Virtual health accelerated

How can health care organisations take advantage of the current momentum?

The COVID-19 pandemic led to an accelerated adoption of virtual health. But will that momentum continue to build? Here’s how health systems could use the growing acceptance of virtual health to transform delivery models.

Executive summary

The COVID-19 pandemic triggered a dramatic adoption of virtual health. During the early weeks of the pandemic, virtual visits (i.e., video- or phone-based visits) increased by more than 11,000% over prepandemic levels, according to the Centers for Medicare and Medicaid Services (CMS).1 But will adoption of virtual health continue to accelerate once the threat of the pandemic subsides?

In late 2020, the Deloitte Center for Health Solutions surveyed clinical leaders from 50 health systems—and held a virtual roundtable with physician leaders—to explore the possible implications of continued virtual health adoption, and examine the potential opportunities that could unfold during the next one to three years. We examined how the last several months have changed the practice of medicine, how consumers and clinicians are likely to use virtual health in the future, and how care delivery models might be transformed.

Findings from our survey showed:

- One in two clinical leaders said the pandemic had led to significant shifts in their health system’s virtual health strategy. Continued investments into virtual health, along with an enterprisewide strategy, were the top strategic initiatives cited. Automating decision-making around virtual health was mentioned as another important consideration.

- Across care settings, clinical leaders anticipate that the optimal level and mix of virtual visits will be very close to the peak they witnessed during the pandemic. For primary care and chronic care management, that means one-third of all visits would be virtual, up from only 5% prepandemic.

