real estate fund life cycle

Funds are being rebuilt on-chain

Crypto markets may swing between hype and skepticism, but the technology supporting them is far steadier. Blockchain is drawing the attention of asset managers who recognize its potential to automate how money moves through the life cycle of a fund. Distributed ledgers and asset-backed stablecoins are catalysts that could reshape commercial real estate fund processes to facilitate transferability by reducing transaction costs and settlement time.

Central to this transformation are smart contracts—software protocols that automatically execute once predefined conditions are met. Asset managers are already testing their application across fund workflows, including subscriptions, capital calls, redemptions, and escrow releases. The technology could also reshape the roles that intermediaries play, making complex workloads more efficient and responsive.

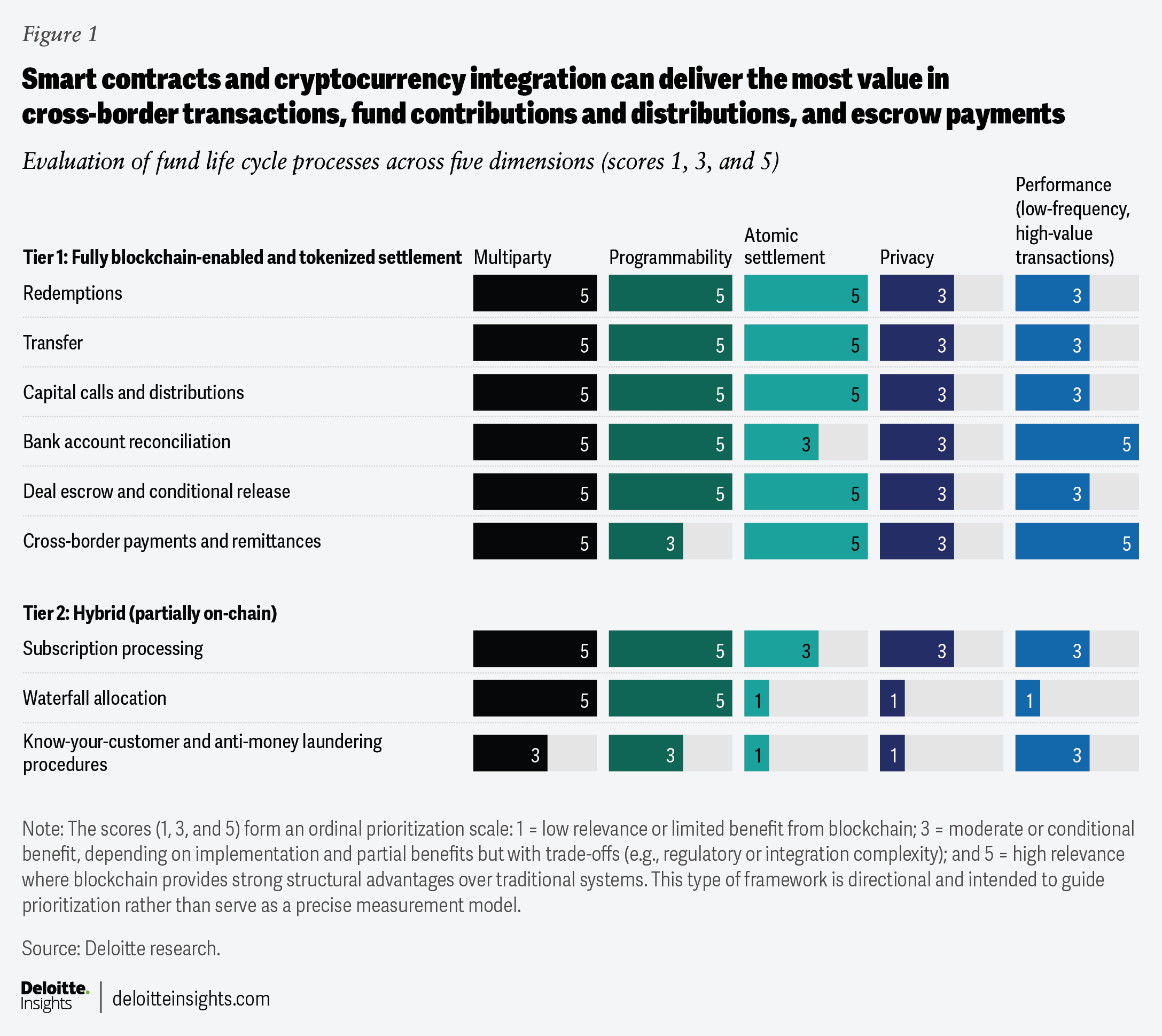

Over the next decade, that experimentation by real estate funds is likely to harden into standard practice. By 2030, most fund managers will likely use blockchain-enabled digital assets in at least one part of the fund flow process (see “About this prediction”). Our research has determined that the most viable points for smart contracts and cryptocurrency integration across a fund’s life cycle include investor-related transactions, cross-border transactions, fund contributions and distributions, rent and utility payments, and property operations (figure 1).

