Agentic AI could help US life insurers reach new customers and narrow the coverage gap

AI can help life insurance shed its reputation as an industry where products are sold, not bought, especially for unserved and underserved consumer segments

For many years, the US life insurance market has faced a basic growth problem: The stated need from consumers is high, but purchase follow-through can be decidedly weak. While the market continues to post strong sales, with new annualized premiums reaching US$17.5 billion in 2025,1 a recent Insurance Barometer survey found that 40% of US adults say they need life insurance or need more of it.2 This disconnect suggests that the issue is not whether households value protection, but whether the industry can help more uninsured and underinsured people move from broad awareness to informed action.

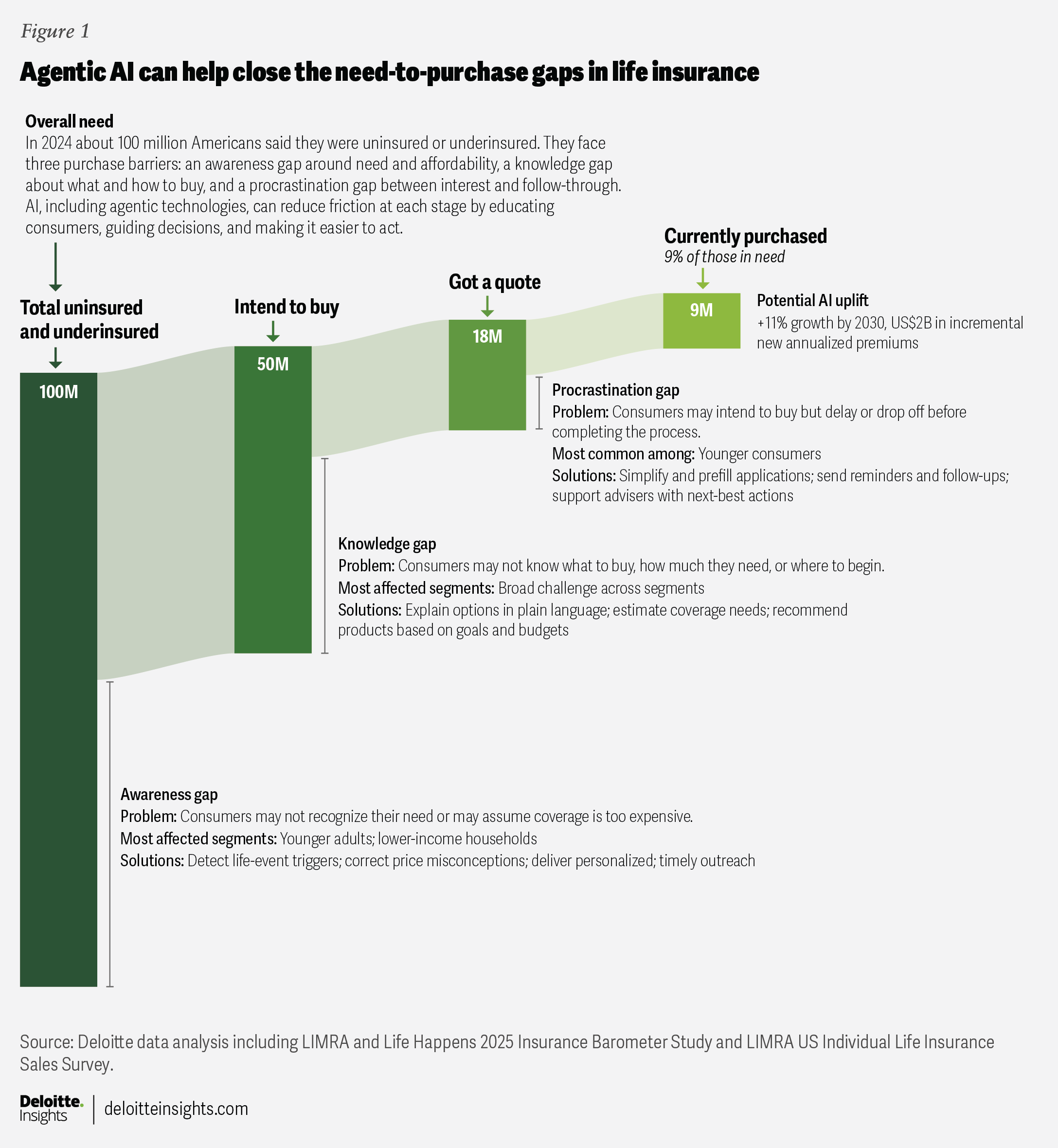

As agentic AI matures, it could play an important role in helping close the gap. The Deloitte Center for Financial Services predicts that by 2030, agentic AI embedded in life insurance distribution could add US$2 billion in annual incremental premiums in the United States (with a range of US$400 million to US$5.2 billion). The center also predicts that AI could increase new annualized individual life insurance premiums in the United States by 11% by 2030 (with a range of 2% to 27%), pushing the market to US$21.2 billion in total premiums instead of US$19.1 billion expected without AI (see “About this prediction”).

Introducing AI in life insurance distribution is not about replacing human agents but about reducing friction across a buying journey that too often stalls. Technology can help consumers understand why coverage matters, what it may cost, and what type of policy may fit their situation. AI can also help carriers and distributors identify life events, personalize outreach, support human agents before and after meetings, and keep smaller cases from falling out of the sales funnel.

