Bridging insurance gaps to prepare homeowners for emerging climate change risks

Deloitte’s survey of homeowners in US states with high climate change risk reveals skyrocketing costs and widening gaps in insurance coverage.

Imagine this: A late-spring storm rips through a Georgia suburb, tearing off roofs, shattering windows with golf ball-sized hail, and flooding basements with the swollen currents from an overflowing nearby creek. When homeowners go to file an insurance claim, though, they discover their policies do not cover these unusual natural events.

Unfortunately, this isn’t just a nightmare scenario. It’s an increasingly common reality for millions of homeowners in an era with more frequent—and more severe—weather events like these. Between 2019 and 2022, the number of severe climate-related disasters in the United States escalated by 32%, causing insured losses over the same period to rise by nearly 300%.1

For insurance executives, this scenario not only exposes a gap in coverage that could lead to customer dissatisfaction and reputational risk, but also presents a missed opportunity for expanding policy offerings and increasing premium revenues in response to evolving climate risks.

Several US insurers are reacting to this untenable situation by either limiting—or entirely withdrawing—coverage in disaster-prone areas, such as California and Florida.2 In markets at high risk of climate-related damage, insurers have also introduced double-digit rate hikes3 that are making it challenging for many homeowners to maintain their coverage.

While climate change may be fuelling these disasters,4 another factor driving up losses is housing demands. Even in the face of rising climate risks, Americans continue to migrate to natural disaster–prone areas like California and Florida, often building higher-value homes in these regions.5 For example, between 1990 and 2020, nearly 44 million homes were built in wildfire-prone zones.6 This increases the concentration of natural catastrophe risk in homeowner insurers portfolios.

For generations, homeowners relied on their insurance policies as a safety net—a promise of resilience in the face of the unexpected. But what happens when the unexpected becomes all-too-frequent to the point that makes insuring some assets uneconomical? What can homeowners do if their safety net starts to fray? And how can insurers adapt and find opportunities in this challenging environment?

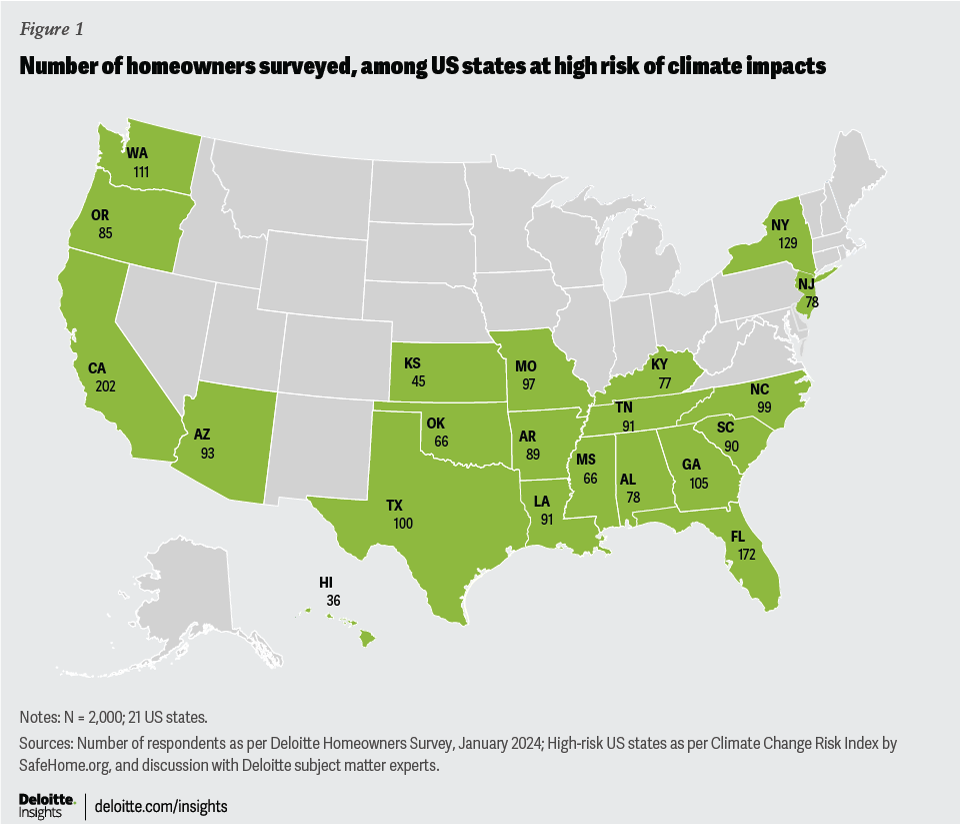

To gain insights into factors contributing to these coverage gaps and to identify solutions that could promote resiliency in the residential insurance landscape, the Deloitte Center for Financial Services surveyed 2,000 US homeowners from 21 states that are at high risk of climate-related disasters (figure 1). Fielded in January 2024, the research targeted respondents who said their coverage is inadequate. The sample reflected a demographically diverse respondent pool across the dimensions of age and income.