As financial institutions race to modernize fund operations, a clearer picture emerges where blockchain technology genuinely adds value and where it may not. Processes like capital calls and distributions, which require coordination of cash movements and ownership updates across multiple parties, are increasingly suited to full on-chain execution. With programmable smart contracts and the rise of tokenized assets and payment rails, these workflows can be automated end-to-end.

Most other high-potential use cases follow a more pragmatic path. They rely on hybrid architectures, where core logic and sensitive data remain off-chain while blockchain provides a shared layer for coordination, verification, and audit trails. By anchoring attestations and timestamps on-chain, firms can synchronize data across administrators, custodians, and investors without exposing confidential information. This model is particularly effective for onboarding, anti-money laundering (AML) and know-your-customer (KYC) reviews, and reporting, where privacy and regulatory constraints limit full on-chain adoption.

Enhancing fund formation, subscription, and investor onboarding processes

Fund operations today are slow and manual. Capital calls, in particular, move through emails, spreadsheets, and multiple intermediaries just to get money where it needs to go. Managers carefully time these calls to avoid “cash drag” or return dilution. Smart contracts could offer a cleaner alternative by validating investor eligibility and available capital instantly and then moving the funds only when all requirements are met. Over time, that could significantly reduce not-in-good-order exceptions and delays caused by missing, incorrect, or noncompliant information, as well as minimize the back-and-forth reconciliation that slows the process today.

Similar efficiencies can emerge during fund investor onboarding. AML and KYC checks are often completed manually and potentially even after transactions occur, driving up costs. In the United States, asset managers spend about US$2,600 for each institutional review, 13% more than peers in the United Kingdom and 23% more than counterparts in Singapore.1 Embedding these checks directly into transaction protocols could allow funds to screen investors automatically, enforcing jurisdictional and accreditation rules in real time.

Making ongoing operations real-time and more efficient

In real estate funds, blockchain can likely solve post-onboarding inefficiencies, particularly in redemptions, transfers, and net asset value (NAV) information updates by reducing delays, improving record synchronization across parties, and enabling investors to act on more timely and transparent fund data.

Valuation and distribution

Fund reporting today is often slow, fragmented, and backward-looking—hardly the service many clients expect in a digital-first world.2 Investors want a clear, up-to-date view across their portfolios, not just periodic snapshots of stale history.3 NAV calculations may rely on external data feeds, but their dissemination and audit trails can be embedded within smart contracts, enabling stakeholders to access and verify both pricing inputs and historical data with greater ease. More frequent and transparent NAV updates also allow redemptions to be priced more accurately, reducing the risk of investors entering or exiting based on outdated information.

Some fund managers are starting to automate how assets are valued and how returns are computed. A real estate investment trust (REIT) has to distribute at least 90% of its income every year or it loses its favorable REIT status. Smart contracts could help calculate and execute distributions to mitigate the risk of losing this status. This also means they should expect more distributions from these types of investments than they might expect from other investments, so smart contracts can help provide speed, clarity, and tracking to distributions.

AI-driven valuation models can automate cash flow forecasting, introducing more dynamic approaches to capital appreciation calibrated to asset utilization and macroeconomic conditions. Early pilots like Citigroup’s tokenized fund, in collaboration with Wellington Management, show that this is no longer theoretical. Distribution and waterfall rules are encoded directly into the fund’s architecture, ensuring that payouts follow agreed seniority and tiering. No manual intervention is needed.4

Redemptions and transfers

Fund redemptions today can be slow due to prescriptive rules for fund liquidity. Redemption terms—like lock-up periods, liquidity thresholds, and NAV calculation processes—can be built directly into digital systems and handled automatically. When an investor triggers a redemption, a smart contract can automate redemption approval and payment at an agreed price, at which point stakeholders are updated in real time and with an audit trail.

Complex assets like digital infrastructure contain even more opportunities for efficiency improvements. Funds dealing with data centers, fiber, and wireless networks can have development cycles, modular capital deployment, and complex revenue-sharing arrangements that span 10 years to 20 years, making capital flows difficult to manage. The manual layers controlling these processes may not keep up. Automated, rule-based systems are more than just an upgrade; they may be essential for managing capital efficiently at scale.

