The next wave of innovation

Technology and value-based care are transforming medtech R&D

The medtech industry is under pressure: From tight margins and the shift to value-based payment models to advances in digital technology, many R&D leaders are taking a fresh look at investment strategies.

Executive summary

MOST medtech companies are under pressure to improve efficiency and reduce costs in an environment where health systems, patients and payers require increasing levels of evidence to justify product value and reimbursement. At the same time, innovation in payment models and advances in sensors and digital technologies are creating new opportunities to advance patient care and improve development efficiency. Technology advances can also create competitive threats from nontraditional entrants.

The Deloitte Center for Health Solutions and AdvaMed surveyed 22 medtech companies to understand how medtech R&D leaders are responding to these trends.

The key findings from the survey are:

- R&D leaders are responding to the need to drive innovation, improve margins and reduce cost by focussing on the following priorities over the next three to five years: diversification of portfolios (86 per cent), accelerating time to market (82 per cent) and leveraging real-world evidence (RWE) in product development (77 per cent).

- Ninety-five per cent of respondents cited increasing complexity of global regulatory requirements as a top challenge for R&D leaders over the next three to five years. This is notable, as medtech companies are increasingly seeking regulatory approval for products and services in multiple jurisdictions.

- New payment models are changing the innovation focus for 68 per cent of companies. They are developing products, services and software that can help providers improve outcomes, reduce cost, decrease posttreatment complications and increase procedural efficiency.

- Digital technology is opening opportunities as well as creating challenges. While 100 per cent of the companies surveyed reported investing in device connectivity, 77 per cent report that integration of data from new technologies is a key challenge. Many companies also find it a challenge to address critical funding and skill gaps, as software constitutes an increasing proportion of product innovation.