{kind=link}

Deloitte research reveals that respondents are generally dissatisfied with shrinking coverage options and skyrocketing costs of their residential insurance policies, which is making homeownership even more challenging for many. A concerning trifecta of challenges can stand in the path to securing adequate insurance.

Insurers’ retreat from high-risk areas is reducing market access for homeowners

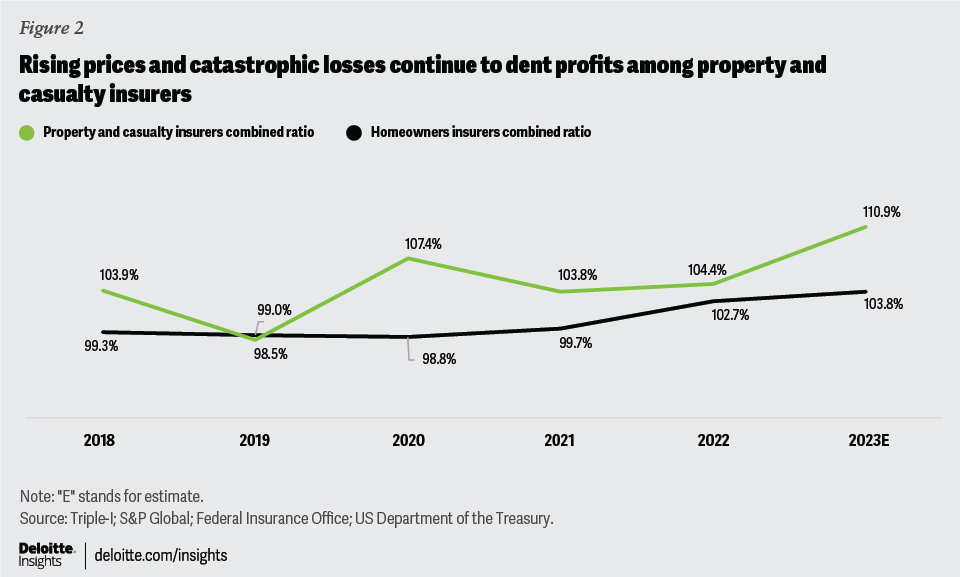

The combination of frequent losses and higher repair costs is squeezing insurers’ profitability, represented by a higher combined ratio for the homeowners’ insurance segment (figure 2). In response, several insurers appear to have already withdrawn or minimized coverage from some high climate-risk areas, a move that impacts the overall availability of coverage options. In California, for example, where many insurers have announced pullbacks due to increased wildfires, it has been estimated that there is a 20% reduction in insurance availability.7 According to Deloitte’s survey data, 23% of respondents said they are struggling with shrinking insurance options.

{kind=link}

Steep premium hikes to restore profitability have created an affordability challenge

