Creator Economy in 3D: The platform’s place in a shifting media landscape has been saved

Perspectives

Creator Economy in 3D: The platform’s place in a shifting media landscape

Consumers and social media

The consumer media landscape is changing. Social platforms have become a mainstay media outlet for consumers, and content creators are the beating heart of a $250 billion revenue opportunity that is projected to nearly double over the next three years¹. To seize this opportunity, platforms should meet shifting consumer content preferences and foster a lucrative environment for creators and brands alike.

Deloitte’s Creator Economy in 3D research sheds light on the interplay between consumers, creators, and brands—including what drives consumer engagement on a platform, what features draw new and established creators, and how to deepen the engagement of existing creators.

In this report we’ll cover how creator platforms can address…

- Shifting consumer preferences for content length and communities

- How creators energize and benefit from platform communities

- How creator platform priorities change over their lifecycle

- What brands prioritize when investing in a platform

Consumer Preferences Trending Towards Long-Form Entertainment on Social Platforms

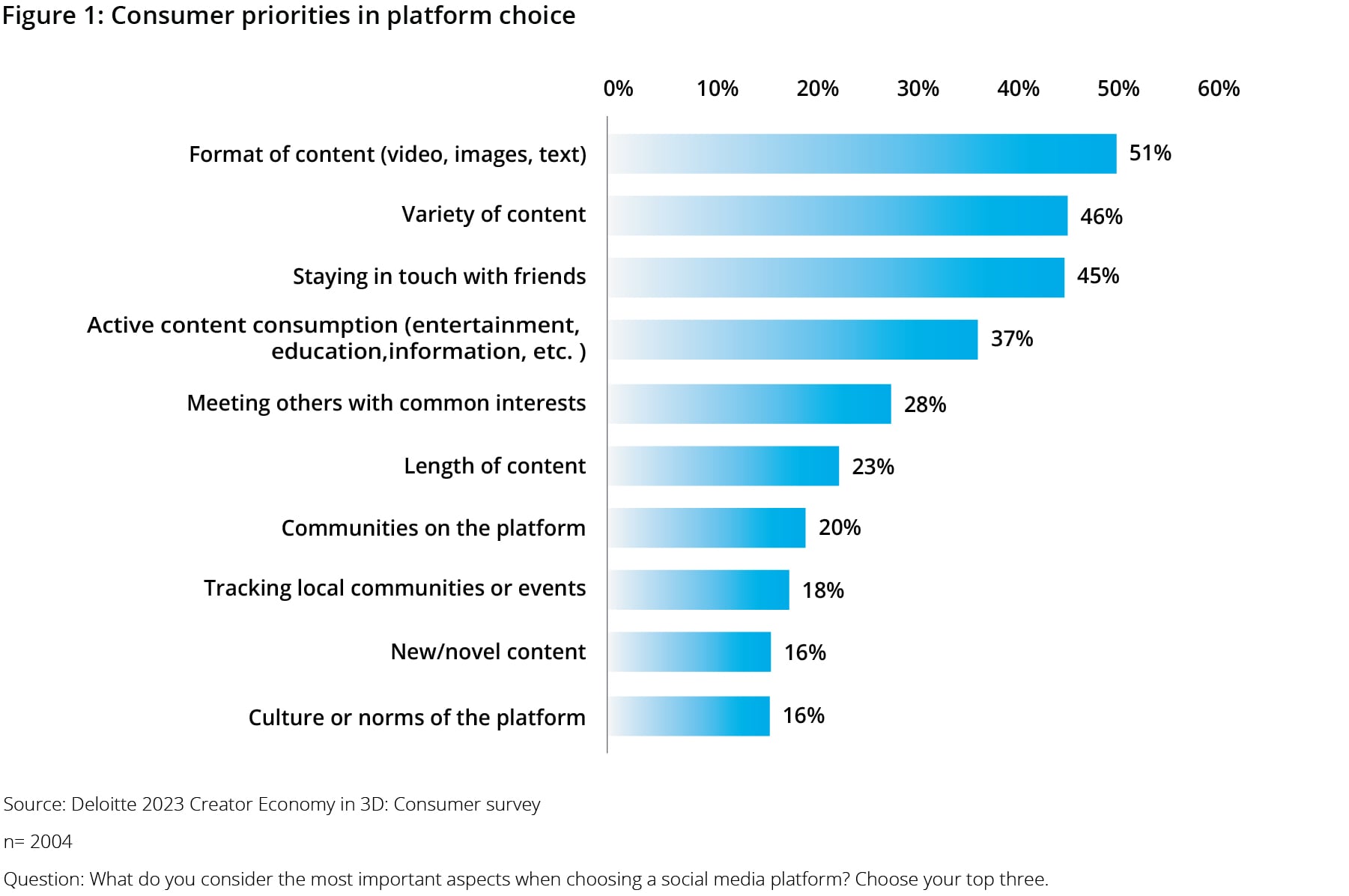

Social media platforms have established themselves as a vital source of entertainment and information for consumers. In fact, the boundless volume and variety of user-created content has positioned social media as a strong competitor to traditional media companies, with many consumers now preferring social media to streaming TV and movies.ii We found respondents’ top priorities in a social platform only reinforce this trend (figure 1).