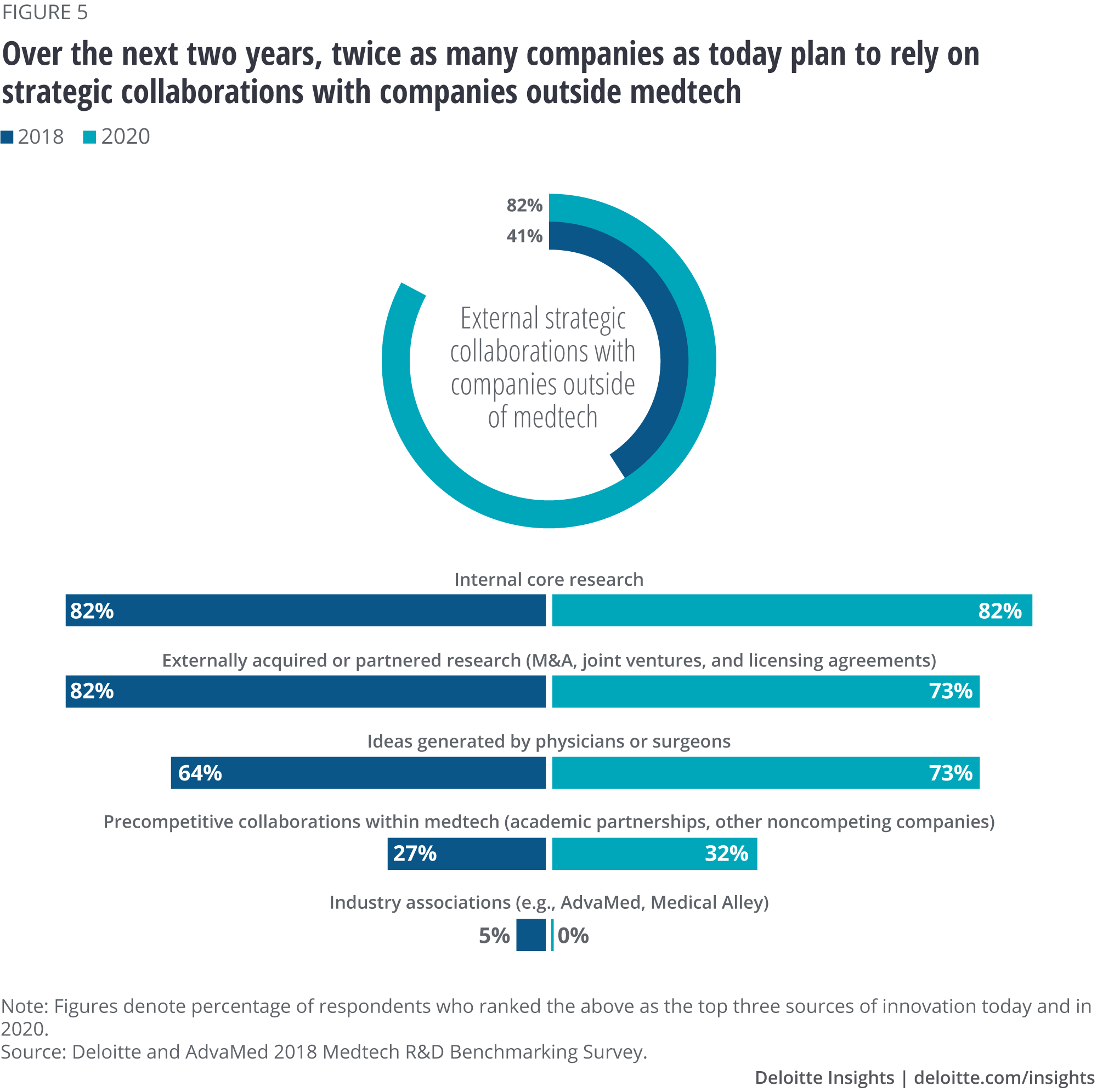

- Companies are looking to nontraditional partners to help drive innovation agendas. In the next two years, 82 per cent of the companies surveyed plan to collaborate with organisations outside of medtech (for example, technology and health care companies), almost double the percentage today (42 per cent).

- Seventy-three per cent of the companies surveyed are adopting hybrid operating models, which leverage a combination of centralised and decentralised resources to enable both business unit autonomy and synergies across business units for new capabilities such as advanced technology or digital.

As a result of these trends, R&D leaders should consider the following strategic questions: Is adequate investment going towards diversifying the portfolio and driving software development while still sustaining the core? What types of evidence will customers demand to adopt new solutions, software and services? Does R&D have access to the right capabilities and talent to drive the development of software-based solutions? Are the right governance and partnership models in place to cultivate relationships with nontraditional partners? Is R&D organised effectively to balance efficiency, autonomy and scalability of new capabilities (for example, software development and analytics)?

Introduction

In recent years, the medtech industry has seen increasing price pressures from payers and providers as a result of the shift from volume to value, a changing global regulatory environment, and the rise of new and nontraditional competitors. Pressures to reduce health care costs and changing purchasing dynamics are compressing medtech company margins. Between 2008 and 2016, the return on capital employed (ROCE) for medical device companies almost halved (from 14 per cent to 6 per cent), as compared to biopharma companies (16 per cent in 2016).1 For R&D leaders at medtech companies, these shifts have created an existential challenge that will likely require a new way of thinking, operating and doing business.

Rapid advances in technology are creating new opportunities as well as posing new competitive threats to medtech companies. In a shift from their core competencies, many medtech companies are incorporating sensors and software into devices and diagnostics to generate, gather and transmit or share data. This means companies will likely need to invest in technology, talent, partnership models, and processes to collaborate and compete with nontraditional competitors.

Survey methodology

The Deloitte Center for Health Solutions and AdvaMed surveyed 22 respondents, mainly from mid-size (US$2–10 billion capitalisation) and large medtech (>US$10 billion capitalisation) companies between April and August 2018. Survey respondents included leaders from R&D and innovation functions of medical device, diagnostics and imaging companies.

The survey was aimed at understanding the impact of various market and regulatory changes on medtech R&D strategies and operating models. The survey included questions on R&D investments, sources of innovation, regulatory impacts, and other priorities and challenges.

What the findings tell us

Companies are likely to focus on portfolio optimisation, driving efficiency and using new data sources

R&D leaders are responding to the need to drive innovation, improve margins and reduce cost by focussing on the following priorities over the next three to five years: diversification of portfolios (86 per cent), accelerating time to market (82 per cent) and leveraging RWE in product development (77 per cent). In addition, many (64 per cent) of the companies are looking to develop more digitally enabled solutions and software (figure 1).