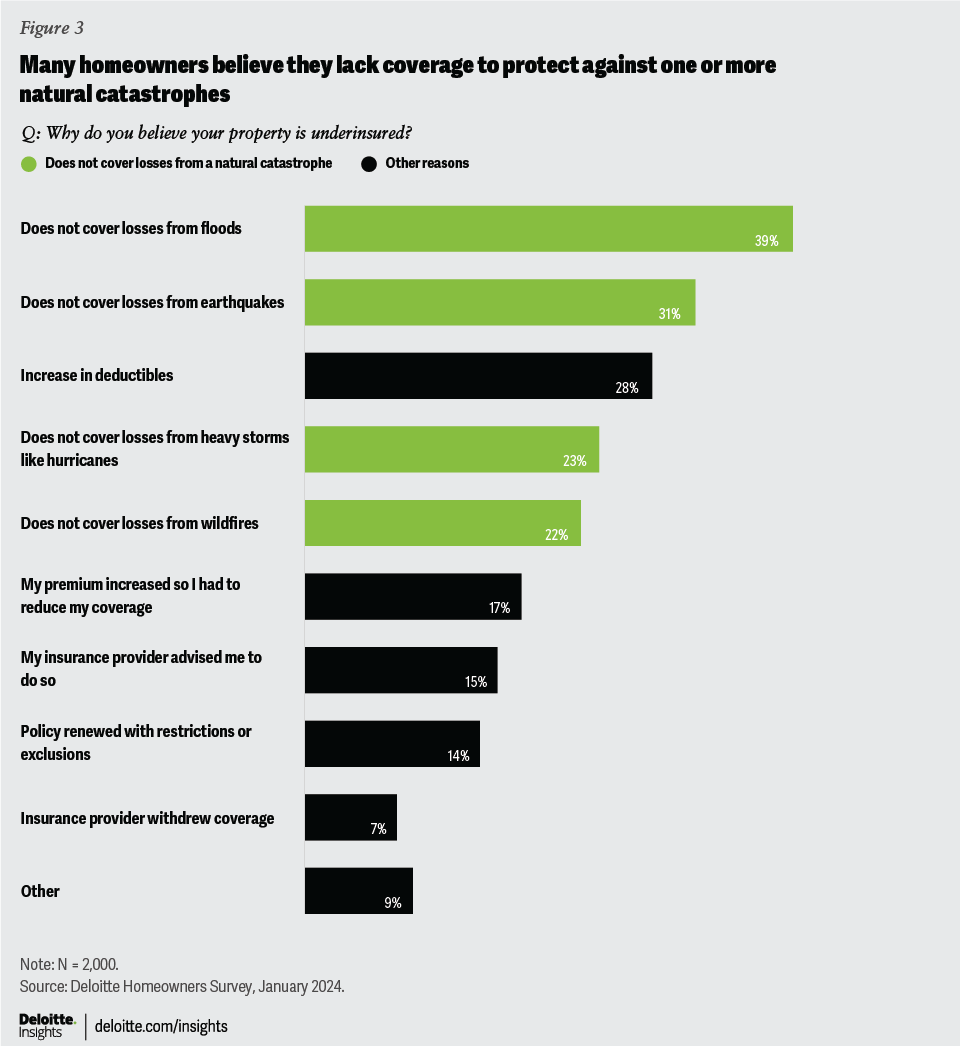

About half of those surveyed (53%) said their existing coverage options have become too expensive, forcing homeowners to seek more affordable coverage, or to go without it. Premium increases across the United States averaged 11% in 2023,8 and those residing in states like Florida that are more prone to natural catastrophes are being hit the hardest.9 According to the survey, 44% of respondents reported premium increases greater than the 11% national average. This affordability challenge is driving widespread underinsurance concerns, with most respondents left feeling more exposed to natural disasters like floods, earthquakes, storms, and wildfires (figure 3).

In the Deloitte survey, several respondents said they were surprised by unexplained premium hikes despite minimal claims history. Among respondents, only 29% had actually filed claims (to cover a loss), and about 50% of those who did were either denied or received approval for less than half of the damages filed due to coverage exclusions or insufficient limits.

{kind=link}

While respondents in all income groups said they believed they had inadequate coverage, the burden appeared particularly heavy on lower-income households (those with an annual income range of US$49,000 to US$99,000). Respondents that believe their protection gap is “substantial” or “catastrophic,” were more likely to come from lower-income households than those with an annual income of US$100,000 or higher.

Of the 25% of respondents that said they don’t plan to do anything to close the coverage gaps in their homeowner policy, the likelihood of inaction seems particularly heavy on lower-income groups, those making between US$49,000 and US$99,000 annually, where options may be limited by what respondents can afford.

Respondents are not sure how to respond to inadequate protection

Most respondents are wondering how to fully protect themselves, with 63% expressing confusion about what coverage they need and how much to purchase, leaving them at risk of being underinsured.

Most respondents (86%), for example, were not taking advantage of any state-sponsored insurance programs. The lack of participation is due to several reasons: 85% were not aware of any such programs, 10% felt the coverage amount offered was too low, and 7% thought the process was too cumbersome.10 These results reveal a complex system where the lack of awareness, misperceptions, and usability issues appear to restrict participation in potentially valuable support structures. Moreover, for those respondents that plan to increase their coverage or buy add-ons, only half of the respondents said their insurance provider advised them to buy more coverage.