Deloitte found that the format of content itself stands out as consumers’ top priority in a platform, followed closely by the variety of content. The prevailing consumer preference is for the short, varied content that social platforms have pioneered, with most consumers leaning toward short (less than a minute) to mid-length (1-10 minute) video (figure 2).

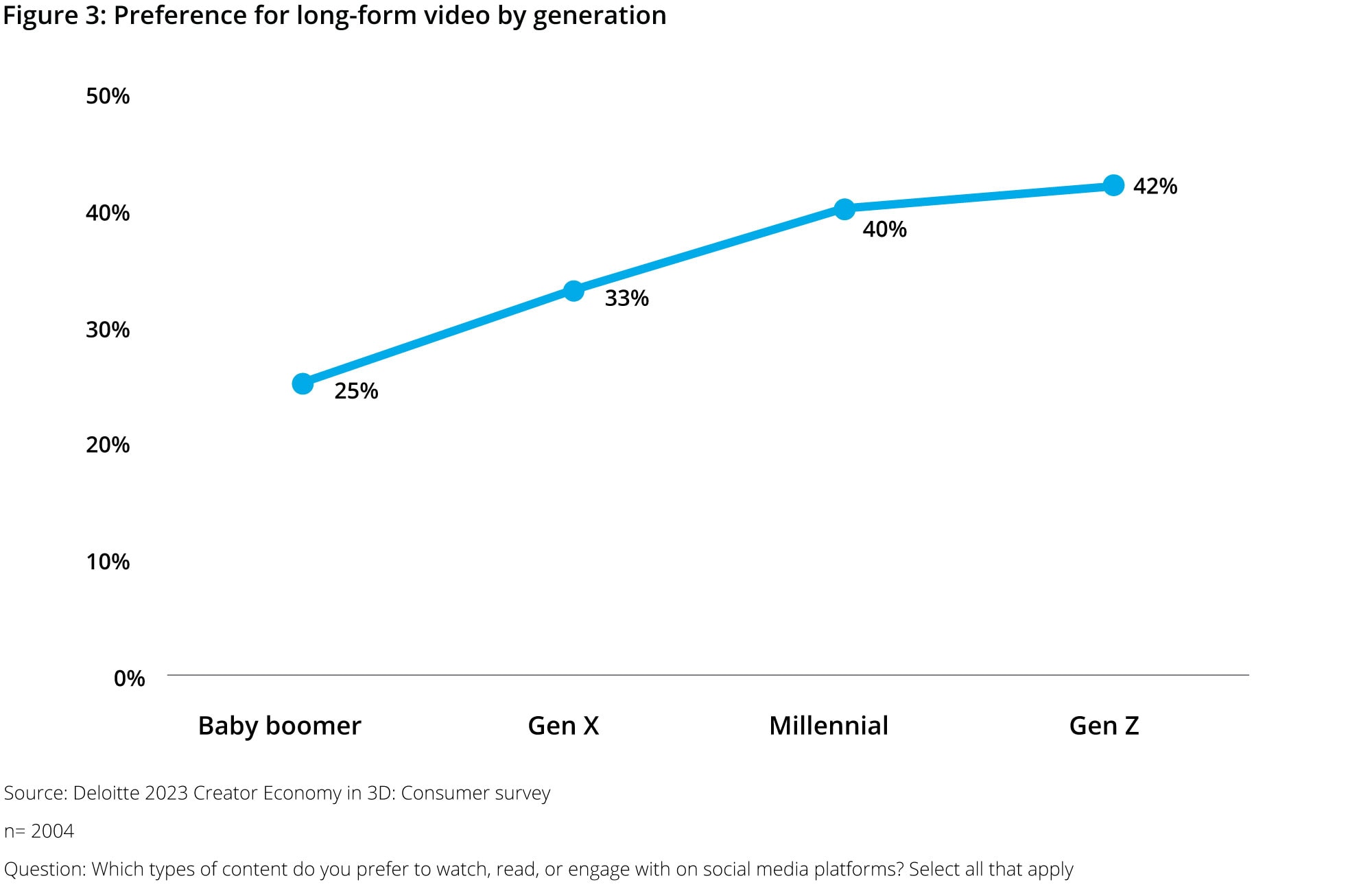

While this preference for shorter-form content speaks to the draw of platforms in providing viewers with a continual stream of varied content, we also found these consumer preferences may be starting to shift. The preference for long-form videos on social media appears to be steadily increasing among younger consumers, with 42% of Gen Z social media users preferring longer length (greater than 10 minute) videos, compared with 33% of Gen X and only 25% of Baby Boomers (figure 3).

The increasing desire for long-form content suggests social media platforms are increasingly poised to compete with traditional media as a source of entertainment among younger generations—if they can attract and incentivize this type of content from creators.