To build differentiated products, many companies are shifting R&D investments away from core products and queue extensions towards transformational innovation: innovation that creates and delivers customer value through novel products, solutions and business models that address unmet market needs. The survey shows that companies expect to increase the proportion of R&D budgets they spend on transformational innovation by 5 percentage points in the next two years (figure 2). This shift is likely to result in higher-margin offerings and an increased return on investment. A Deloitte analysis shows that medtech companies focusing on breakthrough product innovation, especially in new or underdeveloped markets, have a higher return on capital than peers.2

This change in R&D spending, however, reflects a shift in R&D dollars, rather than an increase. Almost 70 per cent of respondents said their R&D spending currently ranges from 5–15 per cent of income and 82 per cent anticipate spending to remain in the same range in the future. With relatively flat R&D budgets, companies may have to make tough choices on investing in transformational innovation and digital technologies, sustaining core products and not developing some products. At the same time, many companies are likely to invest in transformational programmes to help identify areas of cost savings and opportunities to accelerate products to market as a way to free up R&D funds.

This shift towards transformational innovation, including the development of solutions and services, might explain the prioritisation of RWE. Real-world data such as data collected from existing devices, claims data, or electronic medical records could help identify unmet needs that innovative solutions might be able to address. Medtech companies could, for example, understand patterns of noncompliance to a therapeutic device from reviewing this data and develop a service that addresses identified issues. RWE could also be valuable in developing evidence to support product value-propositions and the case for reimbursement.

Successfully launching new products and solutions in multiple jurisdictions is not straightforward: Ninety-five per cent of respondents cited increasing complexity of global regulatory requirements as a top challenge over the next three to five years. Further, 64 per cent of surveyed companies also noted that the number and complexity of global regulations influence new product development decisions. For example, the European Medical Device Regulation (MDR) will require companies to review their portfolios and ensure all products are in compliance with any updates to the regulations. Companies that fail to comply risk losing their licences to market in the region.3 R&D teams should develop skills in understanding and addressing global requirements early in the development process.

Developing software-based solutions means that R&D teams should keep pace with an accelerated rate of innovation and be well-versed in evolving software, cybersecurity and patient privacy regulations. R&D teams should embed cybersecurity early in the software development process. Regulators are advancing approaches and guidance to help companies understand and comply with requirements (see sidebar, “Keeping pace with technological advances at FDA”).

Keeping pace with technological advances at the FDA

Over the last five years, the US Food and Drug Administration (FDA) has clarified its regulatory approach for new and innovative digital devices, including software as a medical device (SaMD). In 2017, the FDA released its digital health innovation action plan which highlighted its numerous efforts. For example and as required under the MDUFA IV Commitment Letter, the plan described that FDA would hire new staff with expertise in software, cybersecurity and digital health. Furthermore, it announced the software precertification pilot programme (Pre-Cert pilot programme), which aims to develop a new approach for a risk-based and accelerated review of digital health products by “looking first at the software developer or digital health technology developer, not the product.”4 Lastly, it released three new guidance documents that clarify regulatory approaches for certain digital health products.

In addition, due to an increased understanding of medical device cybersecurity threats, the FDA and other federal government agencies have taken a renewed interest in this topic and have engaged the assistance of medical device manufacturers and other stakeholders within the health care community. For example, in October 2018, the FDA released a revised draught guidance on premarket considerations and requirements for medical device cybersecurity controls. The guidance refines FDA’s expectations related to the cybersecurity considerations a manufacturer must document during the design and development of a medical device.

New payment models are influencing the wave of innovation

Sixty-eight per cent of surveyed companies are shifting their focus on innovation due to payment model and care delivery reforms. New payment models can give hospitals and physicians incentives to deliver better care while reducing the total cost of care. Many medtech companies are developing service-oriented solutions that help health care providers meet these goals. Surveyed companies are focussing on helping providers improve outcomes, reduce costs, decrease posttreatment complications and increase procedural efficiency (figure 3).