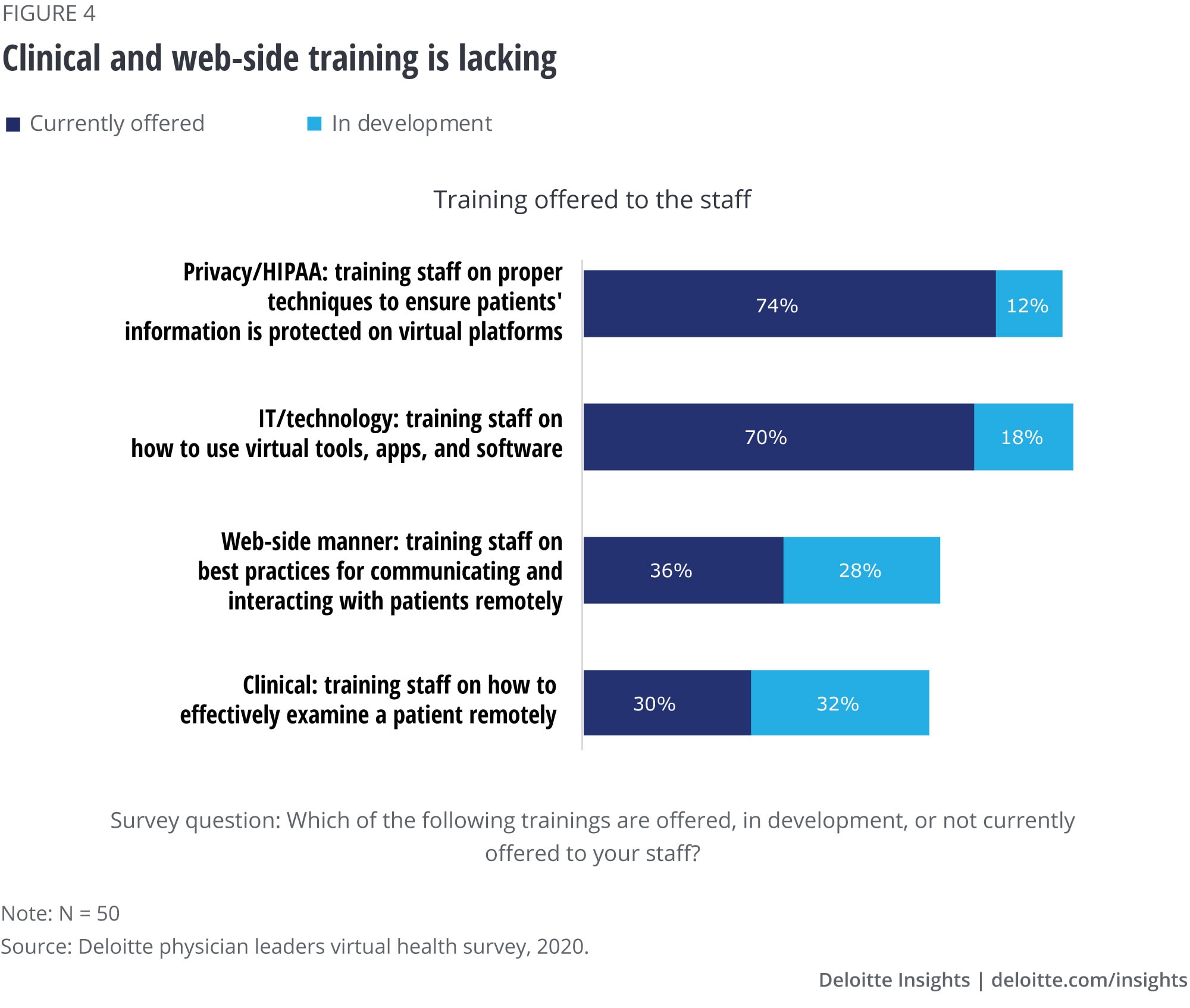

- Two in three clinical leaders said they currently provide staff with technology and privacy training. However, clinical and “web-side manner”2 training is less common.

- Most clinical leaders said they were tracking patient experience and utilisation metrics related to virtual health. Quality of care and team experience measurements are lagging.

- Clinical leaders said they have been able to overcome consumers’ and physicians’ reluctance to adopt virtual health. However, interoperability, integration of platforms, and data vulnerabilities continue to be a challenge.

Virtual health gains could be a silver lining of the pandemic. During the early response phase of the COVID-19 crisis, many health systems and physician practices rapidly implemented processes around virtual health. As a result, the health care sector is probably about five years closer to the Future of Health TM that Deloitte anticipates will take place between now and 2040. As health systems continue to recover from the pandemic, and ultimately thrive3 in the coming months and years, they should work to thoughtfully scale up new learnings and transition to a longer-term, enterprisewide approach. To realise the full benefits of virtual health, this should include:

- Evolving team-based care to advance the integration of behavioural health, primary care, and specialty care, and help family caregivers become more involved in care

- Thinking beyond process measures to develop more meaningful measures of care quality and care-team experience

- Training clinicians and support staff to ensure patients get the same quality care experience as patients who have face-to-face visits

Health care stakeholders probably won’t realise the full value of virtual health if it becomes just another component of the traditional health care delivery process. The pandemic has created a new sense of urgency to advance value-based care, adopt radical interoperability, launch new care delivery models that consider the provider experience, and apply a consumer-centric lens to the health care system.

Methodology

In fall 2020, the Deloitte Center for Health Solutions held a virtual roundtable with physician executives and surveyed clinical leaders from 50 large health systems (76% with annual revenue above US$1 billion).

Our survey sample consisted of chief medical officers (52%), vice presidents, department chiefs, and other clinical services leaders. Their organisations spanned academic medical centers, university-based and community-based hospitals, multistate health systems, children’s hospitals, and physician-owned hospitals.

“There were some myths of what telemedicine could do … and providers and patients were surprised by how effective the clinical visit could be [in a virtual setting]. We are hopeful that there is real opportunity for a telehealth component to health care that is sustainable and reliable.”

—Kenric Maynor, MD, chair of Medicine Institute, Geisinger Health System (Deloitte Virtual Health Accelerated Roundtable participant)

Findings

One in two clinical leaders said the pandemic led to significant shifts in their health system’s virtual health strategy

The COVID-19 pandemic accelerated and catalysed several aspects of the Future of Health—particularly virtual health, which otherwise might have taken years to reach the level of adoption that took place during the pandemic. Deloitte was interested in learning how leading health systems are adapting, and how the rapid and forced shift to virtual visits and remote monitoring has impacted health system strategies and priorities around virtual health in the near and long term.

Deloitte research conducted in early 2020, before the pandemic, revealed modest growth of virtual visits and remote monitoring among physicians. From 2018 to 2020, adoption increased from 14% to 19%.4 Barriers around payment, concerns about fraud and abuse, and patient and clinician acceptance of the status quo were some of the reasons for the limited adoption. COVID-19 changed everything. By the middle of March 2020, many health systems were halting their nonurgent procedures and patients were staying away from clinical facilities to avoid potential exposure to the virus.5 Health systems, clinicians, and patients were forced to turn to virtual visits and remote monitoring. Both the clinical leaders we surveyed and the physician executives interviewed largely agreed that the experiences around virtual health during the first several months of the pandemic led to shifts in their health system’s virtual health strategy. Half of surveyed clinical leaders (52%) reported significant shifts, and 24% saw moderate shifts (figure 1).

Consumer demand, revenue and cost pressures due to the pandemic, pressure to keep up with competitors, and a relaxed regulatory and reimbursement environment were among the top reasons clinical leaders cited for the increased adoption of virtual health.