And while this trend does not indicate long-form content is replacing the short and varied content that still tops consumer preferences, platforms have an opportunity to capture an additional contextual preference—the desire or mood to engage with longer-form or serialized media.

Platforms: Maintain short-form content while ramping up the availability of longer-form content

While platforms should continue to cater to consumer preferences for shorter videos, maintaining a broad competitive appeal for younger consumers means providing a variety of content lengths on the platform. The availability of longer-form creator content situates platforms to better compete with traditional television and streaming content.

Platforms can accomplish this by incentivizing creators to make longer videos, or to produce varying content lengths to appeal to a wider range of consumers. Platforms may consider providing creators with new tools or guidance for developing longer content or adapting their existing long-form content into shorter pieces.

Consumers’ Rising Preference for Platform Communities Provides Compounding Benefits

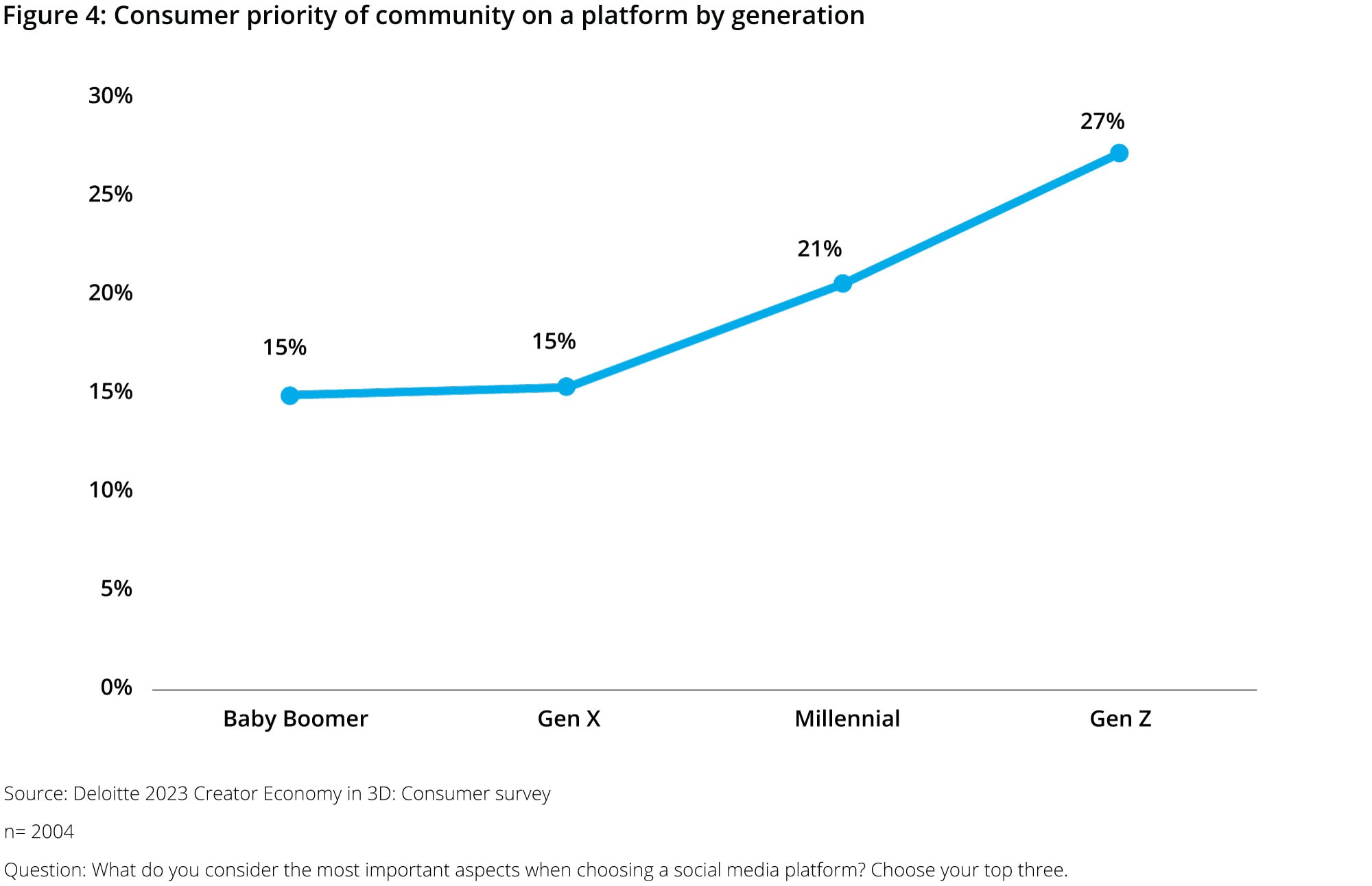

Connecting with friends is consumers’ third priority, after format and variety of content. For most consumers, personal peer groups are the main priority in platform, but Deloitte found a stark generational shift in how consumers look to social media for community (figure 4).