Why cryptocurrencies are gaining favor in CRE transactions

The real estate industry, often seen as slow to change, is proving receptive to cryptocurrencies. Digital assets are being used not only in property sales but also for rent and utility payments, with adoption likely to grow as regulatory clarity catches up. About 14% of US adults now hold crypto,5 and that ownership is beginning to influence how transactions are funded and executed.

Crypto-denominated leases for rent payments and utilities, as well as sale transactions have started to become more common. In a May 2025 survey, Redfin found 12.7% of recent Generation Z and millennial homebuyers sold cryptocurrency to help fund their down payment,6 while The Lurie Group reported a 35% increase in crypto-wealth-enabled home purchases over the last year.7

Stablecoins are also becoming a practical alternative for moving money globally, and real estate fund managers may need to get on board to meet payment expectations. Companies are using stablecoins to settle cross-border transactions faster and at a fraction of the cost—cutting fees from US$2,000 on a US$100,000 transfer to less than US$100,8 while reducing settlement times from days to seconds. Stablecoin transaction volumes hit US$33 trillion in 2025 and could reach US$56 trillion by 2030.9

Adoption is moving beyond experimentation. Nearly 75% of family offices are now investing in or exploring crypto.10 For global sectors like real estate, where US$64 billion crossed borders last year,11 this creates a clear opportunity. And as more banks and financial institutions explore issuing their own stablecoins, the underlying payment rails are becoming increasingly important. Employing a “stablecoin sandwich” strategy—in which a local currency is converted into stablecoin, moved globally in seconds, and converted back into local currency on arrival—offers a way to sidestep local currency volatility while preserving the familiar experience of fiat-to-fiat transfers, pointing to a potentially durable evolution in global money movement.

Capitalizing on a clearer regulatory environment

Recent regulatory changes are bringing more clarity, especially on cross-border issues. Last year’s GENIUS Act, the first US federal law to set standards for stablecoin issuance and custody, spells out who can issue stablecoins, what reserves must be managed, and what disclosures are required.12 It also grants holders priority claims in an insolvency, an added layer of protection that can strengthen risk management and holdings by corporate treasuries.13 At the same time, the CLARITY Act continues to advance in Congress, offering to establish a clearer market structure and framework that more closely resembles traditional banking.

Blockchain enablement may require technology updates

Internally, real estate firms can optimize fund flows through smart contracts and tokenization on permissioned blockchains with controlled access. Externally, they can transform cross-border payments using stablecoins on public networks to capture speed, cost, and liquidity advantages.

The foundation of these technologies is a blockchain network, which may be public or private. Smart contracts automate fund flow processes based on predefined rules and conditions, while a connection layer enables backend systems or middleware to read blockchain data, trigger transactions, and integrate on-chain activity with fund workflows.

Where external inputs such as pricing, payment status, or other verified third-party data are required, oracles bring that information on-chain. A custody and wallet layer manages private keys, transaction approvals, and user access. An audit and control layer supports compliance through transaction monitoring, proof-of-reserve checks, and oracle governance. Finally, supporting infrastructure such as cloud hosting, security frameworks, and access controls underpins reliability and regulatory compliance.

Actionable guidance

- Pick workflows to pilot with measurable KPIs: Consider starting where blockchain can add clear value in capital calls, distributions, escrow, or other milestone releases, then define success metrics (cycle time, reconciliations, fees, and error rates) and set a pilot window.

- Define treasury, liquidity, and risk policies for digital assets: Consider setting rules for stablecoin exposure limits, approved issuers and chains, conversion timing (“stablecoin sandwich” steps), counterparty risk reviews, and stress scenarios for regulatory actions.

- Design compliant and secure identity frameworks from the outset: When integrating standards such as ERC-1400 or ERC-3643 for on-chain identity registries and KYC or AML checks, prioritize robust identity verification, access controls, and regulatory alignment. Given their technical complexity, these features should undergo thorough security audits and continuous monitoring to mitigate exploitation risks and ensure compliance with evolving regulatory requirements.

- Utilize a qualified third-party custodian: That should employ multi-signature controls for digital assets and offer cold storage to ensure these digital assets are kept offline when needed.

- Integrate proprietary application programming interface solutions that handle on- and off-ramping: This should include fiat-to-crypto and crypto-to-fiat conversions, along with cross-network transfers. These features can enable users to move capital across blockchains and geographies while experiencing a straightforward fiat-like transaction process.