Respondents are looking to shop for more coverage or a new insurance provider

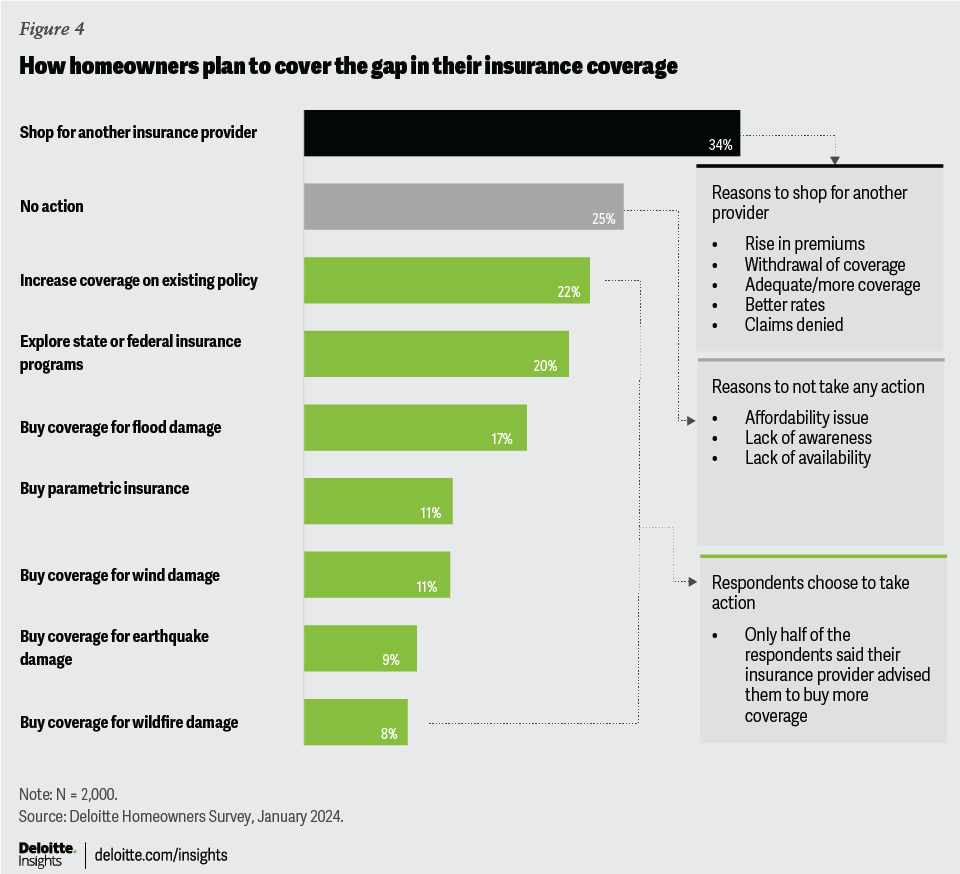

The combination of unaffordable premiums, insufficient coverage options, and inadequate knowledge has driven down many respondents’ carrier satisfaction ratings. Most respondents said they are dissatisfied with their insurance provider and about a third said they plan to shop around for more coverage or a better provider (figure 4). In fact, 22% said they already changed their insurance provider due to a combination of these factors.

{kind=link}

Recommendations for balancing profitability with social equity

Deloitte’s research demonstrates insurers’ first-line approaches for maintaining profitability through increasing premiums and restricting coverage may no longer be sustainable because it tends to fuel policyholder resentment and potentially leaves vulnerable populations exposed to risk. Instead, a shift toward collaborative solutions and proactive risk management may offer a more viable path. Insurers could, for example, explore loss-prevention and mitigation strategies that protect vulnerable communities, rebuild trust, cultivate long-term loyalty, and ensure equitable access to protection in the face of continued uncertainty in climate-related risks. Deloitte’s research identified several potential opportunities for insurers to balance profitability and social equity:

- Partner with public entities to elevate consumer awareness: More than half the respondents (59%) cited the absence of any guidance from their insurance provider on upgrading their residence to better withstand losses. This knowledge gap can create vulnerability and amplify losses.

To address it, insurers can collaborate with state regulators to develop clear, consistent messaging on existing and emerging climate-related risks that are specific to each region, as well as how to help minimize, mitigate, or eliminate exposures. Moreover, carriers can embrace innovative, engaging tools like interactive simulations, localized infographics, and targeted social media campaigns to reach diverse audiences. They can also partner with trusted community organizations, climate specialists, and hyperlocal influencers11 to build trust and help ensure that messages resonate. Several private insurers, for example, currently partner with the Federal Emergency Management Agency and the National Flood Insurance Program to promote flood preparedness and education.12