Over one in four Gen Z social media users prioritize a platform for communities of likeminded users, a figure nearly twice that of Baby Boomers and Gen X. And while catering to this preference may increase a platform’s general appeal, there could be farther reaching potential benefits for the entire platform creator ecosystem.

Communities Connect Creators and Consumers, Deepen Consumer Engagement, and Address Creator Priorities

Platform communities provide a clear audience for creators to bring their content, and a gathering place for consumers with shared interests. Deloitte found that 77% of consumers follow creators either out of a shared interest or hobby or desire to learn something new—indicating that creator followership is largely interest-driven and an incentive for platforms to help creators capitalize on these interest-based communities.iii

Facilitating the connection of consumers with the right creators can have an impact on that consumer’s engagement within a platform. In fact, one in three consumers already indicated they follow creators because those creators are part of a community they identify with.iv Deloitte found that younger generations of consumers are following more favored creators—creators that consumers actively seek out for new content and updates (figure 5).

These favored creators drive both consumers’ total time spent on a platform, and willingness to seek out additional creators. When asked about their platform engagement in relation to their favored creators, 63% of consumers say they spend more time in general on the platform because of these creators.v Additionally, 50% of these consumers indicate they actively seek out additional creators because of their favored creators.

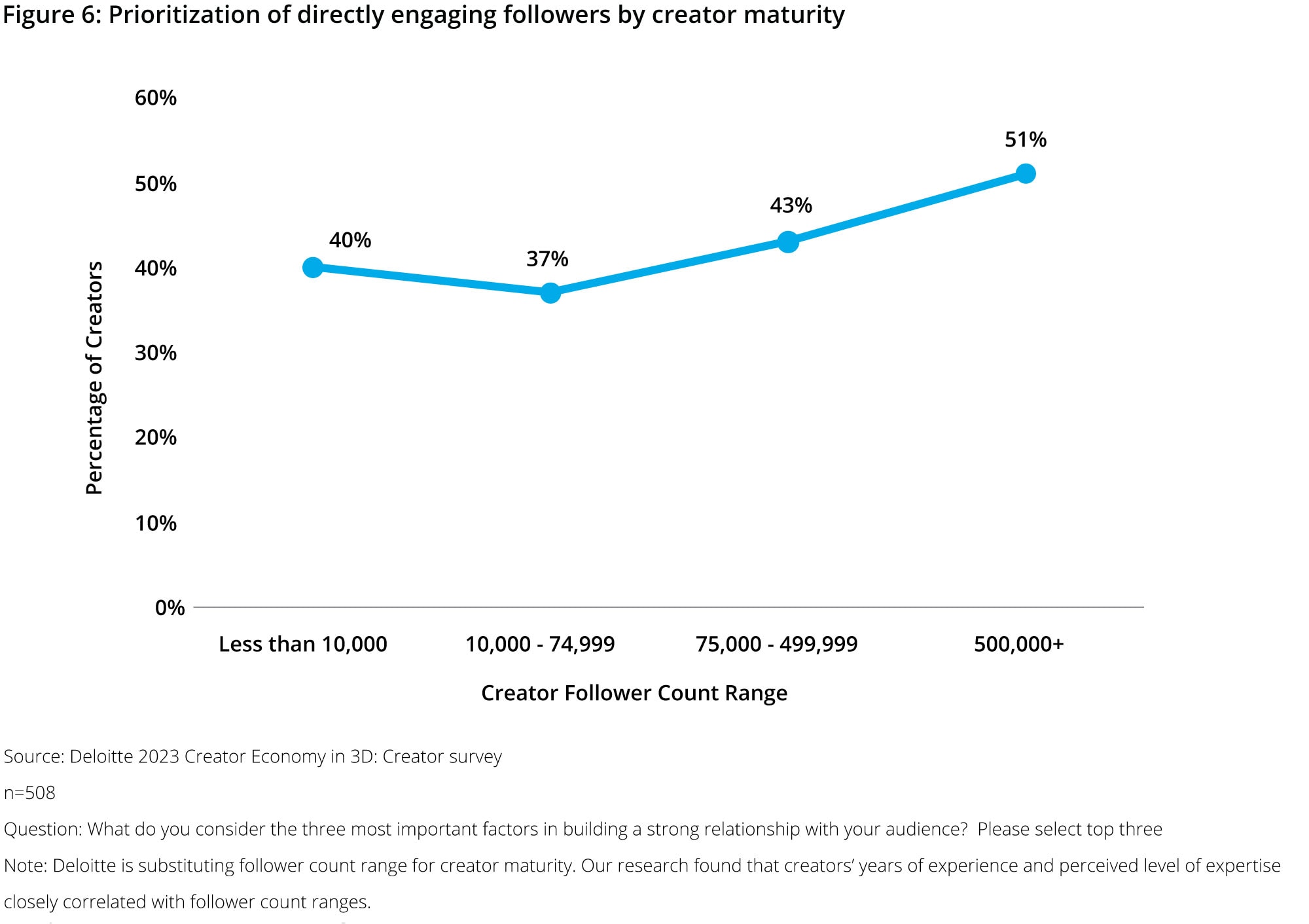

Improving the community experience is also important for creators themselves. Surveyed creators indicated that direct follower engagement is one of their top priorities overall for building a relationship with their audience, and it becomes increasingly important as they grow their following (see Figure 6).

