Shaping the Internal Audit Function of the Future has been saved

Services

Shaping the Internal Audit Function of the Future

From Vision to Value, We’re Transforming Trust with Technology.

Internal Audit (IA) requirements are constantly evolving, yet constraints on resources can make it difficult to keep up. We help our clients to elevate their impact by infusing value at every stage of the internal audit process. We team with your IA function to deliver purpose driven, digitally powered internal audits leveraging automation, analytics, dynamic risk assessment, and agile methodology that align with your strategy. Let us help you anticipate risk and put the right processes and controls in place today to meet the challenges of the future.

Forging the Internal Audit function of tomorrow depends on the steps taken today to infuse value throughout the IA life cycle. Deloitte IA can advise your organization to anticipate risks, cultivate trust, employ emerging technology, and accelerate organizational change to meet new challenges. We help you deliver desired business outcomes using a four-pronged approach—enhancing, advancing, addressing, and adapting.

Deloitte’s Internal Audit Solutions:

Unlock strategic solutions with our internal audit services

Our approach, your advantage

As an alternative to an in-house-only function, many companies outsource or co-source with Deloitte to gain access to industry leaders, subject-matter specialists, and global teams. The outsourced provider invests in training, tools, technology, and intellectual capital, while company management still maintains control and has a single point of accountability. This flexible, scalable approach offers benefits such as lower fixed costs, staffing flexibility, and access to the latest technology, among many others.

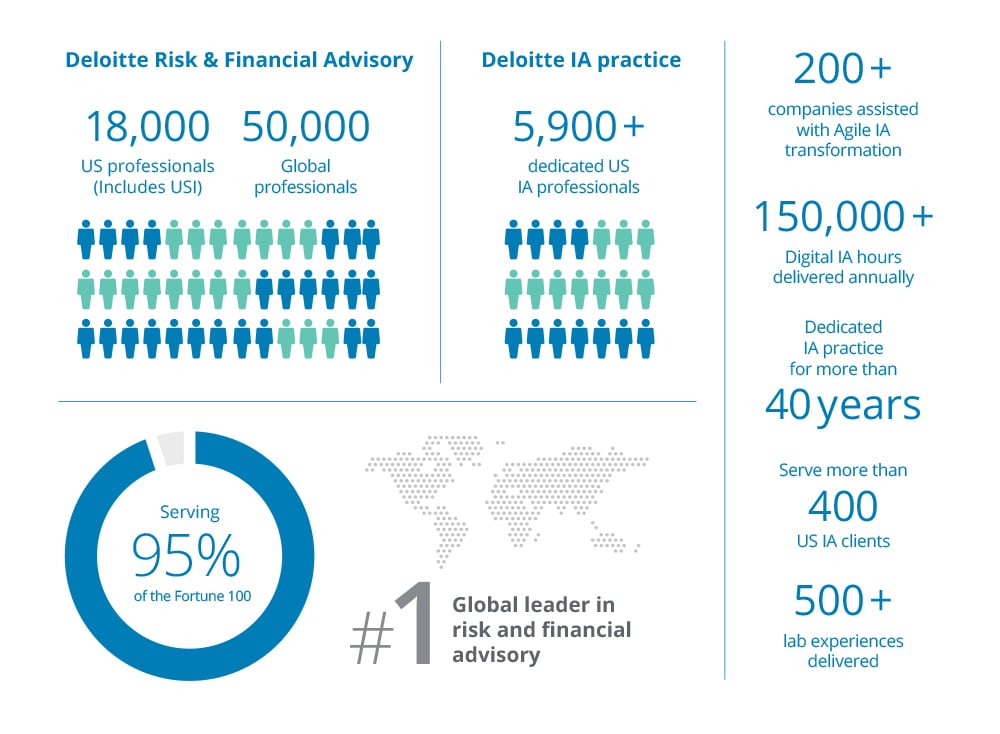

About our practice

An integral part of Deloitte Risk & Financial Advisory’s Accounting & Internal Controls offering portfolio, our IA practice stays ahead of trends and has the vision to translate them into value. We deliver our co-sourced/outsourced services through our fully integrated IA practice, which brings together a core risk and controls team complemented with specialist competencies in various domains, such as IT audit, cybersecurity, enterprise risk management, enterprise resource planning, SOX, contract risk and compliance, forensics, ESG, supply chain, human capital, capital projects, and regulatory audit and risk services.

We also leverage our IA leading practices/modernization framework to help you define your vision for the future and transform through enabling technology and innovative ways of working, resulting in cultivating trust and elevating impact.

Get in touch

Sarah Fedele

Principal | Deloitte Risk & Financial Advisory

Recommendations

Internal Audit 4.0: Megatrends reshaping the IA framework

Purpose-driven and digitally powered IA function of the future

Internal Audit perspectives

Your one-stop shop for all things IA