Deloitte's take on the move to T+1 settlement and impact on stock-based compensation has been saved

Perspectives

Deloitte's take on the move to T+1 settlement and impact on stock-based compensation

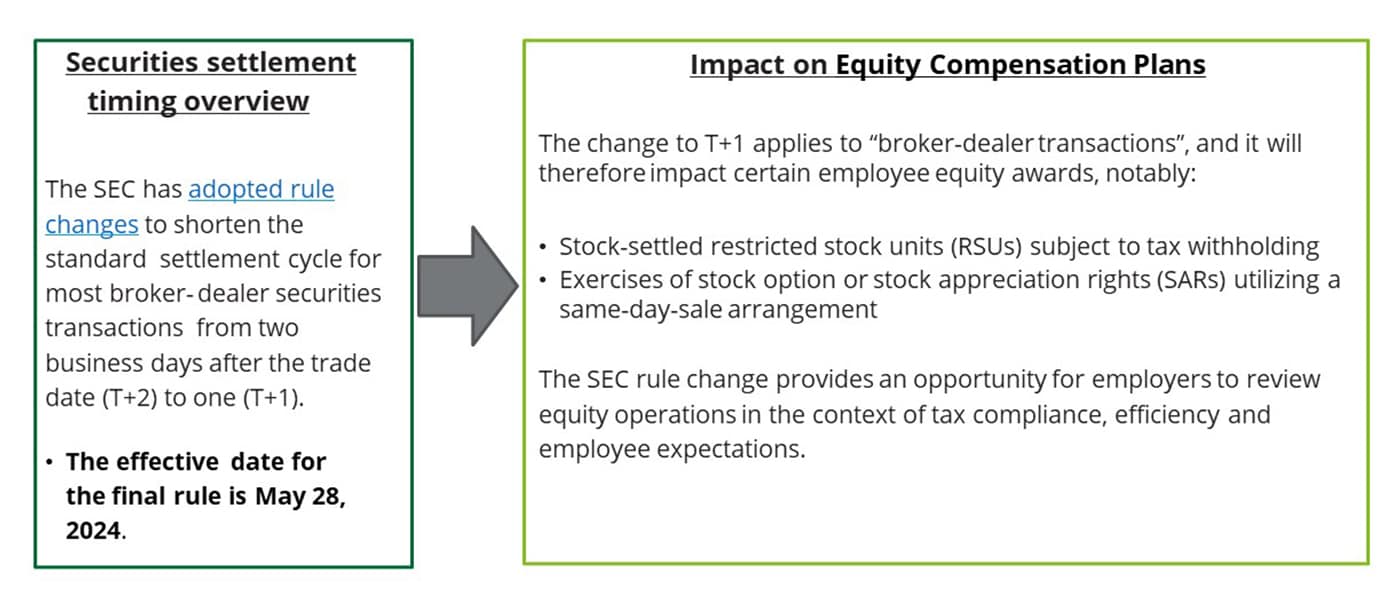

As the introduction of T+1 settlement draws closer following the SEC’s adoption of new rules, companies and brokers are considering the impact the change will have on equity compensation plans.

There is increasing pressure on employers to ensure broker-dealers are equipped with the data points to settle certain employee equity award transactions. Equity award settlement involves coordination amongst multiple stakeholders (broker, payroll, tax and transfer agent, to name a few), and in a decreasing window of time. The updates on the horizon to settlement timing suggest employers should assess and determine whether their equity compensation programs are operating in a manner that not only allow the employer to meet its tax compliance obligations but also meet employee expectations.

|

What are the key considerations for equity compensation plans?

While there are several impacts to the broader employee share plan industry, a few notable areas for consideration include:

${column1-large-text}

Tax withholding

With a shortened settlement cycle for broker-assisted equity transactions (e.g., same-day-sale option exercises or RSU vests subject to withholding), employers may have to review their approach to tax withholding.

${column2-large-text}

US tax remittance

If the U.S. ‘next day deposit’ rule applies, employers have until the day after settlement to remit employment taxes to the IRS, provided settlement occurred within two days of payment being

initiated. Going forward, because settlement will occur a day earlier, the same tax remittance would also be due a day earlier (i.e., on T+2 instead of T+3).

${column3-large-text}

Employee experience

We have seen many employers in recent years increasingly prioritize employee experience in the context of their share plans. These employers are focusing on education and financial wellbeing

programs as well as employee expectations around award settlement.

${column4-large-text}

${column4-title}

${column4-text}

What can companies be doing to prepare?

Looking at the considerations noted earlier, employers who issue equity-based awards may want to consider some of the areas below in preparation for the arrival of T+1 (May 28, 2024).

There are various items for employers to consider when it comes to assessing the impact of settlement timing being reduced to T+1. In explaining the reduced settlement cycle, the SEC signaled consideration of an eventual shift to a T+0 settlement cycle. Employers may want to consider the potential for future rule changes when designing their equity processes. For now, however, it is critical for employers to coordinate with key stakeholders, including stock plan administrators and payroll, to confirm they are aware of the new settlement process timing and how this may affect compliance with payroll and employment tax deadlines and processing.

Get in touch

|

|

|

|

|

|

|

|

||||||

Sandy Shurin |

Meridith Fronza |

Mark Miller |

Patrick Grimes |

Recommendations

Reward, Employment Tax, and Equity Compensation Plans

Helping design and implement competitive reward programs

When employees make a move: Taxation on equity incentive plans

Are you on track with tracking?