By nurturing their user communities, platforms can connect consumers with more creators, deepen consumers’ relationship with the platform, and directly facilitate further creator engagement with their audiences.

Platforms: Lean into user communities to strengthen the overall appeal of your platform

Communities provide a more intentional pathway for users to guide their own content journeys that works alongside existing recommended content algorithms, connect creators and consumers, and provide creators with a further means of engaging their audiences.

Platforms should look to nurture the community spaces within their platform, integrate them within the platform experience, and make them easy for users to locate in relation to their interests.

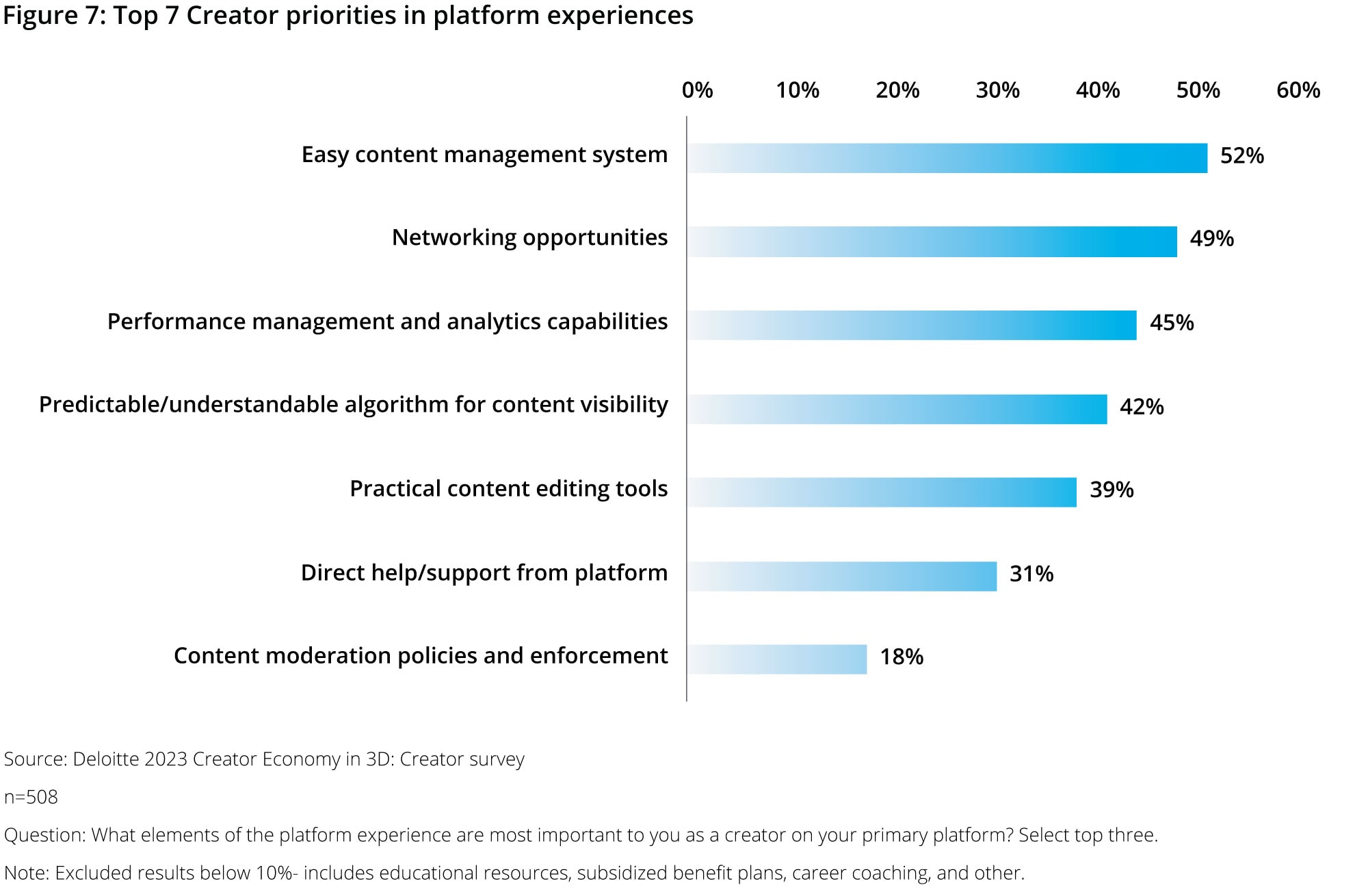

Content Management and Analytics Dominate Top Creator Platform Priorities

While platform communities may provide beneficial elements, creators have a range of business needs to consider in their platform experience. To understand how platforms can appeal to emerging and established creators, we asked creators to rank how they prioritize these factors (figure 7).