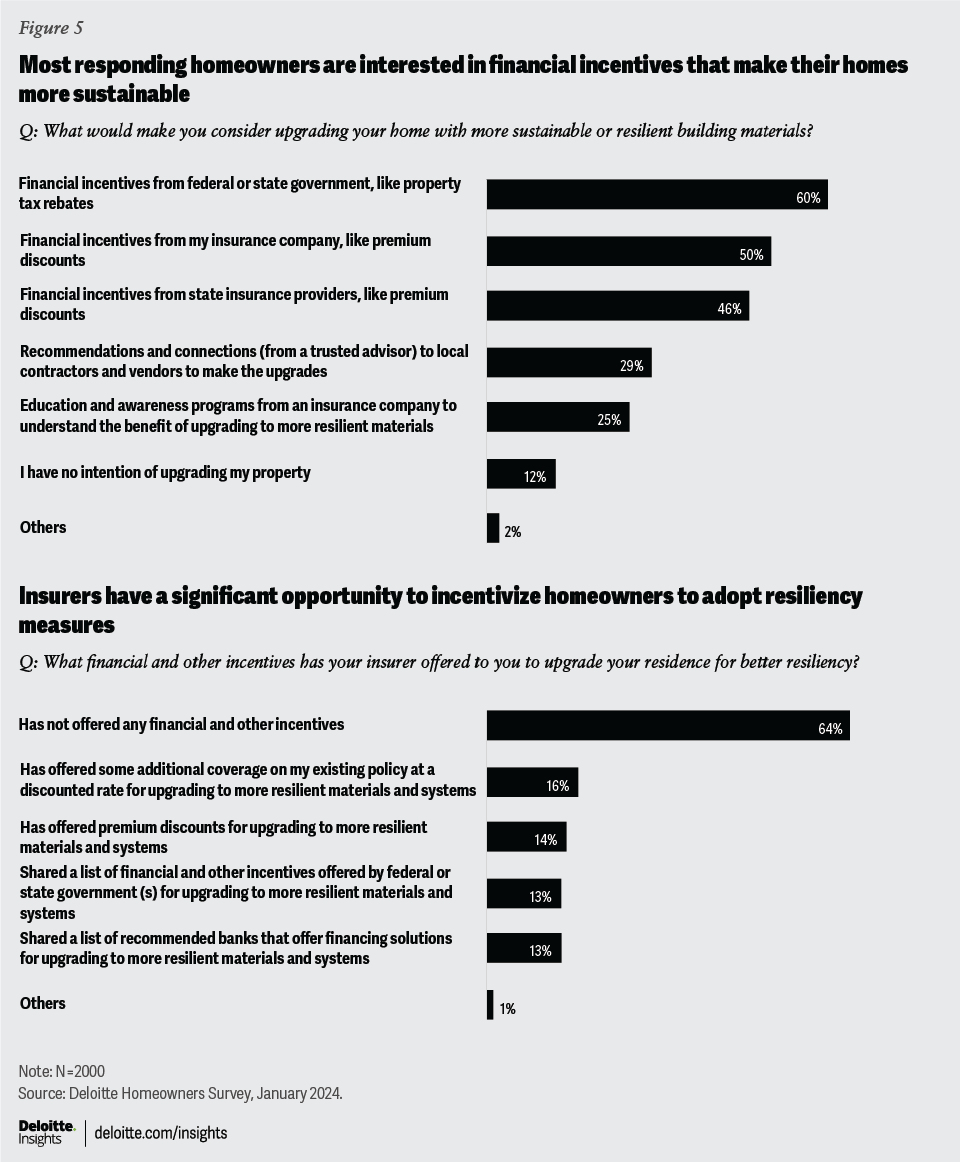

- Encourage investment in proactive risk mitigation through education and resiliency upgrades: The majority of respondents (84%) say they want carriers to educate them on weather-related risks and how to prevent or mitigate losses. This suggests a significant opportunity for insurers not only to empower homeowners to make informed decisions, but to take action to build (or reinforce) the resiliency of their homes. It would also likely go a long way in strengthening loyalty as a trusted advisor. Every dollar spent in hazard prevention measures and making building structures complaint to code can help generate a reduction in climate-related losses.13

The mismatch in consumer interest in financial incentives to upgrade their dwellings and what is being offered (figure 5) suggests a potential opportunity for carriers to incentivize homeowners to adopt resiliency measures.