AI’s role in reaching the unserved and underserved

The life insurance gap in the United States has evolved due to a complex set of related obstacles. Perceived cost remains the top reason people do not own life insurance or do not own enough of it, cited by 46% of respondents in a 2025 Insurance Barometer Study by LIMRA.3 That perception is especially acute among younger adults, who often overestimate costs by roughly 10 to 12 times the true cost.4 When the price anchor is that far off, many households never seriously enter the market.

Moreover, many consumers in the Barometer survey do not feel equipped to make a product decision: In fact, 22% of respondents say they are not sure how much life insurance they need or what type to buy. Another 21% cite procrastination as an obstacle.5 This life insurance need gap remains concentrated in segments that could matter greatly to future industry growth, including younger households, lower-income families, women, and Black and Hispanic consumers.6 For these demographics, AI’s value may lie in removing these everyday barriers. It can communicate with cultural nuance, educate in easy-to-understand language, and prompt action at the time of a life event (figure 1).

AI’s role in distribution will likely have commercial and social applications. Commercially, AI can help carriers and distributors reach more households at a lower marginal cost compared to manual outreach. Socially, it can help narrow a protection gap that has proven stubborn for years. In a category where misunderstanding is common and inertia is powerful, the ability to deliver timely, personalized, low-pressure guidance could matter more than another product feature, marketing slogan, or brand ambassador.