Overall, creators’ top priorities are focused on the monitoring and administration of their business. An easy content management system, and performance management and analytics capabilities take two of the top three spots for creators most important aspects of their platform experience. These are essential tools creators need to manage their business.

Creators also value networking opportunities—the platform’s ability to connect creators with other creators or professionals in their field. Platforms can increase their appeal to creators across the board by fostering creator to creator networking on their platforms. This is particularly important for platforms that are looking to draw new creators to their platform.

Content Management and Networking Opportunities Even More Important for Newer Creators

New and emerging content creators prioritize two facets of a platform experience at a much higher rate than more experienced creators: networking opportunities and an easy content management system (figure 8).

Platforms that are looking to differentiate themselves from their competitors for new and emerging creators may not only want to improve these aspects of their platform experience but market these aspects to those creators. And while this element is less often a priority among more experienced creators, 38% of the largest creators still prioritize networking opportunities in their platform experience—leaving this an appealing element for creators of all sizes.

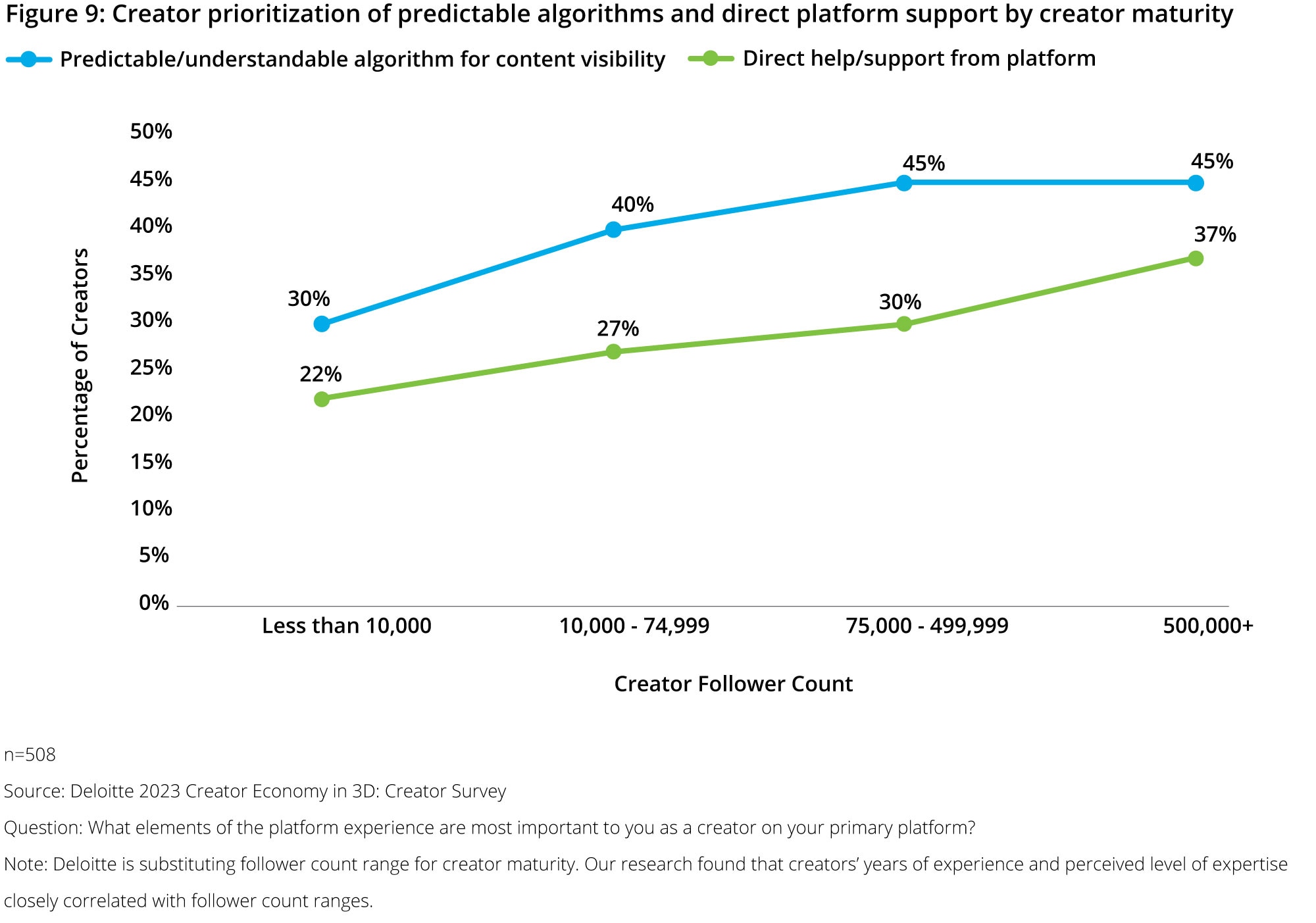

More experienced creators’ priorities shift squarely around analytics; predictable algorithms and direct platform support rise further

