The sustainability imperative for M&A

Why sustainability is now a cornerstone of the M&A Agenda to protect and create value

{kind=link}

Determining the impact of environmental, social, and governance (ESG) considerations across a company’s value chain is becoming central to how many companies craft their overall business strategy.

Companies are under pressure from increasing regulation, stronger investor and NGO activism and shifting consumer demands. The bar has been raised: executing on an ambitious ESG strategy is now core to protecting a company’s “licence to operate”.

Companies that make rapid ESG progress are seeing increases in their valuation and their business opportunities:

- A simple correlation analysis from 2022 showed over 2x higher EV/EBITDA multiples for consumer companies with the best ESG scores compared to those with the lowest scores

- More sustainable, inclusive and less carbon intensive economic models also open up new business opportunities. This drives growth and helps attract high calibre talent, motivated by purpose led work.

In today’s business environment, attracting external investment, whether from banks, private equity or via an IPO, requires not only a myriad of non financial disclosures but also an ambitious ESG strategy and clear evidence of implementation and delivery. Institutional investors are prioritising companies that are transitioning to more sustainable business models, products, and services not only because they feel they must but also because they see long term value creation potential.

M&A should be a central part of the corporate arsenal as a means to manage a company’s sustainable corporate strategy. It can help execute on the value ambition by:

- securing innovative business models to accelerate the decarbonisation of value chains, in particular of companies operating in hard to abate sectors; and

- accessing technological solutions to tackle social challenges, in particular for companies sourcing from conflict affected and high risk areas (CAHRAs).

We observe three main trends for Sustainability M&A

Protect your “Licence to Operate”

ESG is seen as a strategic imperative as companies are increasingly concerned that risks arising from the value chains of acquired companies will threaten their "licence to operate".

The general pressure to combat climate change requires companies not just to commit but act on their environmental impact. However, material acquisitions can significantly dilute the progress an acquiring company has made. The resulting failure to meet publicly made environmental commitments (such as achieving 100% recyclable or reusable packaging by 2025), can lead to reputational damage with customers and investors, harming the brand, company and management team.

Besides the environmental dimension, companies are also protecting their “social licence ”. Child labour, precarious working conditions or the use of bribery, in the supply chain of an acquired company can trigger material reputational damage and financial risk. This is particularly relevant for sectors sourcing from CAHRAs. Examples include rare earths and minerals used in EV batteries, and precious metals and stones used in jewellery.

Increase transparency on the financial impact

What distinguishes ESG risks significantly from most other risk categories that companies have managed in the past is the unclear financial impact of ESG initiatives and risks. Serial acquirers are asking us:

- How can future profitability levels be grown or at least maintained in a new, less carbon intensive and more socially sustainable business model?

- What is the impact of climate risks on the value of acquired assets? Is there a potential risk for material impairments or even stranded assets in the future?

Creating transparency as part of ESG due diligence will identify material financial exposure. Relevant diligence questions include:

- What is the EBITDA impact from a more sustainable sourcing or packaging strategy, e.g. switching to “green” steel or to fully recyclable containers?

- What one-off cost or Capex will be required to align the target to less carbon-intensive operations of the buyer (e.g. by replacing inefficient equipment)?

- What financial exposure will there be for the target related to climate change risks (e.g. the impact of flooded manufacturing facilities)?

- What are sustainability synergies, e.g. proven solutions for waste reduction?

- How ready is the target to meet mandatory non-financial disclosure requirements e.g. EU Taxonomy) What one-off and running costs have to be added?

Shift to more innovative business models

The shift to more sustainable economic models opens up new business opportunities. This drives growth and gives companies an edge hiring high calibre talent attracted by the appeal of work aligned to their values. It gives companies the opportunity to reposition their offering and helps to future proof revenues by:

- Thriving in existing markets: a focus on sustainability can spur innovation through sustainable and therefore differentiated products that enable price premiums, capture market share, and drive operational efficiencies.

- Unlocking new markets: sustainability provides an opportunity to increase the total number of addressable markets and capture above average growth for the industry by moving into new markets.

In addition, private equity investment continues to flow into businesses that are focusing on sustainability, either directly or via private equity backed corporates consolidating a sector and expanding their skillset or service offering. This trend is expected to continue, with innovation leading to an increasing number of emerging ESG focused sub sectors that offer strong growth opportunities. Examples include innovations related to the energy storage and generation, electric vehicle related, waste to value/energy and recycling, future of food as well as platforms for ESG data management and transparency/traceability.