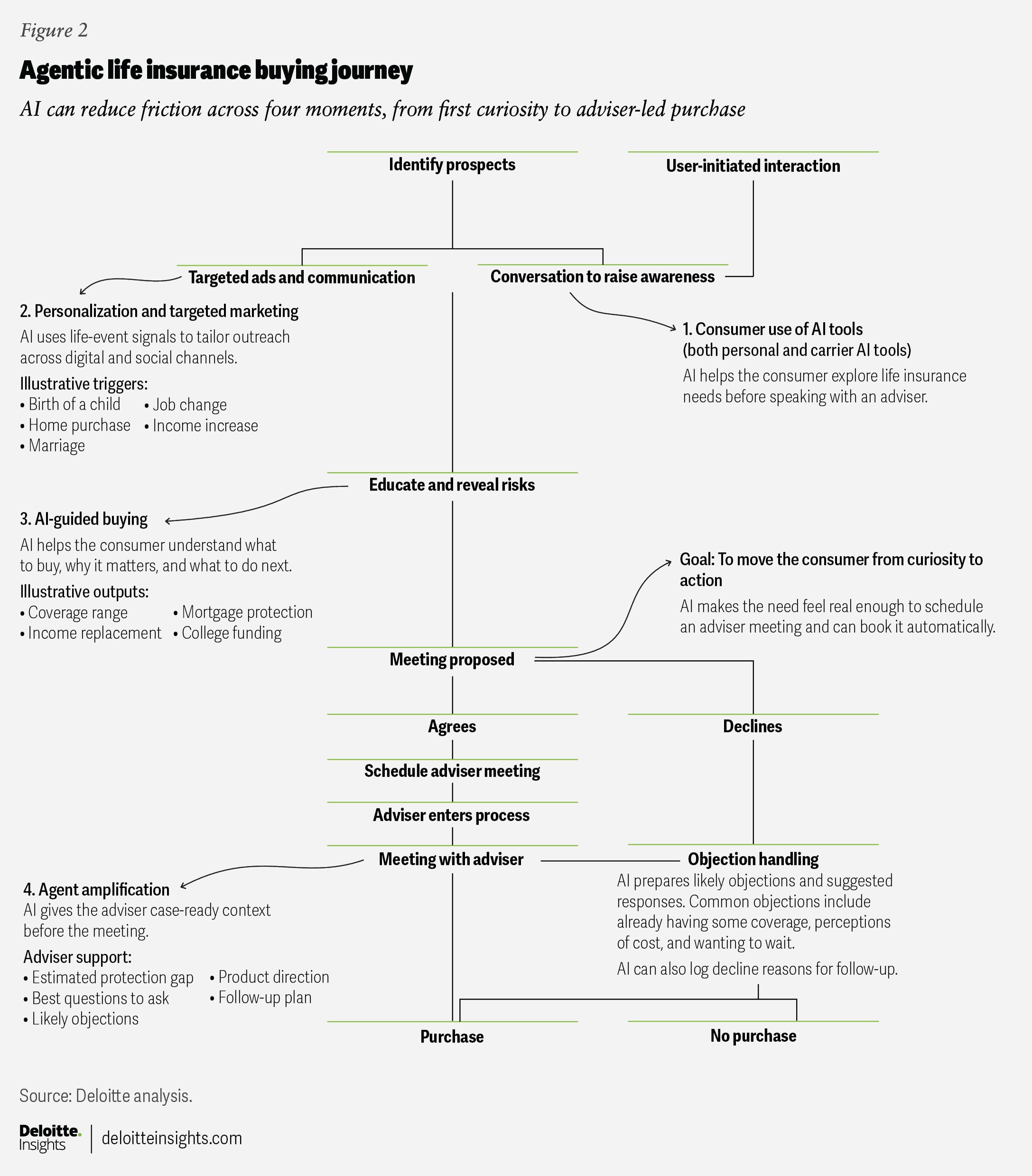

Four big AI moments unfolding in the life insurance–buying journey

The impact of AI on life insurance policy sales will likely develop across the following four moments in the buying journey.

1. Consumer use of personal AI tools to explore insurance needs and options: In the 2025 Insurance Barometer Study, 51% of responding consumers said they would use an AI tool to research life insurance, and 55% would use one to shop for it.7 This shift is consistent with a broader pattern across industries, where consumers are becoming more open to using AI tools for research, guidance, and decision support. AI is becoming part of the self-education layer of the journey, especially before a person is ready to speak with an adviser. “A Gartner® survey of 365 US consumers, conducted in July and August 2025, found that 51% of consumers say their research habits have changed due to gen AI.”8

2. Personalization and targeted marketing through AI agents: Life insurance demand is highly event-driven. Marriage, a home purchase, a new child, a job change, or a jump in income can all create triggers for protection. Yet, many carriers still struggle to reach the right household with the right message at the right time, especially when the case size would likely be modest. Agentic AI can change that by monitoring signals, tailoring content, and starting simple conversations that can help explain the need in more concrete terms. Outside of insurance, consumers are already using generative AI as a recommendation engine: Adobe found that 39% of consumers have used generative AI for online shopping, including 47% for product recommendations and 43% for deals.9 The insurance industry can therefore use AI to show up in those moments with more relevance and less friction (figure 2).