Case study: Designing solutions to drive value across the episode of care5

Zimmer Biomet offers patient engagement, clinical and telerehabilitation services to help improve outcomes for orthopaedic episodes of care. Interactive patient engagement tools educate patients about treatment options, facilitate physician-patient communication and collect patient-reported outcomes data. Consultation services, combined with a data-mining and analytics platform, help hospitals improve overall productivity and surgical efficiency by streamlining clinical workflow. Telerehabilitation tools enable personalised, clinician-supported postsurgical physical therapy at patients’ homes.

Through these services, the company aims to improve patient outcomes, reduce costs and make the care process for orthopaedic patients more efficient.

Ninety-three per cent of surveyed companies are developing a combination of products, services and software. These solutions can increase patient engagement, minimise provider operational inefficiencies, as well as track and analyse patient-reported outcomes for reimbursement. Medtech companies should engage with customers early to understand what evidence they will demand to adopt new services or solutions.

Beyond developing new products and services, 64 per cent of surveyed companies reported either discussing, piloting, or implementing value-based contracts with payers or providers. A growing number of value-based contracts tie payment more closely to device performance and patient outcomes. For example, Medtronic entered into an agreement with a large payer that links payment to the success of its automated insulin pump in lowering HbA1c (glycated haemoglobin) levels in patients (see the sidebar, “Case study: Medtronic partners with health plan to focus on outcomes”).7 These new contracts will likely spur organisations to generate RWE from sensors, devices and health IT systems, and use analytics to gain insights from the outcomes data.

Case study: Medtronic partners with health plan to focus on outcomes6

Medtronic partnered with a health plan on a new model for patients with Type 1 and 2 diabetes, transitioning them from multiple injections to a Medtronic insulin pump. Patients have access to Medtronic’s closed-loop system, which automatically delivers insulin to keep their blood sugar levels in range. It also ties a portion of Medtronic’s payment to meeting clinical improvement thresholds for these patients.

Companies are investing in digital capabilities to lay the foundation for innovation

All companies surveyed reported investing in device connectivity. Device connectivity requires capabilities in software development that enable data exchange, encryption and interoperability. Seventy-three per cent of medtech companies expect R&D spending on software development to be more than 10 per cent of budgets by 2020, as compared to only half of companies currently. Though an improvement, is this level of investment enough to move the needle in terms of capability? Only one surveyed company expects spending on software development to be over 40 per cent of the R&D budget in 2020. With relatively flat R&D budgets, this could mean a shift away from the development of traditional devices towards connected and digital solutions.

Case study: Connected devices to improve cardiac care outcomes8

In 2017, Boston Scientific launched its Resonate™ family of implantable cardiovascular defibrillators (ICD) and cardiac resynchronisation therapy defibrillators (CRT-D). These systems include the HeartLogic™ Heart Failure Diagnostic to help physicians improve heart failure management. The diagnostic tool alerts physicians of worsening heart failure by combining data from sensors evaluating heart sounds, respiration rate and volume, thoracic impedance, and night heart rate and activity. The HeartLogic Heart Failure Diagnostic will send alerts directly to a physician’s LATITUDE™ NXT remote patient management system to enable timely intervention and potentially improve patient outcomes.

Vast amounts of real-world data, including data from connected devices, could be used to understand the patient journey, consumer preferences, and unmet needs and to improve products and services. However, data integration and analysis are not small tasks. While 64 per cent of companies are prioritising developing more digitally enabled solutions, 77 per cent cite integration of data from new technologies as a key challenge. Successful data integration could include both understanding customer needs through the analysis of real-world data and the integration of data generated from connected devices into the clinical workflow to make information actionable.

Some companies (64 per cent) are starting to collect, analyse and use data to improve their products or provide additional services (figure 4). Today, many companies are only scratching the surface in terms of how they can apply data, likely using it to inform patient decision-making or to make minor software updates. But there is a long way to go before they could achieve a closed-loop R&D model where data from products will be fed back into the R&D process and inform future product development.

Beyond enabling product enhancement or new service offerings, digital capabilities can help improve R&D productivity. Specific opportunities include digitising and rationalising processes, reducing cycle time (a key priority for most surveyed companies) and generating cost savings. Robotic cognitive automation, for example, can help execute repetitive tasks more efficiently and allow workers to focus on high-level tasks. Fifty-five per cent of surveyed companies plan to develop automated protocols to accelerate clinical trials in the future, as compared to 14 per cent today.