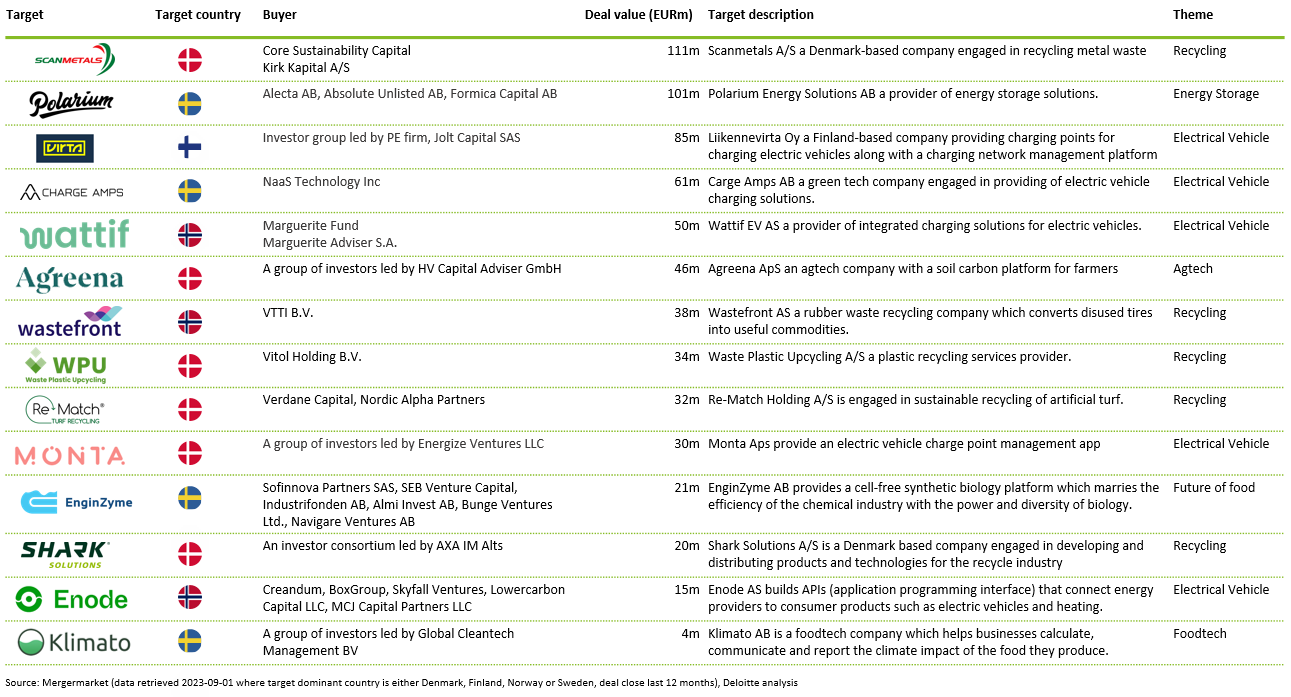

Nordic ESG deals with innovation at its core

In recent years, the Nordic ESG landscape has witnessed a notable surge in M&A activity involving companies with innovative business ideas that extend beyond conventionally associated ESG areas such as renewable energy. While renewable energy remains a significant part of the ESG equation, Nordic M&A highlights a spectrum of innovative business models and industries that are actively contributing to ESG objectives. From recycling companies pioneering the transformation of waste into valuable resources to technology firms revolutionising EV infrastructure, agritech companies fostering sustainable farming practices, and food tech companies helping businesses calculate the climate impact of the food they produce – the ESG investment landscape showcases the diversity and innovativeness of Nordic businesses.

Two exemplary acquisitions within the above-mentioned industries are the acquisition of Virta (Liikennevirta Oy), a Finnish provider of EV charging stations and E-mobility software, and the acquisition of the Danish agritech company Agreena. These deals underscore the dynamic nature of ESG investments, demonstrating that software investments and sustainable investments in innovative solutions can be combined (for more examples of interesting recent ESG deals in the Nordics, see the linked table). As the Nordic region continues to embrace a diverse range of ESG-focused ventures, it becomes increasingly clear that the ESG landscape is not only evolving but also thriving, with innovation at its core.

Case study

Buy-side ESG due diligence

A client, within the consumer goods industry, approached Deloitte regarding assessing a target company from a sustainability perspective. Emissions, packaging and supply chain are three ESG areas that are of the foremost importance for the client when reducing their carbon footprint, becoming more sustainable for their customers, and increase enterprise value for the group as a whole.

At Deloitte, we assessed the target company through a ‘double materiality approach’. In the approach, several ESG areas such as the earlier mentioned areas in addition to e.g. energy management, business ethics and product safety and quality were analysed. How the ESG areas were handled by the target company and the potential impact on customers, enterprise value and the acquirer’s stakeholders were assessed.

Each ESG area was examined across four dimensions:

- Materiality: which investments to emphasize given the business model, mapping of stakeholders and potential impact on value chain based on identified ESG risks and opportunities

- Maturity: what activities and level of effort the company is undertaking

- Bridging: how much effort is required to bring the organisation to desired maturity level

- Risk and opportunities: what is the “net risk”, considering materiality, maturity and activities to close gaps

During our assessment we identified several development areas for the target company which affected the purchase price of the company. In addition, we suggested sustainable strategies and solutions to drive further enterprise value in relation to ESG areas such as the supply chain, packaging and energy management, which in turn also generated potential cost benefits.

Martin Eriksson