Looking ahead, 60% of respondents said their health systems need to make additional investments in virtual health, and 52% said it was essential to have an enterprisewide strategy (figure 2). Many hospitals are trying to determine which visits should be face-to-face and which ones should be virtual. While only 36% of clinical leaders said care pathways were used to guide those decisions, 54% are planning to develop such a strategy over the next one to three years. While just 16% of respondents said their health system has a “virtual first” system for scheduling certain visits, 52% said such a system was being planned. During our roundtable discussion, one physician executive said, “We are looking at ways to leverage data and develop algorithms to help predict the right length of visits, the type of visit, and whether it can be a video, phone, or face-to-face [visit] so that this process actually becomes more automated rather than leaving it up to the provider.”

“As devastating as COVID-19 has been, it has also been the best thing to come along in a long time in terms of stimulating health care innovation. It has forced us to accelerate our thinking in a lot of different ways, that we should have been doing, but we didn’t have the necessary pressure to do.”

—Robert J. Keenan MD, MMM, chief medical officer/vice president quality, Moffitt Cancer Center (Deloitte Virtual Health Accelerated Roundtable participant)

Our research participants agreed that, as health systems refine strategies and adopt new models, they should be mindful to avoid some of the mistakes that were made during the early years of the electronic medical record. Long before the pandemic, physicians were experiencing frustration and burnout from screen time and administrative fatigue.6 A recent study shows physicians were satisfied with virtual visits when they had input into how they were used, had administrative help, adequate payment, and access to reliable and easy-to-use technology.7 We expect to see increased investments in remote monitoring and patient wearables in the coming years. This will likely be driven by growing investments in digital health,8 and demand from clinical leaders. Half of the clinical leaders we surveyed said they wanted more functional tools and technology to optimise virtual health (figure 2). Health system leaders should think through how to seamlessly integrate those tools and platforms so that they enhance clinical care rather than add work for clinicians.

Across care settings, clinical leaders describe the optimal level of virtual visits as being close to the peak they witnessed during the pandemic

During our roundtable discussion, physician executives said they were interested in determining the optimal level of virtual visits for the future. Clinical leaders we surveyed indicated that the optimal level of visits over the next one to three years could be similar to the peak volume they saw during the pandemic.

When face-to-face visits reached their lowest point during the pandemic, virtual visits for primary care and for chronic condition management peaked at 45% and 41%, respectively (figure 3). Virtual visits for nonsurgical specialty care in outpatient settings (excluding behavioural health) peaked at 34%. Clinical leaders agreed that the optimal level of virtual chronic-condition management and primary care will be about one-third of overall visits. Prepandemic levels of virtual visits for those areas of care were around 5%. This willingness to continue virtual visits at levels that are close to the peak seen during lockdowns could be good news for the continued growth of virtual health.

We asked clinical leaders which areas of hospital stay they expect would be most impacted by the acceleration of virtual health. A majority of them said that there could be a significant increase in virtual technology for prestay scheduling and reminders, postdischarge chronic-care check-ins, patient monitoring, and follow-ups in the coming months and years.

We also asked which specialties would likely see the largest uptake in virtual visits over the next one to three years. Primary care topped the list, followed by behavioural health, dermatology, and internal medicine.

“Once we are through the pandemic … we will be able to truly evaluate the operational efficiency and opportunity from virtual health. Patient access and patient convenience are key goals, and we have a whole new world of competitors. I think if we don’t (invest in virtual health), then we will fall behind.”

—Brian Hasselfeld, MD, medical director, digital health & telemedicine, Johns Hopkins Medicine (Deloitte Virtual Health Accelerated roundtable participant)

Clinical leaders reported offering technology and privacy training to their staff, while clinical and web-side manner training is less common

The Deloitte 2020 survey of US physicians, conducted before the pandemic, found that approximately 85% of physicians thought that training on how to communicate effectively with patients—using virtual means—was currently lacking, but would be essential for success in the future.9 In prior research, we have emphasised the importance of training clinicians to be able to convey empathy, build rapport, make eye contact, and other critical bedside manner techniques in a virtual setting.10 In our latest survey, 74% of clinical leaders said they are currently offering training related to the Health Insurance Portability and Accountability Act (HIPAA), and ensuring that patient information is protected on virtual platforms. Training staff on software, apps, and other platforms is also common (70% of clinical leaders are currently doing this). However, only 36% of clinical leaders said they currently have “web-side manner” training on best practices for communicating and interacting with patients remotely, and 28% expect to develop this content in the next one to three years. That still leaves about 30% with no well-defined plans to offer such training (figure 4).