About this prediction

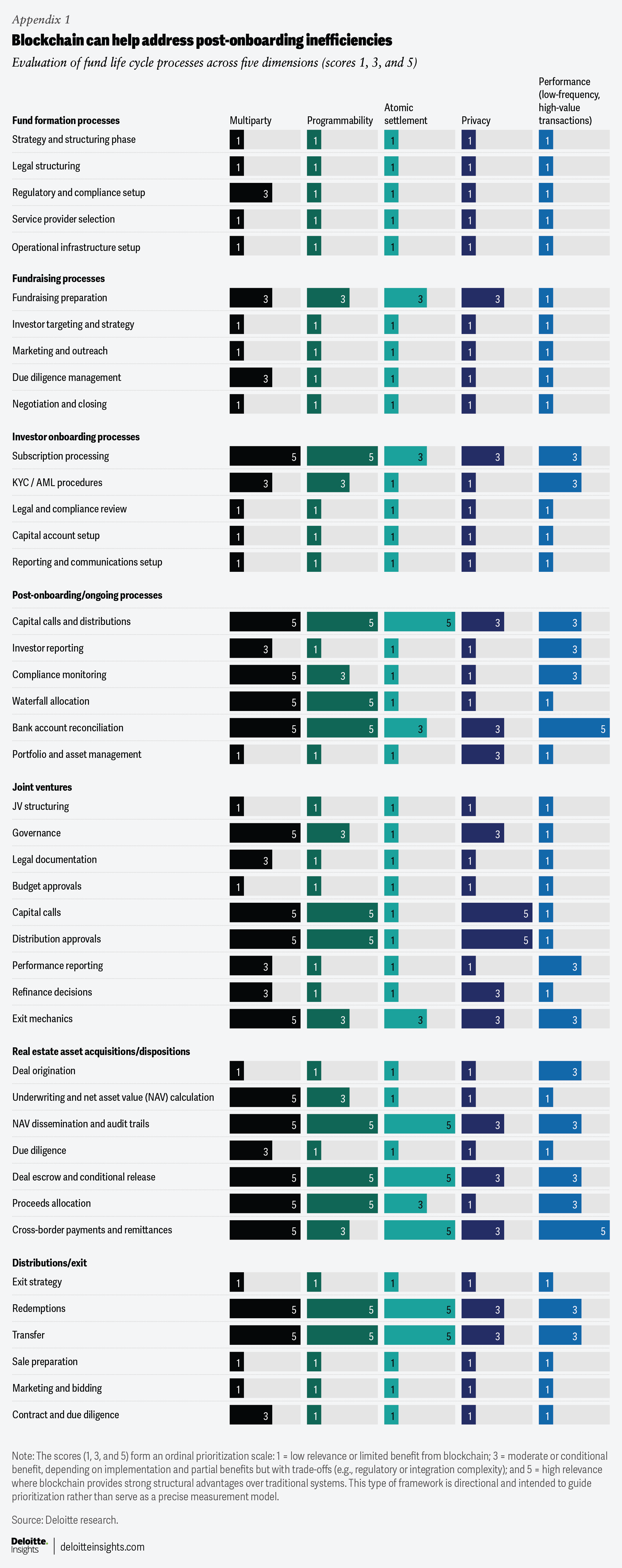

Each process within the fund flow life cycle was evaluated across five dimensions.

- The extent of multiparty coordination and reconciliation pain: Recognizing that blockchain is most effective when there is no single trusted source of truth and significant effort is spent reconciling data across parties.

- The level of programmability: Assessing whether workflows can be codified into deterministic rules (eligibility, fee logic, cutoffs, approvals) suitable for smart contract execution.

- Requirements for atomic settlement (transfer of an asset and its corresponding payment occur simultaneously): Particularly relevant in scenarios where linking cash movement with ownership reduces timing risk and intermediaries, such as capital flows, transfers, escrow, and redemptions.

- Privacy fit: Evaluating whether sensitive data can remain off-chain while leveraging on-chain attestations or proofs.

- Volume and performance considerations: Can the process be incorporated to ensure alignment with blockchain’s strengths in low-frequency, high-value transactions?

Processes were scored on a standardized scale (low, medium, and high) and translated into a quantitative ranking to enable comparison across the fund life cycle. Scores of 1, 3, and 5 correspond to weak, conditional, and strong fit, respectively, with an aggregate score (out of 25) used to prioritize use cases. Our detailed assignments are categorized in the table below, with the most viable cases across each phase highlighted.

by

Rob Massey

Brian Ruben

Tim Coy

Parul Bhargava

The authors wish to acknowledge Anuja Sandeep Mhatre and Gaurashi Sawant for their extensive contributions to the development of this report.

They would also like to thank their colleagues Tim Davis, Nathan Galvan, and Brian Hansen for their insights and guidance.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover artist: Sofia Laviano

Knowledge services: Vanapalli Viswa Teja