{kind=link}

3. Offer rewards for sustainable practices today to help reduce premiums tomorrow: Granting rewards and discounts for adopting sustainable practices could potentially stabilize or even lower premiums for policyholders in the long term. Some private insurance carriers in Florida, for example, are offering discounts to policyholders that fortify their homes against hurricane-force winds by strengthening and securing roofs and shutters and reinforcing garage doors.14 Insurers can also work with local authorities to reward residents who meet building codes, enact flood mitigation plans, and take wildfire prevention initiatives. The state of California, for instance, offers incentives such as discounts on insurance or tax credits to homeowners who make their homes more resistant to fires, wind, rain, and hail.15 This might include establishing a buffer zone between vegetation and the home, using fire-resistant materials and designs for walls and roofs, and installing sprinkler systems. Florida also offers sales tax exemptions for impact resistant windows, doors, and garage doors. Policyholders of the Federal Government’s National Flood Insurance Program can lower their premium rates by raising their properties up, moving equipment off the bottom floor, and providing flood openings to allow floodwaters to flow from the interior to the exterior.16

4. Innovate affordable solutions that cover existing and emerging risks: Insurers could also consider providing alternative affordable solutions that cover existing and emerging risks for the underinsured homeowner segment. For example, parametric insurance, which pays out a predetermined amount based on the size of an event as opposed to the size of the losses, seems poised for growth. The global market is expected to more than double from US$12 billion in 2021 to US$29 billion by 2031,17 due in part to the fact that it tends to help make the claims process timelier and more cost-efficient, likely improving the experience for policyholders and reducing operational expenses for insurers. These premiums can be tailored to a customer’s specific budget, as well as bundled with indemnity insurance to help bridge gaps in coverage. USAA, for instance, collaborated with Parametric Solutions on a pilot program that offers parametric flood insurance to its members in flood-prone areas of Texas and Louisiana. The members who enrolled in the program gave positive feedback, indicating potential broad acceptance and paving way for wider-spread adoption within USAA.18

Insurers can also introduce bundled offerings for homeowners to cover new risks. For example, Swiss Re and Security First Insurance have entered into an agreement enabling residents to include water damage (including flood coverage) in their homeowner policy. Using Swiss Re’s proprietary model, policyholders can elect to buy added coverage with a single deductible for wind and flood at a price that accurately reflects the risk.19

Emerging technology may also help refine risk assessment models. For example, Chubb Climate+ uses artificial intelligence and advanced data analytics to identify vulnerable households and the likely damage.20 By using advanced technology to detect underlying structural or geographic issues, insurers can educate and incentivize consumers to implement risk management measures earlier in the process and potentially drive down both claims and premiums.

Building a resilient and sustainable future is a shared responsibility

Balancing profitability and social equity isn’t a zero-sum game. By investing in resilience, offering diverse solutions, and fostering trust and transparency, insurers can help fill the void caused by the wake of retreating carriers and affordability challenges for the most vulnerable markets. However, the insurance industry cannot achieve this alone. It will likely require collaboration and pragmatic partnerships between public and private enterprises, including professionals in building and technology disciplines. The insurance industry appears uniquely positioned to champion these solutions and act as a convener, bringing all stakeholders to the table. Illuminating, encouraging, and incentivizing long-term resilience and more refined risk management models can potentially create a more sustainable and profitable market despite the increasing threat of severe weather events.

Survey methodology

To gain insights into the factors that contribute to these coverage gaps and to identify solutions that could promote resiliency in the residential insurance landscape, the Deloitte Center for Financial Services surveyed 2,000 US homeowners from 21 states that are at a high risk of climate-related disasters.21 The survey was fielded in January 2024 and targeted respondents who believed their homeowners insurance coverage was inadequate. The sample reflected a demographically diverse respondent pool across age and income groups. There was representation from age groups in the 18 to 34 years (14%), 35 to 44 years (26%), 45 to 54 years (20%), 55 to 64 years (19%), and 65 years and above (20%). In terms of income brackets, we surveyed respondents with annual income of less than US$49,000 (21%), US$50,000 to US$74,999 (24%), US$75,000 to US$99,999 (16%), US$100,000 to US$249,999 (34%), and US$250,000 or more (5%).

BY

Kelly Cusick

David Sherwood

Namrata Sharma

The authors would like to thank Courtney Davis, Principal, Risk and Financial Advisory and Elizabeth Payes, Senior Editor, Deloitte Insights for their contribution toward this article. Additionally, we would like to thank David Levin, DSAS Manager, for providing survey advisory support and Rajesh Medisetti, DSAS senior analyst, for providing tableau analysis of the survey data.

Cover image by: Natalie Pfaff

Visit the Deloitte Center for Financial Services

Access more insights for the banking and capital markets, commercial real estate, insurance, and investment management sectors.