We continue to call for health systems to consider training clinicians and support staff on how to ensure a high-quality virtual visit. If patients do not feel virtual visits match the quality of face-to-face visits, we will lose momentum around virtual health. Further, as wearable and remote monitoring technology become more sophisticated, we should be able to take vital signs and gather other important biometric data remotely, which could put virtual visits more on par with face-to-face visits. Clinical leaders should consider strategies to implement those technologies. To create a sustainable program, health systems should also think about the experience for all users (clinicians, patients, front- and back-office support staff). Clinical leaders should consider applying the principles of human-centered design, training users on the technology, and ensuring continuity of care through follow-up virtual visits.

Measuring the performance of virtual health programs: Process and utilisation metrics are tracked comprehensively; quality of care and team-experience measurements are lagging

During the public health emergency, several regulatory flexibilities made it easier for clinicians and health systems to adopt virtual health. As we look to the future, regulators should determine whether temporary rules should be made more permanent. They will likely evaluate the payment models and benefit designs that support virtual health and their ability to improve patient health, while reducing the use of low-value services and unnecessary care. Rather than sequential visits with separate specialists, virtual health makes it possible for patients to connect to a suite of caregivers who can work collaboratively to offer more comprehensive and coordinated care.11 If health systems take existing care models and simply convert them into virtual formats, we could lose momentum and fail to realise the full potential of virtual health. As health care stakeholders work to redesign care models, clinical leaders should measure clinical and patient-centred outcomes. This could help ensure that the use of virtual health will continue to grow. 12

One area that will be important to capture is the extent to which remote monitoring can evaluate how well patients are managing their conditions. We can learn a lot from applying advanced analytics to large populations of patients who are monitoring their conditions at home. For example, data from glucose monitors that track diabetes, peak-flow meters that monitor asthma control, and weight and oxygen-saturation metrics for those with heart failure, can help clinicians learn how well patients are managing their conditions. Data from these devices can also highlight barriers they face and identify nudges that might be effective at changing behaviour. Health systems can begin to leverage this collective data to learn how to support patients more effectively.

To measure the performance of their virtual health programs, most clinical leaders said their organizations comprehensively track patient-experience measures such as patient satisfaction (74%) and access to care and wait times (52%) (figure 5). Almost two in three health systems also comprehensively measure utilisation and resource measures, such as length of stay, admissions and re-admissions, and emergency room utilisation. However, about 75% of clinical leaders reported either partial tracking or no tracking of quality measures, such as medication adherence and continuity of care. These measures will likely be critical in building data on health improvement and outcomes. Going forward, these measures could be essential—not only from a regulatory perspective, but also to stay competitive. The ability to successfully track such measures could also lead to more successful collaboration with health plans. Health systems that collect this data could use it to make the case for virtual health to patients, clinicians, employers, and health plans.

Another area with minimal tracking is the care-team experience—including physician and care-team satisfaction, and the level and quality of collaboration. These measures could help shape workforce and operational strategies to tackle issues such as physician and care-team burnout, and how to build on and improve team-based care or re-design care altogether.

“The COVID-19 remote patient-monitoring program we developed really activated and engaged our practice … and now several specialties want to extend remote monitoring to their patients as well.”

—Tufia Haddad, MD, medical director of the Center for Connected Care Remote Patient Monitoring program and chair of digital health for the Department of Oncology, Mayo Clinic (Deloitte Virtual Health Accelerated Roundtable participant)

Consumers and physicians are on board with virtual health. However, interoperability, integration of platforms, and data-security vulnerabilities continue to be a challenge

Despite an uncertain regulatory and reimbursement environment, clinical leaders we surveyed—and the physician executives who participated in our roundtable—agree that virtual health is here to stay. Prior to the pandemic, only 25% of primary care physicians, 17% of nonsurgical specialists, and 9% of surgical specialists reported that there was consumer demand for virtual health in their practices.13 When our latest survey respondents were asked about the top challenges their health systems overcame during the past few months, consumer and physician reluctance to virtual health were no longer seen as concerns.

Other Deloitte research shows that after the pandemic began, some health system chief financial officers expanded their virtual health strategies and created executive command center strategies that allow for more rapid decision-making.14 As a result, several health systems were able to quickly transition to virtual care. However, some challenges remain. As health systems attempt to mainstream virtual health into the existing clinical and revenue-cycle workflows, 66% of the clinical leaders we surveyed said data security is a long-term concern, 62% said interoperability remains a challenge, and 52% cited a lack of integration with other platforms.