To remain competitive, medtech companies should develop digital competencies and skills—in R&D and beyond. Seventy-three per cent of surveyed companies cite talent gaps, specifically around software and cognitive technologies, to be one of the top three constraints to R&D productivity. Top talent priorities include software development (82 per cent), device connectivity (82 per cent) and analytics (77 per cent). This shift in talent priorities is not unique to R&D. Building and delivering end-to-end solutions requires collaboration across the company. For example, regulatory and commercial functions will likely also need to become data-savvy to seek regulatory approval and gain market traction for new solutions. Accessing digital talent will likely require more resourceful recruitment and retention strategies, including looking externally for collaborations and partnerships with a diverse range of existing and emerging players, especially academia, data-first tech companies and innovative new startups.9

Surveyed medtech companies will look outside of the sector for strategic partners

Traditionally, medtech has relied on internal research and external acquisitions to build and replenish product portfolios and pipelines. In the next two years, surveyed companies report that while they will continue to rely on internal core research, they will also significantly increase the priority of strategic collaborations with companies outside of medtech. In fact, twice as many companies (82 per cent) plan to seek out collaborations outside of medtech than those that do so today (41 per cent) (figure 5).

Collaborations and partnerships with companies outside of medtech can offer access to the digital skill sets required for innovation. While medtech companies have already built sophisticated sensors and connected devices, many have just begun experimenting with artificial intelligence (AI) capabilities, for example. Technology companies could provide the technical capabilities required to improve device efficiency, data management and insight generation (see the sidebar, “Case study: Leveraging AI to improve diagnostic capabilities”). Moreover, medtech companies can also tap into the rich customer engagement experience of consumer tech organisations such as Google as they become more consumer-oriented.

While companies are increasingly looking outside of medtech for collaborations, survey respondents reported that only 7 per cent of R&D projects are being done in partnership with non-medtech companies today. This may be because these partnerships are in their early stages, supported by small budgets, or that companies are leveraging them for non-project-specific capabilities. Some companies may simply be experimenting with new collaborations or technologies but have not yet committed resources to execute projects beyond the pilot stage. In addition, some might not have yet figured out how to address new risks these partnerships pose.

Successful collaborations with companies outside of medtech may require new ways of working. Specifically, companies may want to consider centralising relationships through teams focussed on digital innovation. These teams tend to have the resources to invest in long-term strategies and are not constrained by meeting the business units’ short-term goals. These teams should also consider intellectual property protection, income-sharing models and management of parallel product development processes. An increasing network of collaborations may require companies to establish new governance models.

At the same time, the entry of nontraditional players such as consumer electronics into the regulated device arena could present a competitive threat. This implies that the complexity of these collaborations will likely increase, as they will require incremental controls to ensure that intellectual property and other confidential information is safeguarded.

Case study: Leveraging AI to improve diagnostic capabilities10

To boost image-processing power, GE Healthcare has partnered with NVIDIA to bring AI technology to its 500,000 imaging devices globally, including the Revolution Frontier computed tomography (CT) system and ultrasound imaging devices, such as the Vivid™ E95 and LOGIQ™ E10. This AI technology accelerates reconstruction and visualisation of blood flow and improves 2D and 4D imaging for select imaging solutions. The technology also enables deep learning algorithm applications for analytics, which is integrated into clinical and operational workflows and equipment.

These solutions help to improve imaging capabilities, liver and kidney lesion detection and characterisation, and to reduce non-interoperable scans and unnecessary follow-ups.

Medtech companies are increasingly adopting hybrid operating models

Seventy-three per cent of respondents reported that they have adopted a hybrid operating model, leveraging a combination of centralised and decentralised resources, up from 59 per cent in 2015 (figure 6). In a centralised model, resources and strategic decisions are managed at the corporate level. In a decentralised model, both resources and decision-making are managed at the business unit or functional level. Hybrid models allow companies to segregate capabilities between corporate and business units, allowing more control over core and noncore functions. For example, under a hybrid model, companies can have R&D experts in the business units and share across the company services such as business development and engineering support.