While networking opportunities makes the top three for creators’ platform priorities—this is largely skewed because of newer creators. When we look at creator platform priorities by creator lifecycle, late-stage creators’ top three priorities shift to a near-tie around content management and analytics:

Mature Creators’ Top Three Priorities in the Platform Experience

- Easy content management system

- Performance management and analytics capabilities

- Predictable/understandable algorithm for content visibility

Performance management and analytics, easy content management, and a predictable algorithm dominate experienced creators’ top priorities, followed closely by practical content editing tools. The relative importance of these elements against other factors cements the notion that creators are primarily focused on the tools to manage their business throughout their lifecycle.

However, two additional elements of the platform experience stand out among more experienced creators when compared with new and emerging creators: predictable content algorithms and direct platform support (figure 9).

Notably, the number of creators prioritizing direct platform support rises steadily as creators grow in experience and follower count—suggesting platforms may increase their appeal to more experienced creators by offering additional “white glove” support. Trends in creator prioritization of predictable algorithms suggests more experienced creators also increasingly favor stability on their platforms—i.e. they don’t want to continually adjust how they market and target their content.

Platforms: Content management tools provide the widest draw, but networking opportunities have stronger pull for new and emerging creators

In sum, the data suggests a professional mindset keeps creators on a platform. Having strong or easy-to-use tools for creating content as well as support from the platform to resolve issues as they arise has the potential to differentiate platforms among more mature creators. But just as consumers increasingly favor communities, platforms should also pay close attention to how they can help foster creator communities to facilitate networking for new, emerging, and experienced creators.