The clinical leaders shared their investment priorities today and in coming years. Most respondents (78%) said high-speed internet is a top investment priority. Looking ahead one to three years, clinical leaders said artificial intelligence (AI) and machine learning were top investment priorities (68%). Physician executives in our roundtable discussed the use of AI for clinical-decision support and the management of staffing.

As health systems continue to scale up virtual health, they will likely want to capture data from remote monitoring tools and wearables, integrate the data with electronic health systems and clinical-decision support, and build real-time dashboards. However, though cited in the survey results as challenges that need to be overcome, data interoperability and cyber security did not appear to be top priorities for future investments. This could turn out to be a blind spot for health systems going forward. Health systems leaders should consider prioritizing investments in those areas, not only to satisfy regulatory requirements, but also to gain a significant long-term competitive advantage.

The pandemic has highlighted the digital divide

Many have been spending much more time at home since the pandemic began. We are ordering groceries, doing our work, and even having our children attend school online. But not everyone has equal access to high-speed internet. There are disparities by race, income, geography, age, and other factors.15 As of February 2019, 79% of white households had access to home broadband, compared to 66% of Black households, and 61% of Hispanic households. Ninety-two percent of those with a household income of US$75K or more have access to home broadband. By contrast, 56% of people who have household income below US$30K have access to broadband. More than one in three households headed by a person age 65 or older do not have a desktop or a laptop computer, and more than half do not have a smart device.16 Older Americans, and people who live in rural areas, are also much less likely to have access to home broadband.17

Lack of broadband internet is associated with fewer telehealth visits and reduced use of patient portals. Stakeholders, including policymakers, public health officials, and health care organisations, should work together to ensure that as we shift more health care into the home, we do not increase disparities.

Implications for health systems

Virtual health gains could be a silver lining of the pandemic. We could be as many as five years ahead of where we expected to be on our future-of-health journey. To keep this momentum going, health care stakeholders should:

- Adapt team-based care and operations to realise the full benefits of virtual visits. Clinical leaders told us that the optimal level of virtual health (for primary care and chronic care) would be about one-third of all visits. Before that can happen, many health systems will need to build new workflows or re-design existing workflows, create scheduling capabilities to enable specialist consultations and easy referrals, integrate digital health devices, collect patient-reported outcomes, and develop new approaches for data analytics and interpretation. While barriers remain, clinical leaders can work to advance the integration of behavioural health, primary care, and specialty care, and help family caregivers become more involved in care. This can ultimately lead to better adherence and better health outcomes.

- Train clinicians and support staff to improve the quality of visits. Training clinicians and staff to conduct high-quality virtual visits is essential but lacking. Health plans and health systems should ensure virtual visits are on par with traditional visits in terms of quality and patient satisfaction. The human-experience component should be considered in every element of virtual health, including virtual check-ins and follow-ups, accessing the patient portal, and virtual visits and remote monitoring.

- Move beyond process measures in their virtual health programs to more meaningful measurements, including quality-of-care and care-team experience. Health systems should plan to increase tracking of these measures and set targets to improve them. Health plans will likely make these table stakes in coming years. There are opportunities for health systems and health plans to collaborate and experiment with strategies to improve measurement and performance of their virtual health initatives.

- Recognise that we won’t realise the full value of virtual health if it becomes another layer of the traditional health care system. In theory, increased use of virtual health should enable integration of care from multiple team members more seamlessly. However, our findings show that clinical leaders have concerns around the digital divide, the ability to address disparities, lack of interoperability and platform integration, and physician burnout. Research also shows that patients and families look for certain characteristics in their health care interactions.18 They want to feel like the care is personal and they want to connect with clinical staff on some level. They also want a simplified experience that is convenient, as well as transparent, so that they can clearly understand what is happening to them and why. Finally, patients require security around their personal health information.

Maintaining momentum in virtual health will not be easy. It will have to happen while we are still fighting the pandemic, implementing the largest-ever vaccination campaign, recovering from financial losses, and restoring morale from the exhaustion, burnout, and forced layoffs. But health systems should keep pushing forward to stay competitive and to move closer to the future of health.

Deloitte's Life Sciences and Health Care Consulting Services

Innovation starts with insight and seeing challenges in a new way. Amid unprecedented uncertainty and change across the industry, stakeholders are looking for new ways to transform the journey of care. Deloitte’s US Life Sciences and Health Care practice helps clients transform uncertainty into possibility and rapid change into lasting progress. Comprehensive audit, advisory, consulting, and tax capabilities can deliver value at every step, from insight to strategy to action. Find out more at Deloitte.com.