The popularity of hybrid models may reflect a desire to balance control with cross-business-unit collaboration. Survey respondents described the advantages of hybrid models over the centralised or decentralised approach:

- Execution at the business-unit level

- Enable faster decision-making and execution of business strategy;

- Drive customer and patient engagement; and

- Enable collaboration with external entities that bring complementary expertise, as well as other divisions of the same company.

- Centralisation of core competencies at the corporate level

- Drive synergies via centres of excellence (for example, advanced technology and digital transformation);

- Centralise strategic investment in disruptive or white space opportunities; and

- Present a cohesive message to the external market.

The financial reality of each organisation will ultimately influence the selection of an operating model. The constant need to accelerate innovation, combined with a growing cost base, is expected to continue pushing many medtech organisations to look for ways to reduce costs to reinvest in R&D. Generating economies of scale through integration or M&A will likely continue to be a lever. In addition to typically integrated functions such as IT, accounting and HR services, companies should look at more strategic choices such as optimising the product portfolio or the manufacturing network to drive additional efficiencies and fuel more differentiated innovation.

Next steps

Growing competitive pressures, combined with the constant emergence of new technologies, will likely require medtech companies to be flexible and constantly adapt to the changing health care ecosystem. For R&D leaders, this means transforming how they think about allocating R&D investment, sourcing and organising new capabilities and hiring and retaining talent. At the same time, one size will not fit all: Companies should evaluate business segments to determine where they are likely to realise the most value from transformation and prioritise initiatives accordingly.

Allocating R&D investment. While companies are shifting a greater proportion of R&D funds towards transformational innovation and software development, is it enough to stave off competitive threats from nontraditional players? Companies should rebalance portfolios, shifting investment away from developing products with limited profitability towards those with higher growth potential. They should also consider approaches to reduce R&D cost, maximise value from limited digital investment and start building for the long term.

Transformational initiatives could help reduce R&D cost and accelerate products to market. For example, lean and agile approaches could enable faster learning cycles to optimise products. New technology such as robotic process automation could help reduce unnecessary manual intervention and increase value-added activities, which in turn could help improve product quality.

In addition, innovation will require investment in the generation of compelling clinical evidence to support adoption and reimbursement. Companies should consider making long-term investments to establish technology platforms to be able to access, integrate and analyse real-world data. RWE could help to not only develop new products and solutions, but also support the case for reimbursement.

Balancing the operating model. Medtech companies are likely to continue to look towards hybrid operating models for the right balance of autonomy and efficiency. Integration of some capabilities at the corporate level may offer opportunities to scale and reduce costs while allowing business unit autonomy in other areas.

R&D teams are likely to increasingly rely on critical capabilities such as software development and data analytics. Focusing these capabilities in centres of excellence may allow teams to maximise on limited resources. Digitally focussed innovation teams, for example, can align investments with long-term vision, establish partnerships to secure needed capabilities and maximise learning. These teams can partner with the business units to embed new capabilities. Many companies are moving towards centralising software and analytics capabilities via centres of excellence and scaling them across business units.

Talent strategy. R&D leaders should formulate talent strategies to simultaneously develop and acquire critical skill sets such as digital product development and hardware/software integration. Companies may need to look outside of medtech to acquire some skill sets, but also develop robust onboarding programmes to help ensure the talent is successfully integrated into the organisation. The integration of software and analytics with core medical device and regulatory expertise will likely be critical for accelerating innovation. Companies are likely to compete with other industries for top talent and should ask themselves what they can do to attract the best technical skills.

Optimising the performance of R&D is a complex task that requires a deep understanding of the multiple interdependencies this critical function drives. Defining a clear transformative strategy combined with a commitment to efficient execution can be key for driving growth while supporting ongoing business needs. R&D leaders should continue to evolve throughout this journey and seize the opportunity to shape the future of the enterprise.

Life Sciences R&D

Clinical innovation remains imperative amid increasing pricing pressures, growing market share for generic pharmaceuticals and biosimilars, looming patent cliffs and heightened scrutiny by regulators. With many new avenues enabled by the 21st Century Cures Act, real-world evidence, translational medicine, big data analytics and digital technologies, new opportunities abound—if strategically harnessed—to enhance the patient experience and improve research and development efficiencies and returns.

{kind=link}