3. AI-guided buying on digital channels: In life insurance, too many journeys still depend on long forms, unclear steps, and a hard handoff between education and purchase. An AI conversational interface can explain product basics, gather information progressively, prefill parts of the process, and keep the buyer moving. Further, as agentic capabilities expand, more sophisticated underwriting operations could take potential buyers through to instant-issue digital policies. Adobe found that traffic to US retail banking sites from generative AI sources rose 1,200% from July 2024 to February 2025, and that those visitors spent 45% more time browsing once they arrived, suggesting that AI-referred users are often more engaged by the time they reach a digital destination.10

4. The most important moment of all—agent amplification: Here, the value is not only better efficiency, but better advice delivery. AI can prepare a case summary, estimate a protection gap, suggest discovery questions, surface likely objections, and draft a follow-up. That would allow human advisers to spend more time earning trust, applying judgment, and helping households make a confident decision. JD Power found that 27% of current do-it-yourself investors say they are likely to use a financial adviser in the next 12 months, rising to 37% among Gen Y and Gen Z investors.11 At the same time, financial services research firm Cerulli Associates found that 42% of bank advisers already use AI capabilities and 77% expect to incorporate them within two years.12 AI may reshape the top of the funnel, but human advice and relationship building should remain central at the point of commitment.

Strategies to position life insurance carriers for AI-enabled distribution

Insurers will likely need to develop a strategy to appeal to a new class of customer: AI agents. As consumers increasingly use AI tools to research, compare, and shortlist options, carriers will need to think beyond traditional search marketing. Product information should be clear, current, structured, and easy for AI systems to retrieve and explain accurately. In practice, that means plain language descriptions, transparent coverage explanations, and fewer gaps between what a prospect reads online and what an adviser later says in person. Mastering the emerging sphere of agentic search engine optimization will likely be crucial to staying relevant as the internet evolves to accommodate agentic commerce.13

Insurers may also benefit from investing in personalized outreach. AI can make it more economical to serve middle-market and smaller ticket opportunities that have historically been hard to pursue profitably. That does not mean flooding consumers with more automated messages. It means using AI to identify moments that matter, speak to the specific concerns a household may have, and offer a path forward that feels useful rather than pushy. For some carriers, especially those with broad customer bases in adjacent lines, this may create a practical way to widen the reach of life insurance conversations that rarely happen today.

Forward-thinking insurers should consider reconfiguring agent workflows to help them shine. The opportunity is to build AI into pre-meeting prep, needs analysis, quoting support, objection handling, and follow-up communications so that human agents can spend less time on administrative work and chasing leads, and more time advising. Success in the long term could then be measured not just by efficiency but also by policy count growth, better conversions on smaller cases, and stronger reach into segments where stated need remains high.

AI can go a long way toward removing the friction that currently inhibits unserved and underserved consumers from securing life insurance. Insurers that use AI to demystify and simplify, while catering to how customers are using these tools, stand to see the most potential gains. Ultimately, these actions can help the industry serve more households and close the insurance gap. The firms that move early may be best positioned to improve distribution economics and earn relevance in a market where consumers increasingly expect guidance to be immediate, personalized, and easy to act on.

About this prediction

Our analysis draws on four inputs: market size, industry adoption, current sales gaps, and ticket size. We used LIMRA and Life Happens Insurance Barometer data to estimate the uninsured and underinsured market. We then assessed how agentic AI could be adopted across independent, captive, and direct distribution channels by agents, customers, and carrier employees. Next, we identified the main barriers to life insurance purchases today, including awareness, knowledge, and procrastination gaps, and mapped those against willingness to use AI across age and income groups. Finally, we estimated the average policy size tied to AI-enabled conversion using a weighted average of the remaining market across age and income bands. Deloitte analysis and assumptions were then used to estimate the potential impact on new US individual life insurance annualized premiums by 2030.

BY

Reetika Fleming

Corey Arnouts

Bill Jarmuz

The authors would like to thank Dishank Jain for his contributions to the article.

Editorial: John Labate, Hannah Bachman, Karen Edelman, Cintia Cheong, Stacy Wagner-Kinnear, and Anu Augustine

Design: Sofia Laviano, Sylvia Chang, and Guido Agüero Gonzalez

Audience development: Maria Martin Cirujano and Kelly Cherry

Cover image by: Sofia Laviano

Knowledge services: Rishitha Bichapogu