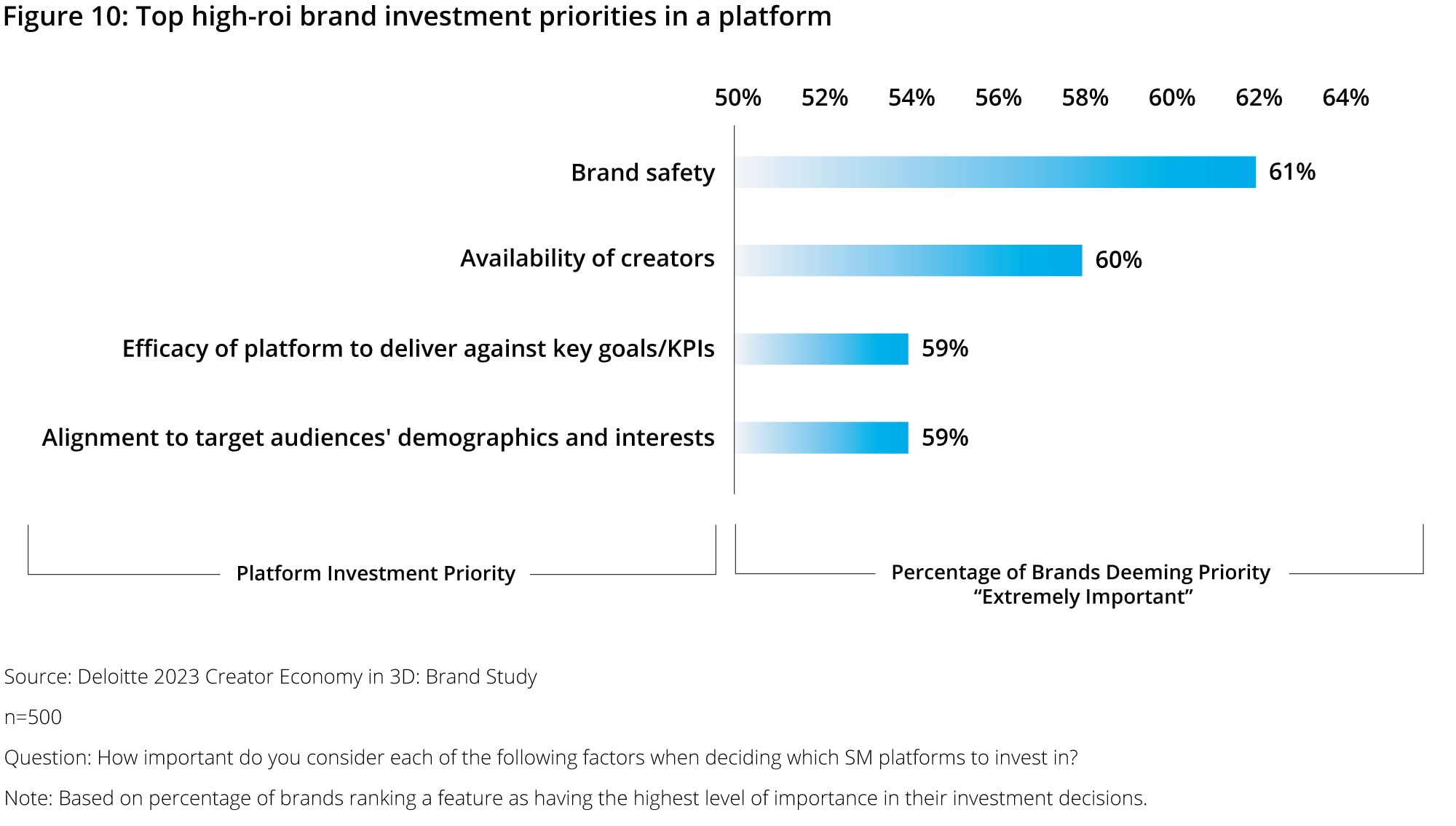

Brands Look to Platforms for Brand Safety, Creator Availability, and Audience Alignment

As the creator economy continues to grow, platforms should adapt an evolving relationship between brands, creators, and their place on their platform. In Deloitte’s 2023 Creator Economy in 3D report, we found that the brands reporting the highest ROI on creator-driven revenue are investing more of their social media budgets into creator partnerships and working with more creator partners at a time than other brands.vi As these high-ROI brands continue to trailblaze the marketing space of the creator economy, we looked at what features these brands prioritize in a platform compared with their less successful peers (figure 10).

High-ROI Brands Place Highest Priority on Brand Safety

High-ROI brands are placing the highest priority on keeping their brand safe from risks such as association with offensive content or controversial topics. Brand safety was not only the top priority for high-ROI brands, but they placed the highest priority on this element 1.7x as often as their low-ROI peers.vii While this is especially pertinent in cases of brand advertisements appearing in front of inappropriate or offensive content—there are additional elements to consider for creators—only 10% of surveyed creators strongly agreed that platforms adequately monitor hate speech or abuse.viii Fostering brand safety on a platform thus also translates to fostering a safe environment for creators, and their potential brand partners.

Brand Prioritization of Creator Availability Signals Continued Importance of Drawing Creators

High-ROI brands' second investment priority underscores the importance of platforms in maintaining a high availability of creators- especially as the market becomes more saturated. High-ROI brands primarily prioritize creators in higher follower count ranges (250-500k followers), but a broad range of creators is important to maintain as many brands also work with smaller creators.ix Aside from fostering an attractive environment for content creators, platforms can cater to this brand priority through an organized creator marketplace that facilitates creator-brand connections.

Closing thoughts: The evolving social media frontier

While social media is not wholly replacing traditional media, the trends we observe suggest that the social media space is a growing competitor. Platforms can now position themselves as direct competitors to streaming media in the future to capture new advertising revenue. This evolving media landscape poses important questions for how brands incorporate these trends into their media advertising and marketing strategies that platforms can help answer. To do so, platforms should adapt to what it means to be a community-driven media network and foster an environment where consumers, creators and brands can all thrive.

As a start- platforms should adapt to evolving consumer trends for longer-form content and facilitate their platform communities. These communities can play an important role in improving the platforms overall appeal to both consumers and creators. Platforms can further increase their appeal to creators by providing creators the tools and support they need and help connect them to other creators to learn and grow. Platforms have a responsibility help keep those growing communities thriving and safe for creators, brands, and consumers alike. Deloitte thrives within this complex intersection of consumers, creators, and brands to help you navigate this uncharted media territory.

Methodology

This series of three surveys provides insight into how consumers, content creators, and brands in the United States are engaging with each other within the content creator economy. The surveys were fielded by an independent research firm July–August 2023 and surveyed 658 content creators, 500 brands, and 2,004 consumers. Consumer data was weighted back to the most recent census data to give a representative view of consumer sentiment and behaviors. Our generational definitions are as follows: Gen Z (1997–2009), millennial (1983–1996), Gen X (1966–1982), boomers (1947–1965), and matures (1946 and prior). Creators were sampled according to a representative distribution of follower counts, including an 150-count oversample of creators from traditionally underrepresented groups (based on race, gender identity, and/or disability). Our brand sample targeted brands that reported a minimum annual revenue of $250 million or more.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

This article was authored by Connor Seidenschwarz and Bree Matheson.

Endnotes

i Goldman Sachs, “The creator economy could approach half-a-trillion dollars by 2027,” April 19, 2023.

ii Kevin Westcott, et. al. 2023 Digital Media Trends: Immersed and Connected, Deloitte Insights, April 14,2023.

iii Deloitte, 2023 Creator Economy in 3D: Consumer Survey.

iv Ibid.

v Ibid.

vi Deloitte, 2023 Creator Economy in 3D: Brand Survey.

vii Ibid.

viii Deloitte, 2023 Creator Economy in 3D: Creator Survey.

ix Ibid.

Get in touch

Kenny Gold

Managing Director, Head of Social, Content and Influencer | Deloitte Digital

Recommendations

The Creator Economy in 3D

This report covers how the content creator economy is changing consumer engagement with brands, media, and buying channels.