The value of online banking channels in a mobile-centric world

It may be a mobile-first world, but consumers still use—and sometimes prefer—online banking channels. Here are some key lessons our global consumer survey on digital banking revealed about online banking usage.

Many banks across the globe are pursuing a mobile-first strategy with vigour. Some have even launched mobile-only banking brands to ward off fintech challengers,1 while the majority are enhancing their mobile apps with new features such as person-to-person payments, personal financial management tools and virtual assistants.2

This focus on mobile banking is certainly justified, yet there seems to be little discussion lately about the role of online banking in a mobile-dominant world. As more and more customers adopt mobile banking, will online banking remain pertinent - and if so, in what capacity?

Findings from Deloitte's global digital banking survey of 17,100 consumers across 17 countries on their digital banking behaviours and channel usage suggest banks should continue to invest in making online banking a seamless and high-quality customer experience. The survey findings reveal online banking may remain a key channel of customer interactions in the foreseeable future, even among mobile banking users.

Our survey found 73 per cent of respondents globally use online banking at least once a month, compared to 59 per cent who use mobile banking apps. Moreover, it revealed no generational differences in how frequently online banking is used - baby boomers use online banking just as often as tech-savvy millennials.

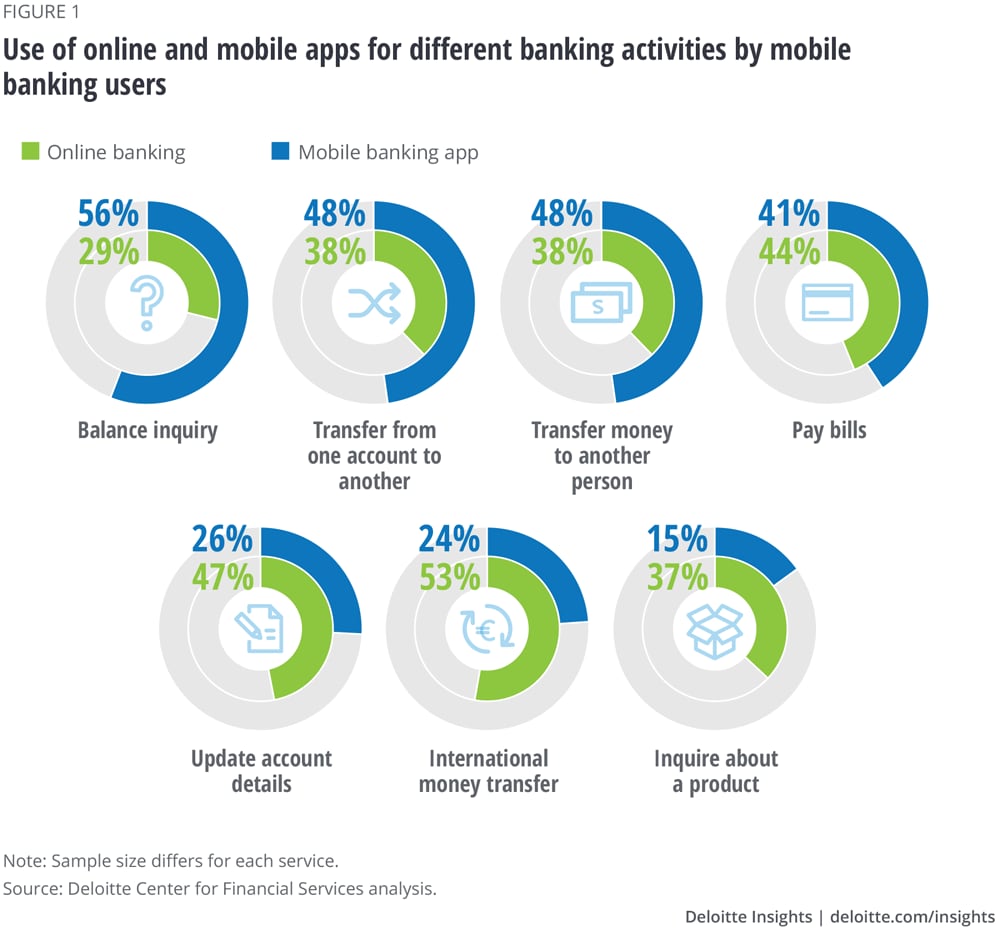

Even more interesting, mobile banking customers3 who responded to our survey continue to use online banking channels extensively: Ninety-four per cent use the online channel at least once a month. These respondents said they use mobile banking for relatively simple and quick transactions, such as transferring money or balance inquiries, but prefer to go online to transfer money internationally, enquire

about products, or update account information.

When selecting a primary bank (the bank that handles most of their banking needs), seven out of 10 survey respondents said having a consistent experience across channels, including mobile and online, was extremely important or very important to them. Our survey also showed customers globally are more likely to use online banking more frequently if banks increase security, provide more real-time problem resolution and allow more regular banking transactionsto be completed online.

Overall, these findings suggest that as banks continue to invest in improving and enhancing mobile capabilities, there are potential challenges if banks allow mobile banking to fully eclipse online banking. Instead, banks should continue to enhance the value proposition of the online channel, focusing on evolving the online banking experience rather than seeing it as a phase-out to mobile. To do this, banks should aim to provide a more seamless experience between online and mobile channels and purposefully measure online customer engagement to meet evolving customer needs and preferences.

Deloitte Consulting

Innovation, transformation and leadership take many forms. At Deloitte, our capacity to help clients tackle their most complex issues is unparalleled. We provide strategy and implementation from both a business and technology perspective, to help you stay ahead in the markets in which you compete.

{kind=link}